Last Updated on by Tree of Wealth

Each scheme caters to different retirement needs and has distinct features, making it essential for Singaporeans to understand their options. While most people born after 1958 are automatically enrolled in CPF LIFE, some may still qualify for the RSS. Choosing between the two depends on factors such as life expectancy, retirement goals, and financial situation.

This article dives into the key features, differences, and considerations for CPF LIFE and RSS to help you make an informed decision about which scheme best suits your retirement needs. With the right planning, you can ensure financial peace of mind and a comfortable retirement lifestyle.

Planning for retirement in Singapore can feel… a little overwhelming.

You’ve got CPF, Retirement Sums, payouts, eligibility rules—it’s a lot to take in. But at the centre of it all are two key schemes that determine how your CPF savings are eventually paid out: CPF LIFE and the Retirement Sum Scheme (RSS).

Most people have heard of CPF LIFE. It’s the newer one—launched in 2009—and it’s designed to give you monthly payouts for as long as you live. That’s a big plus if you’re worried about outliving your savings.

RSS, on the other hand, is the older system. Simpler. Payouts stop when your Retirement Account runs out or when you hit age 90—whichever comes first.

So which one’s right for you?

That depends.

-

Are you hoping to leave more of your CPF savings to your kids?

-

Do you expect to live past 90?

-

Do you have other income sources to fall back on?

In this guide, we’ll walk through the key differences between CPF LIFE and RSS. We’ll keep things simple, practical, and as close to real-life thinking as possible. By the end, you should have a better idea of which scheme fits your retirement goals—and your personal situation.

You May Be Interested

Quick Look: CPF LIFE vs Retirement Sum Scheme (RSS)

Not sure which scheme makes more sense for you? Here’s a side-by-side breakdown to help you spot the key differences quickly.

| Feature | CPF LIFE | Retirement Sum Scheme (RSS) |

|---|---|---|

| Payout Duration | Monthly payouts for life — no matter how long you live. | Payouts stop when your RA savings run out or when you turn 90, whichever comes first. |

| Who Qualifies | – Born in 1958 or later |

-

At least $60,000 in your Retirement Account by age 65

-

Singapore Citizen or PR | – Born before 1958, or

-

Born after 1958 but didn’t hit $60,000 in RA by payout age

| Feature | CPF LIFE | Retirement Sum Scheme (RSS) |

|---|---|---|

| Interest on Savings | Premiums earn up to 6% interest, but the interest is pooled to support payouts for all members. Only unused premiums are returned to your beneficiaries. | All remaining RA savings, including full interest, are passed on to your beneficiaries. No pooling involved. |

| Auto Enrollment | Yes — if you’re eligible (born in 1958 or later, with at least $60,000 in RA by age 65). | No — only applies if you meet specific criteria. |

| Can You Switch? | You can switch to CPF LIFE anytime before turning 80, even if you started with RSS. | Once you’ve joined CPF LIFE, you can’t return to RSS. |

This table gives you the essentials in one glance. Don’t worry if something’s still unclear—we’ll unpack all of it in the next sections.

1. Understanding CPF Retirement Sums

Before you dive into CPF LIFE or RSS, it helps to understand how much you’re expected to set aside for retirement. That’s where CPF Retirement Sums come in.

There are three tiers. Each one gives you a different level of monthly payouts.

-

Basic Retirement Sum (BRS) – For those who own a property and plan to use it as a security pledge. It gives you the smallest payout, but you keep more flexibility.

-

Full Retirement Sum (FRS) – Exactly double the BRS. This is for those who want higher monthly payouts, without using property as a backup.

-

Enhanced Retirement Sum (ERS) – Triple the BRS. It gives you the highest possible CPF payout, if you can afford to set aside that much.

You May Be Interested

Changes to CPF Retirement Schemes in 2025: What You Need to Know (and Why You Should Care)

Why It Matters

The more you set aside in your Retirement Account (RA), the higher your monthly payouts will be under CPF LIFE. Pretty straightforward.

