Last Updated on by Tree of Wealth

Subscribe to our Telegram & Email Newsletter for immediate updates!

About Best Investment- Linked Policy

There are many ILPs around and everyone would like to find the best investment plan in Singapore. Some comes with high insurance charges and are not suitable for investment purposes should your focus is on wealth growth.

Enter Investment focused ILPs. They are usually categorised with 101% of protection (as they are more investment focused) and there are indeed competitive 101% ILPs around with strong funds. Finding for the right one is not going to be easy, especially with the undergoing charges and returns and the many different start-up bonuses and loyalty bonuses that each insurer is going to give.

Retail and even Accredited Investor (AI) like Fundsmith fund is available on these platforms and it certainly attains higher returns. As always, when it comes to investment it is always non-guaranteed and returns are always matched with the risks.

That being said, 101% ILPs set out to minimise that risk by investing in longer time horizon to average the risk and steady the returns.

How 101% comes about is that in the event of death, 101% of the investment value will be paid out, as opposed to traditional 105% ILPs that takes into higher cost of insurances (as well as investing into sub-funds managed by insurers). This means that the 101% has more weightage into investment, yet providing assurance to policy holders that in the event of death, their investments are being protected for.

Also to note that even the same plan from the same insurer will also reflect the different bonuses that you will receive.

We have done the homework and below let’s have a comparison view on which plans are the most competitive!