Some people aim for the BRS and rely on other income (like rental). Others go all the way to the ERS for maximum peace of mind. It really depends on your lifestyle goals and how much flexibility you want.

CPF also offers relatively high interest — up to 6% per year — which makes early contributions more powerful thanks to compounding.

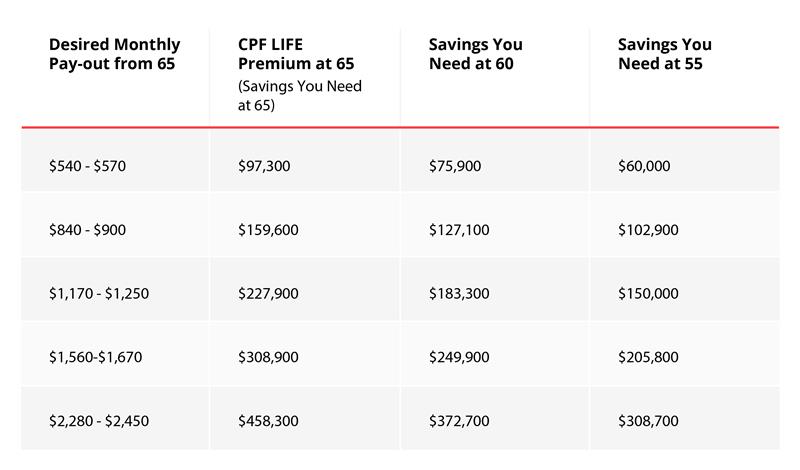

Estimated Monthly Payouts (Turning 65 in 2034)

| Retirement Sum | Set Aside in RA | Monthly Payout (Est.) |

|---|---|---|

| BRS | $102,900 | $890 – $970 |

| FRS | $205,800 | $1,560 – $1,670 |

| ERS | $308,700 | $2,270 – $2,420 |

Source: CPF Board, 2024 estimates

Real-Life Examples

Let’s put this into context:

-

Mr. Tan owns a fully paid HDB and has rental income. He sets aside the BRS and gets around $900 a month from CPF, which tops up what he already has.

-

Ms. Lee wants full financial independence. She opts for the FRS and receives about $1,600 monthly—enough to live comfortably on her own terms.

-

Mr. Raj wants the biggest possible payout and doesn’t mind locking away more CPF savings. He goes for the ERS and gets over $2,400 each month.

Everyone’s situation is different. Some people want to leave more behind. Others want to spend freely in their later years. What matters is choosing the Retirement Sum that fits you—not what everyone else is doing.

Source: CPF

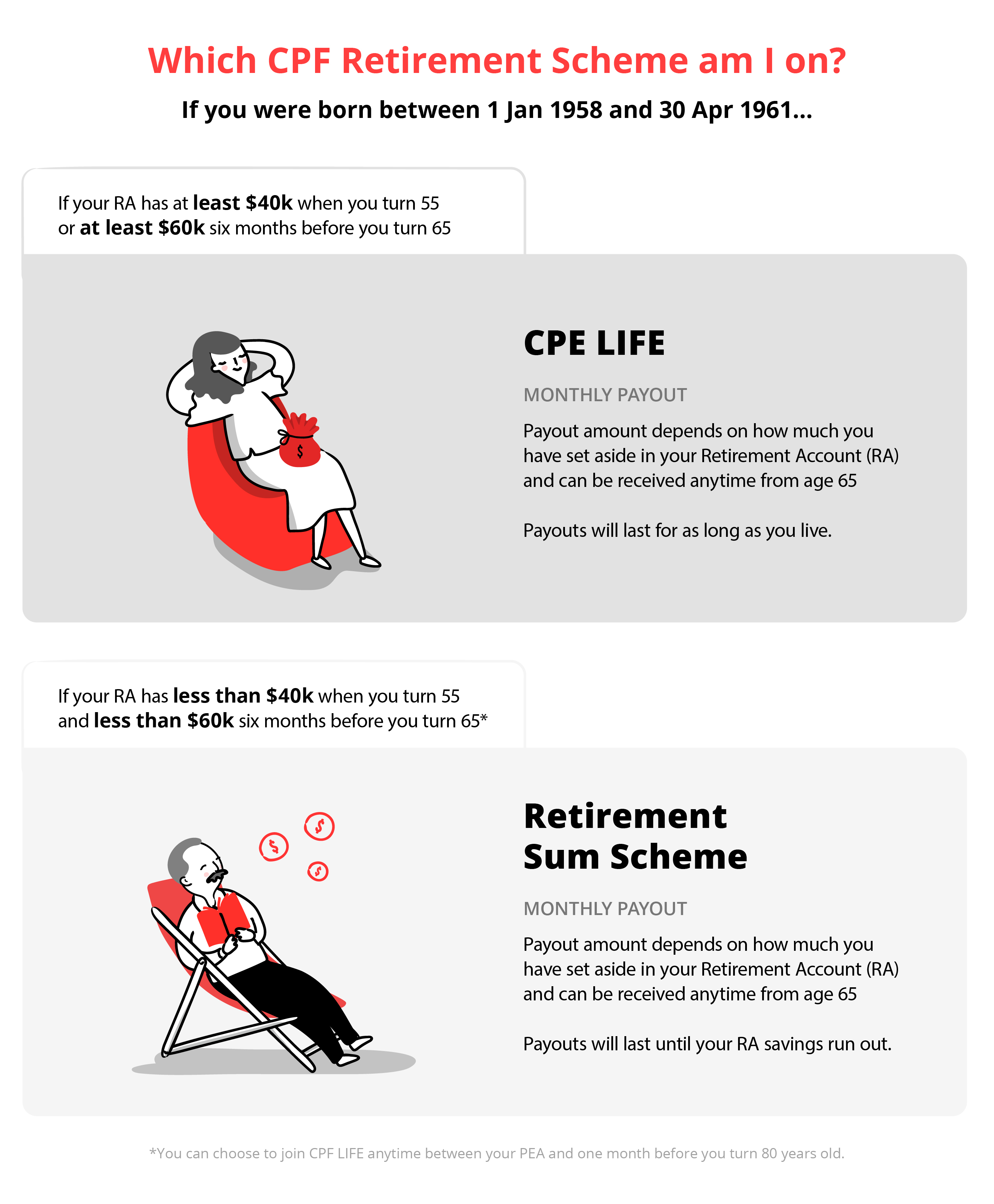

2. The Retirement Sum Scheme (RSS)

Before CPF LIFE came along, this was the default payout plan for retirees.

The Retirement Sum Scheme (RSS) is a simpler system. There’s no pooling of funds, no annuity premiums. Just monthly payouts from your Retirement Account (RA) savings — until they run out, or you turn 90. Whichever comes first.

How It Works

If you’re on RSS, your CPF simply pays you a monthly sum drawn from what’s in your RA. Once the savings are gone, the payouts stop. There’s no guarantee that the money will last your whole life.

This scheme mostly applies to:

-

People born before 1958

-

Those who don’t meet CPF LIFE’s minimum RA requirement ($60,000)

-

Non-citizens or non-PRs who don’t qualify for CPF LIFE

It still exists today, mainly for older cohorts or folks with lower CPF balances.

You May Be Interested

Understanding CPF Retirement Options: CPF LIFE vs. Retirement Sum Scheme (RSS)

Pros of RSS

| Advantage | What It Means |

|---|---|

| Straightforward | You get payouts directly from your RA, no annuity, no pooled interest. |

| Everything Stays Yours | Whatever is left — including interest — goes to your family when you pass on. |

| Limitation | Why It Matters |

|---|---|

| You Might Outlive Your Payouts | If your RA savings run out or you live past 90, there’s no more income from CPF. |

| No Lifelong Security | Unlike CPF LIFE, RSS doesn’t guarantee income for life. That’s a big trade-off. |

-

Older Singaporeans already on the scheme (Pioneer or Merdeka Generation)

-

Those with lower CPF balances who want to pass on whatever’s left

-

People with other income streams (rental, investments, family support)

It’s a decent option if you’re not depending solely on CPF for retirement. But if you expect to live a long time or want a reliable stream of income for life, RSS may not go far enough.