Analyzing Breakeven Yield P.A. $1,000/month Comparison

|

3 years |

5 years | 10 years | 15 years | 20 years | 25 years |

30 years |

|

|

Singlife Savvy Invest |

2.53% | 2.13%

2.26% (Flexi) |

2.35%

2.39% (Flexi) |

NA | 1.00% | Na | NA |

| NA | NA | NA | 1.56% | 0.81% | 0.46% | 0.28% | |

| NA | NA | 1.89% | 1.03% | 0.71% | 0.56% | 0.48% | |

| TM Atlas Wealth | NA | 2.32% | 1.63% |

1.49% |

1.42% | 1.37% | NA |

| TM #goTreasures | NA | NA | 2.05% | 1.51% | 1.15% | 0.85% |

0.72% |

| FWD Invest First Plus |

NA |

NA | NA | 1.44% | 1.29% | 0.99% |

0.86% |

| NA | 1.91% | 1.49% | 0.72% | 0.48% | NA |

NA |

|

| NA | NA | 1.0% | 1.2% | 1.2% | NA |

NA |

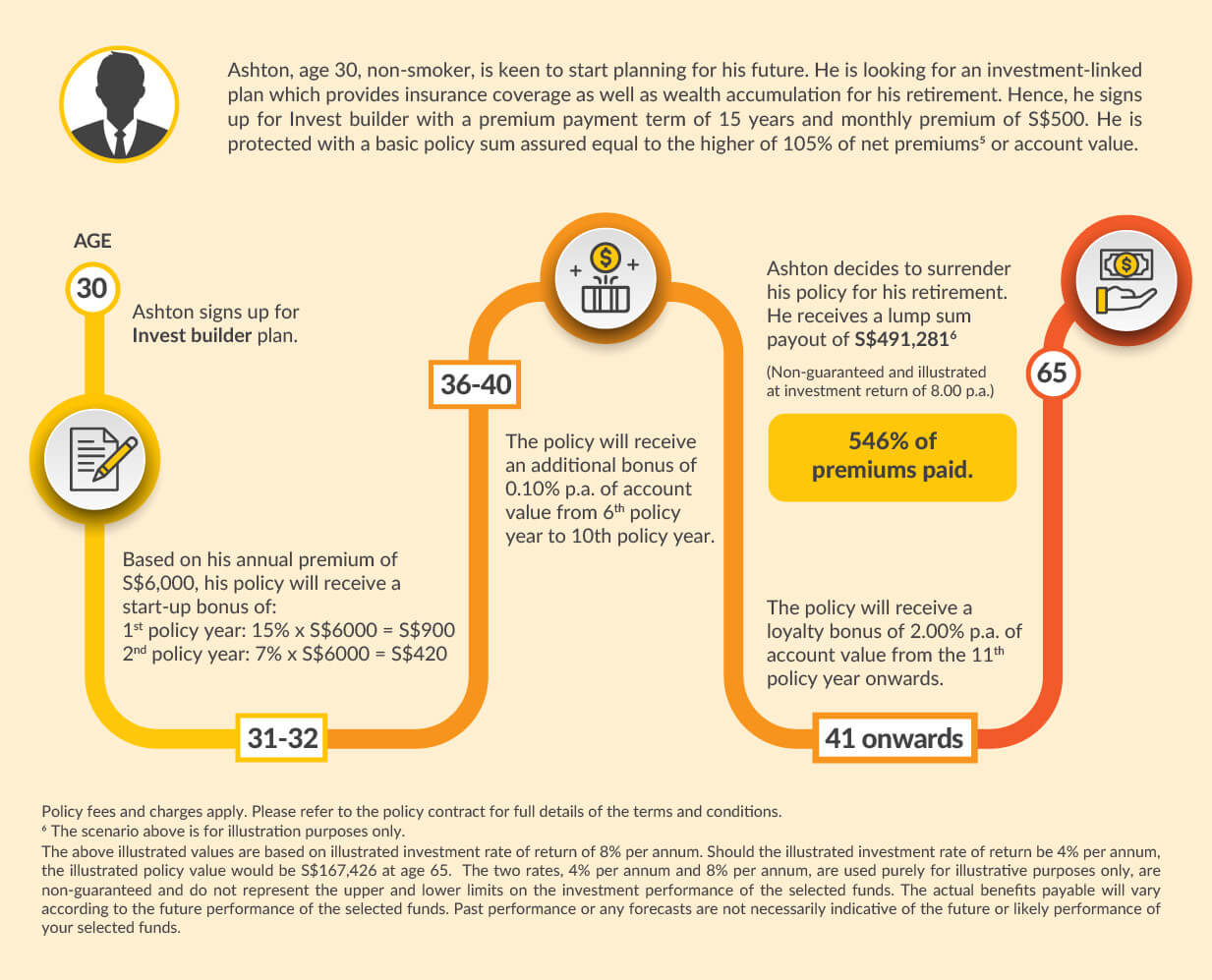

Etiqa Invest Builder

Strength

- Fundsmith Fund is Available!

Short term Investment (3 years Available / 5 years) - Portfolio Managed Funds

- Principal Guaranteed upon death throughout holding period

- 1x Withdrawal of 15% from Account value during life contingency event + Premium freeze 12 months

Weakness

- 2.30% p.a. charge throughout policy term (Till age 100)