3. CPF LIFE – Lifelong Income for the Elderly

Launched in 2009, CPF LIFE is now the go-to retirement payout scheme for most Singaporeans. And for good reason — it pays you every month, for as long as you live.

That’s the main draw. You don’t have to worry about running out of money if you live into your 90s… or even past 100.

You May Be Interested

Best Early Stage Multiple Pay Critical Illness Plan Singapore 2025 [In-Depth Comparison]

How CPF LIFE Works

When you turn 65 (or choose a later start), a portion of your Retirement Account (RA) is used to pay a CPF LIFE premium.

That premium earns up to 6% interest, but here’s the catch: the interest goes into a shared pool. It’s how the system makes lifelong payouts sustainable for everyone, even those who live much longer than average.

Your payouts come from this pool, not just your personal balance. And when you pass away, any unused premium gets passed to your beneficiaries — but not the pooled interest.

So you’re trading inheritance potential for lifelong security. It’s not for everyone, but for many, it’s worth it.

Who’s Enrolled?

You’re automatically placed on CPF LIFE if:

-

You were born in 1958 or later

-

You have at least $60,000 in your RA six months before turning 65

-

You’re a Singapore Citizen or PR

Didn’t meet the criteria? You can still join CPF LIFE any time before turning 80.

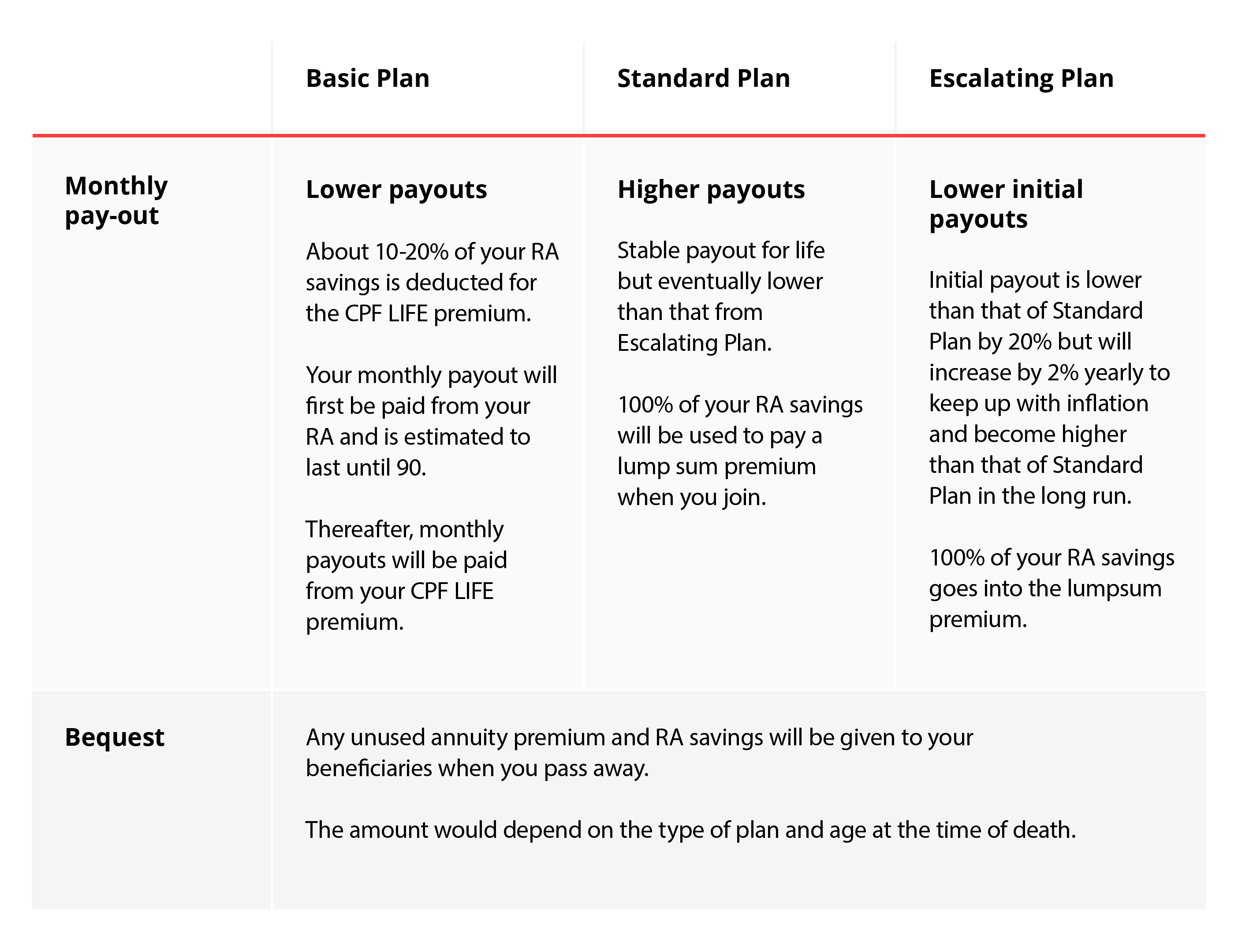

The Three CPF LIFE Plans

CPF LIFE isn’t one-size-fits-all. You can choose the plan that fits your priorities:

| Plan | Key Features | Best For… |

|---|---|---|

| Standard Plan | Higher, consistent payouts for life | If you want stable income each month |

| Basic Plan | Lower payouts, more money left for your loved ones | If leaving behind a legacy matters more |

| Escalating Plan | Payouts increase 2% every year | If you’re worried about rising costs over time |

Quick Example

-

Mr. Lim wants a steady income and no surprises. He picks the Standard Plan.

-

Ms. Tan wants to make sure her children receive more later on. She picks the Basic Plan.

-

Mr. Goh is worried about inflation eating into his expenses later. He goes for the Escalating Plan.

You can use the CPF LIFE Estimator online to run your own numbers. It’s helpful if you’re unsure which plan gives you the best fit.

You May Be Interested

Why CPF LIFE Works Well

| Benefit | Why It Matters |

|---|---|

| Lifelong Payouts | You’ll always have monthly income, no matter how long you live. |

| High, Risk-Free Interest | Premiums earn up to 6% — better than most savings accounts. |

| Flexible Start Age | You can start payouts anytime between 65 and 70. Later start = higher payouts. |

One Thing to Keep in Mind

CPF LIFE does not return interest earned on your premiums to your beneficiaries. It stays in the pool to support lifelong payouts for others.

That trade-off helps make the scheme work — but it’s important to know upfront.

4. CPF LIFE vs Retirement Sum Scheme (RSS): What Really Sets Them Apart

If you’re trying to decide between CPF LIFE and RSS, here’s where things get clearer.

Both are retirement payout schemes under CPF, but they’re built differently — not just in how they work, but in how they serve your goals.

Let’s break it down.

You May Be Interested

Singlife Smart Saver Plan Review: A Smart & Flexible Way to Save

1. How Long the Payouts Last

| CPF LIFE | RSS | |

|---|---|---|

| Lifespan Coverage | Monthly payouts for life — no end date. | Payouts stop at age 90 or when RA savings run out. |

Why it matters:

If you’re concerned about living into your 90s or beyond, CPF LIFE removes that risk completely. RSS might work if you expect a shorter retirement or have other income sources.

Source: CPF

Disclaimer: The monthly payouts provided are estimates based on the CPF LIFE Standard Plan for individuals turning 65 in 2034, as calculated in 2024. These payouts may be subject to adjustments to reflect long-term changes in interest rates or life expectancy. Any such adjustments, if made, are expected to be minimal and gradual.

2. What Happens to Your Interest

| CPF LIFE | RSS | |

|---|---|---|

| Interest on Savings | Earns up to 6%, but interest goes into a pooled fund to support all members. Your family only gets unused premiums. | You keep everything — including full interest. All remaining RA savings go to your beneficiaries. |

Why it matters:

RSS is better if you want to leave more behind. CPF LIFE prioritizes sustaining income for life, even if it means giving up the interest.