How Etiqa Invest Builder Works

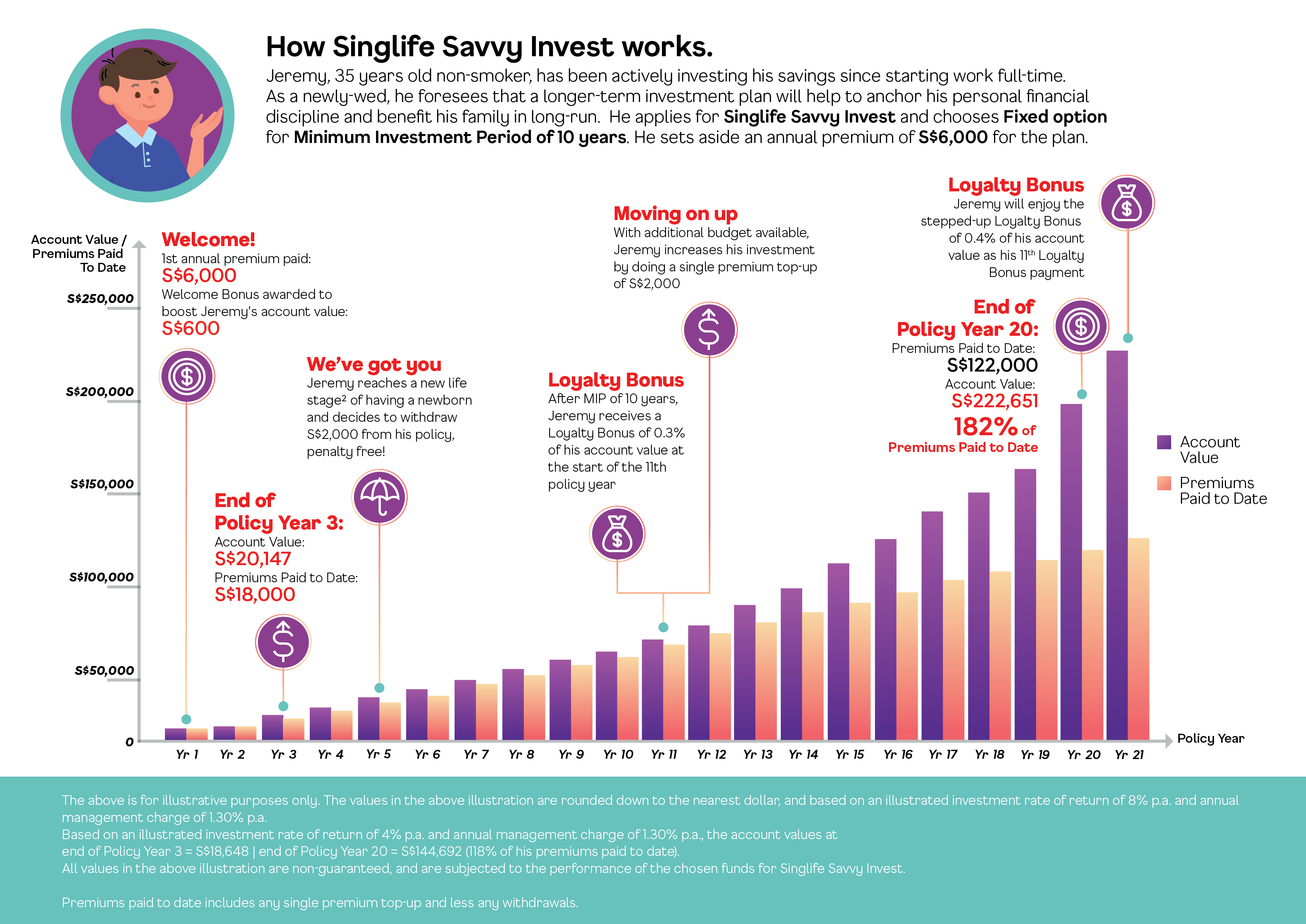

Singlife with Aviva Savvy Invest

Strength

- Short term Investment (3 years Available / 5 years Flexi)