3. Who’s Eligible

| CPF LIFE | RSS | |

|---|---|---|

| Who Can Join | Auto-enrolled if: |

-

Born in 1958 or later

-

Have $60,000 in RA by 65

-

Singapore Citizen or PR | Mostly for:

-

Those born before 1958

-

People with under $60,000 in RA by payout age

-

Non-citizens or non-PRs |

Why it matters:

Most younger Singaporeans are now automatically placed on CPF LIFE. RSS is only available in certain cases — it’s more of a legacy option.

4. Can You Switch?

| CPF LIFE | RSS | |

|---|---|---|

| Flexibility | You can join CPF LIFE anytime before age 80. | Once on CPF LIFE, you can’t switch back to RSS. |

Why it matters:

If you’re on RSS and unsure, you still have time to opt in to CPF LIFE later. But once you switch over, it’s a one-way street.

Summary Table: CPF LIFE vs RSS

| Feature | CPF LIFE | RSS |

|---|---|---|

| Payout Duration | Lifelong | Until age 90 or RA runs out |

| Interest | Pooled (not passed to beneficiaries) | Fully passed to beneficiaries |

| Enrollment | Auto-enrolled (if eligible) | Legacy/default (for certain groups) |

| Switching | Can switch to CPF LIFE before age 80 | Can’t switch back from CPF LIFE |

Each scheme has trade-offs. It really depends on what you value more — lifelong income or preserving your CPF savings for your family.

5. CPF LIFE or RSS? How to Choose What Fits You

There’s no one-size-fits-all answer. The best scheme for you depends on how you see your retirement, what you already have in place, and what matters most to you.

Here are some questions to help you figure it out.

1. What Kind of Retirement Do You Want?

-

Do you see yourself living simply, spending minimally, maybe staying in your current home?

-

Or are you hoping to travel, enjoy hobbies, or spend more on lifestyle comforts?

If you expect to need more monthly income, CPF LIFE with a Full or Enhanced Retirement Sum could be a better fit. But if you have other sources of cash flow, RSS might already cover the basics.

2. Do You Have Other Sources of Retirement Income?

-

Own a property you plan to rent out?

-

Got savings, stocks, SRS, or other investments?

If yes, you may not need the security of CPF LIFE’s lifelong payouts. RSS could give you enough monthly support, and still allow you to leave more behind.

You May Be Interested

A Step-by-Step Guide to Applying for Letters of Administration in Singapore

3. Are You Planning to Leave Behind a Legacy?

If passing on your CPF savings to your children or spouse is important, RSS gives you more control. Your full RA balance — interest included — goes to your beneficiaries.

With CPF LIFE, only unused premiums are returned. The interest earned stays in the pool.

4. Do You Expect to Live a Long Life?

If you have good health and your family tends to live well into their 90s, CPF LIFE gives you peace of mind. Your payouts never stop, no matter how long you live.

On the other hand, if you don’t expect a long retirement — or prefer to make the most of your savings now — RSS may work better.

Practical Examples

| Case | Background | Decision |

|---|---|---|

| Mr. Wong, 65 | Owns a flat, no other income, worried about living a long time | Chooses CPF LIFE Standard Plan for guaranteed monthly income for life |

| Ms. Lim, 70 | Has $50,000 in RA, strong investments, wants to leave more behind | Stays on RSS to pass full savings (with interest) to her children |

| Mr. Tan, 65 | Set aside FRS, expects rising expenses due to health | Chooses CPF LIFE Escalating Plan for payouts that grow 2% each year |

| Mrs. Chen, 75 | On RSS, but savings are depleting faster than expected | Switches to CPF LIFE before age 80 to secure lifelong income |

Other Things to Think About

-

Do you worry about inflation? → Escalating Plan under CPF LIFE may help.

-

Do you have health concerns? → RSS might allow more flexibility upfront.

-

Do you want full control over your CPF money? → RSS is more transparent, and you keep all your interest.