- Restricted Funds

- Principal Guaranteed upon death throughout holding period

- 2x Withdrawal of 10% from Account value during life stages

- Fundsmith Fund

Weakness

- Flexi Option No Options to reduce premium to 0

How Singlife with Aviva Savvy Invest Works

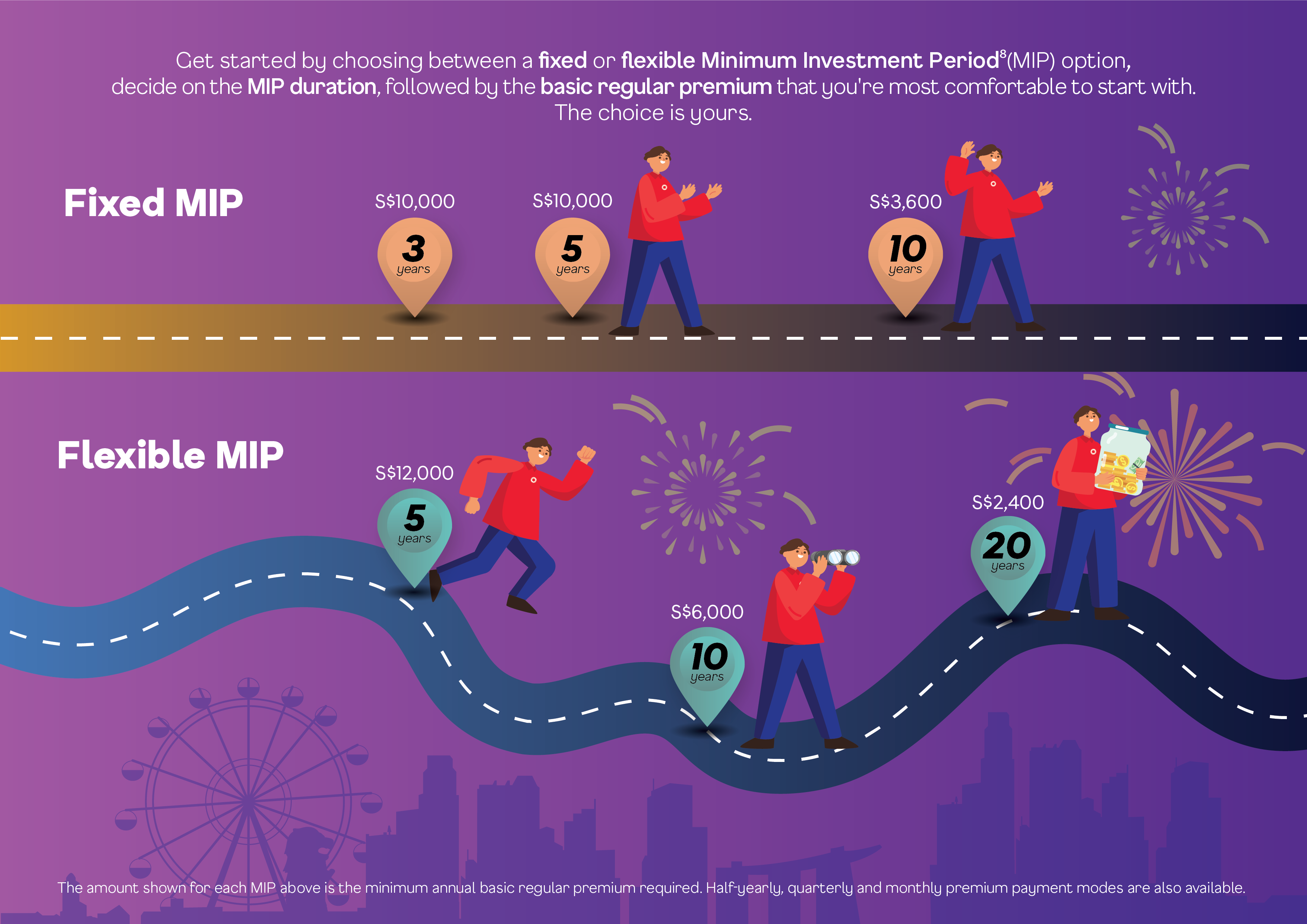

Tokio Marine TM Atlas Wealth

Strength

- Premium Flexibility after 1st year (Regardless of Payment Term) MIP 1 year only

- Access to Fundsmith

- Low Breakeven Yield 10 – 15 years Premium Term

- Range of riders to be added to waive premium e.g. cancer, spouse, eci waiver

- Advanced Death Benefit (Principal Guaranteed upon death during premium payment term)