In short, it comes down to priorities:

-

Security? → CPF LIFE

-

Simplicity and inheritance? → RSS

You May Be Interested

What Happens to a Deceased’s Bank Account After Death in Singapore?

6. Boosting Your CPF Savings

Choosing between CPF LIFE and RSS is one part of retirement planning. The other part? Making sure there’s actually enough money set aside to support the lifestyle you want.

If your CPF balance feels a little short of your goals, here are two tools that can help.

Retirement Sum Topping-Up Scheme (RSTU)

This is one of the most direct ways to grow your CPF savings.

You can top up:

-

Your Special Account (SA) — if you’re under 55

-

Your Retirement Account (RA) — if you’re 55 or older

You can also top up your loved ones’ CPF accounts — like your spouse, parents, or siblings.

Why It’s Worth Considering

| Benefit | What It Means |

|---|---|

| Higher Payouts Later | Every dollar you top up earns risk-free interest (up to 6%), which boosts your monthly payouts. |

| Compound Growth | The earlier you top up, the more time interest has to compound — especially powerful if you start young. |

| Support for Family | You can top up someone else’s account to help them build their own retirement savings. |

| Tax Relief | Cash top-ups may qualify for up to $8,000 tax relief (plus another $8,000 if you top up a family member). |

Just note: tax relief is subject to eligibility, income caps, and annual limits.

CPF LIFE Estimator Tool

If you’re not sure how much to top up — or what kind of payout you’re looking at — the CPF LIFE Estimator helps with that.

You enter:

-

Your age

-

Current CPF savings

-

Preferred retirement sum or payout target

And it shows you how much you can expect to receive under each CPF LIFE plan. You can also tweak the numbers to see how different top-up amounts change the payouts.

You May Be Interested

Example

-

Mr. Lee (age 40): Tops up $10,000/year for 15 years. By 55, it grows to over $250,000.

-

Mrs. Tan (age 55): Tops up $10,000/year for 5 years. By 65, it grows to around $60,000.

That’s the power of time and compounding. Start earlier, and the numbers work harder for you.

Wrapping It All Up

Your CPF is more than just a savings account — it’s your future monthly income.

Using tools like the Retirement Sum Topping-Up Scheme and the CPF LIFE Estimator can make a real difference. Topping up early grows your savings faster. And understanding your projected payouts helps you plan with clarity, not guesswork.

Small steps today can lead to a more comfortable retirement tomorrow — one with higher payouts, better peace of mind, and even tax perks along the way.

CPF LIFE or RSS — What Works for You?

Both schemes offer something different. Neither is “better” across the board — it really comes down to what matters to you.

-

CPF LIFE gives you income for life. That’s a huge plus if you’re worried about outliving your savings.

-

RSS is simpler. It lets you keep more control, especially if you plan to leave behind your CPF savings for family.

If your main concern is long-term stability, CPF LIFE probably makes more sense.

If you’re working with a smaller CPF balance, or want to leave behind more to loved ones, RSS might be the better fit.

Don’t Just Pick — Plan

Before you decide, take a step back and look at the big picture:

-

What kind of lifestyle do you see for yourself in retirement?

-

Do you have other assets or income outside CPF?

-

Are you thinking about family support — either giving or receiving?

-

How’s your health, and what’s your take on inflation?

These aren’t just financial questions. They’re personal ones. The answers can shape how you approach your CPF, your retirement goals, and the kind of life you’re planning for.

You don’t have to figure it out on your own.

If you want help making sense of it all — from payout projections to top-up strategies — we’re here.

Let’s talk. And let’s make your CPF work the way you need it to.

Final Thought

CPF LIFE and RSS aren’t just technical retirement plans — they’re tools. The real question is how you want to live, what safety nets you need, and how much you want to pass on.

Take your time to explore both options.

And if you’re unsure where to start, we’re here to help.

Want Help Planning Your Retirement?

Our advisors can walk you through CPF LIFE, RSS, top-ups, and everything in between. Whether you’re just starting or rethinking your approach, we’ll help you build a plan that works for your life.

Fill in the form below to speak with someone from our team.

Your future self will thank you for taking this step.