Weakness

- Higher Breakeven yield Beyond 20 years

- No immediate dividends

- High Minimum Cash Outlay – $630/mth

How TM Atlas Wealth Works

Tokio Marine TM #goTreasures

Strength

- Premium Flexibility after 2 years (Regardless of Payment Term) MIP 2 years only

- Access to Fundsmith

- Lower Cash outlay for 20 years premium term – $300/mth

- Low Breakeven Yield from 15th year onwards

- Can be converted to auto unit deduction draw down after premium payment term

- Advanced Death Benefit (Principal Guaranteed upon death during premium payment term) + Secure Feature

Weakness

- No immediate dividends

- High Breakeven yield for 10 years

- High cash outlay for 10 / 15 years: $500 per month

- Lack of premium waiver riders

How TM #goTreasures Works

HSBC Life Wealth Harvest

Strength

- Minimum to start 300/mth

- Low breakeven yield beyond 15 years – 30 years (Extremely low from 20th year onwards) due to 0 Account Maintenance Fee from year 12th

- Access to Fundsmith Fund

Weakness

- No Flexibility for First 11 years

- No immediate dividends

- Lack of flexibility for first 11 years

- No Principal Guarantee upon death

How HSBC Life Wealth Harvest Works

FWD Life Invest First Plus

Strength

- Flexibility to Pause Premium Payments and Repay Later

- Get a Free Auto-Rebalancing Service for Your Investment Portfolio

- Access to Fundsmith Fund

Weakness

- Minimum Investment Period is 15 years

- Breakeven yield relatively higher

How FWD Life Invest First Plus Works

HSBC Life Wealth Abundance

Strength

- Enjoy two free partial withdrawals during MIP, with no withdrawal charge.

- Ad hoc withdrawals are possible from the 3rd year onwards and regular planned withdrawals are allowed after MIP.

- Ad hoc top-ups and recurring single premiums are permissible from the 13th policy month until the life insured turns 70 years old.

- The application process is hassle-free, with no medical examination required.

- Access to Fundsmith Fund

Weakness

- Only one premium term

How HSBC Life Wealth Harvest Works

Charges Breakdown

| Product | Policy Fees |

| TM Atlas | – 4% p.a. Initial Charge on First Year Premium ONLY During Premium Term (Total 5.5% p.a. inc policy charge)

– 1.5% p.a. Policy Charge on Total Policy Value throughout as long as policy is inforced |

| TM #goTreasures | – 5.4% p.a. Initial Charge on First Two Years Premium ONLY During Premium Term (Total 6.9% p.a. inc policy charge)

– 1.5% p.a. Policy Charge on Total Policy Value throughout as long as policy is inforced |

| Singlife Savvy Invest | – 0.65% p.a. Administrative Charge throughout

– 1.85% p.a. Supplementary Charge First Ten years |

| Etiqa Invest Builder | – 2.30% p.a. Policy Charge Throughout |

| HSBC Life Wealth Harvest | – 3.5% p.a. Account Maintenance Fee for first Eleven years |

| HSBC Life Wealth Abundance | – 2.10% p.a. Policy Charge of account value During Policy Term, 0.6% After. |

| FWD Life Invest First Plus | – 15 – 19 Premium Years: 1.8% p.a.

– 20 – 24 Premium Years: 1.4% p.a. – 25 – 29 Premium Years: 1.2% p.a. – 30 Premium Years: 1.0% p.a. |

Pure Investment Policies are recently picking up traction as they offer investors another platform of investment coupling with start up bonuses as well as loyalty bonuses and pure investment funds.

Here the ILPs shown are competitive in their own rights. With the different yields, minimum investment periods, bonuses, charges, funds availability and many other factors taken into consideration, it is important to know which plan is most suitable for you to match your investment horizon and needs.

To find the most suitable investment plan, simply fill in the form below and our friendly licensed FA advisor will get in touch with you. Based on your needs, a custom made solution will be adjusted only addressing your concerns.

No obligations, no hidden fees. All advice are of no charges.