Last Updated on by Tree of Wealth

The Central Provident Fund (CPF) is a cornerstone of Singapore’s social security system, designed to meet retirement, housing, and healthcare needs. With compulsory contributions from employers and employees, CPF balances grow over time, building a retirement nest egg with attractive interest rates.

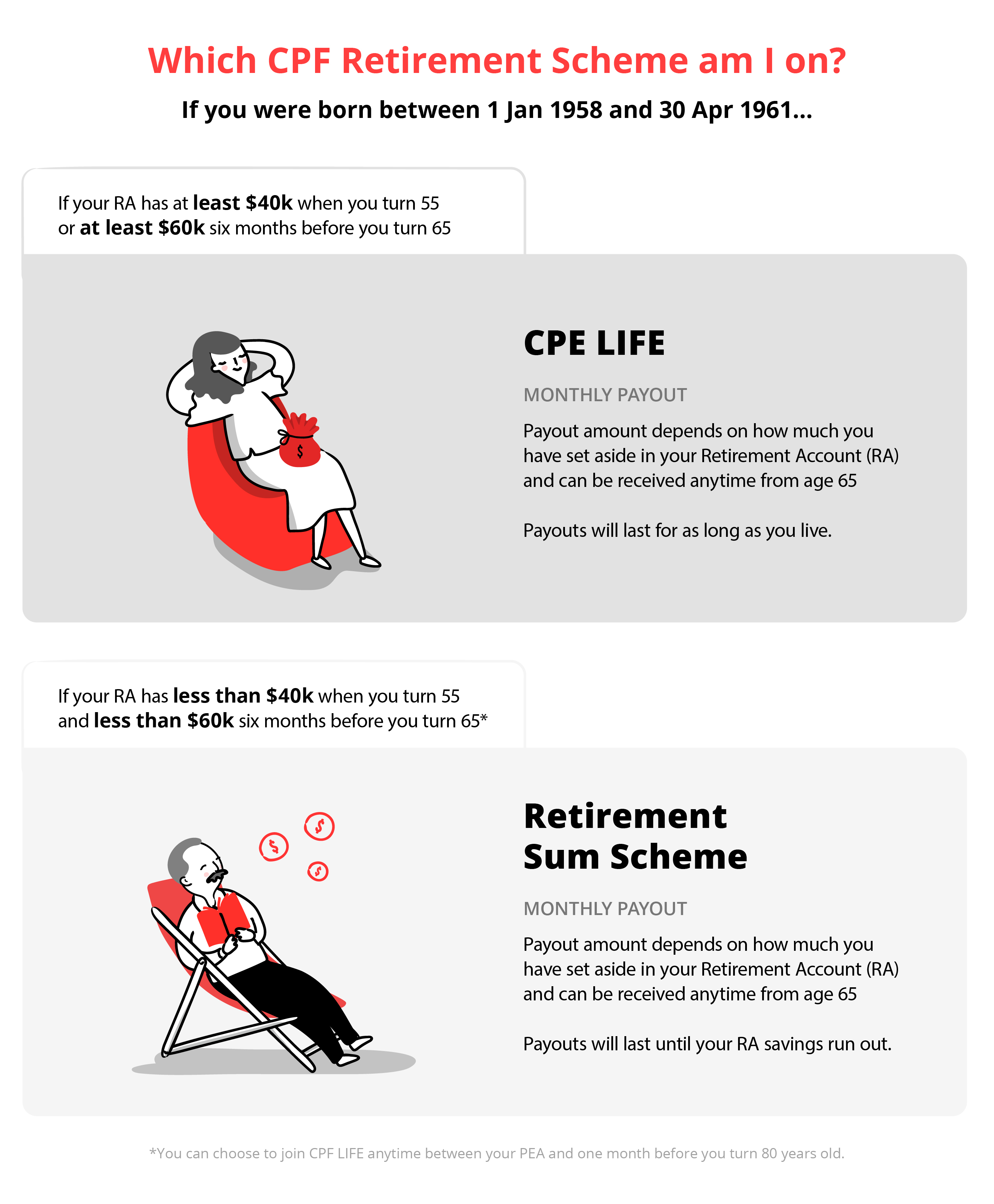

For retirement, Singaporeans can choose between two key options: the Retirement Sum Scheme (RSS) and CPF Lifelong Income for the Elderly (CPF LIFE). Most individuals today will be automatically enrolled into CPF LIFE, a national annuity scheme providing lifelong payouts. However, older Singaporeans born before 1958 may still be under the RSS.

This guide explains how these schemes work, their differences, and how to make the most of CPF tools like the Retirement Sum Topping Up Scheme (RSTU) to secure your dream retirement.

What is CPF Retirement Sum?

At the heart of CPF retirement planning lies the Retirement Sum, the amount of CPF savings you set aside in your Retirement Account (RA) to fund monthly payouts starting from your Payout Eligibility Age (PEA) at age 65.

There are three tiers of Retirement Sums to choose from:

- Basic Retirement Sum (BRS): For those who plan to supplement CPF payouts with other income sources or liquid assets.

- Full Retirement Sum (FRS): Double the BRS, offering higher monthly payouts.

- Enhanced Retirement Sum (ERS): The highest tier, for those seeking maximum monthly payouts.

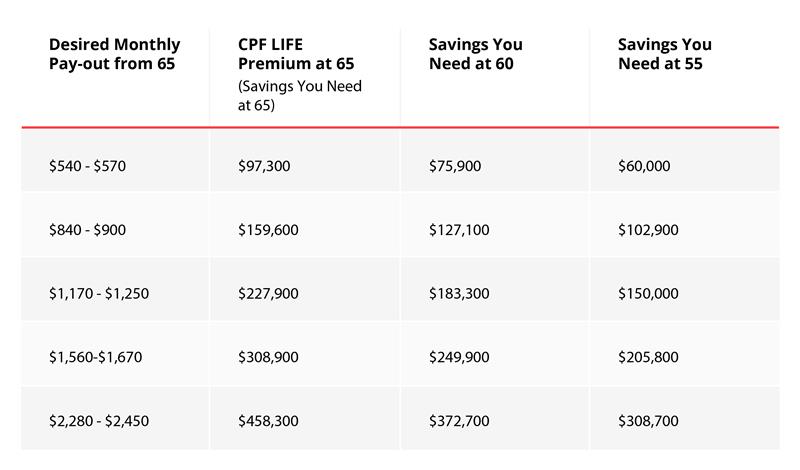

| Retirement Sum Tier | Savings to Set Aside (at 55) | Estimated Monthly Payouts (at 65) |

|---|---|---|

| Basic Retirement Sum (BRS) | S$99,400 | S$810–S$870 |

| Full Retirement Sum (FRS) | S$198,800 | S$1,520–S$1,650 |

| Enhanced Retirement Sum (ERS) | S$298,200 | S$2,240–S$2,490 |

*Figures are based on CPF LIFE Standard Plan for members turning 55 in 2024.

CPF LIFE vs. Retirement Sum Scheme (RSS)

1. Retirement Sum Scheme (RSS)

RSS provides monthly payouts to support basic living expenses during retirement. However, payouts stop when your RA savings are depleted or when you turn 90, whichever comes first.

Eligibility for RSS:

- Born before 1958.

- Born in 1958 or later but have less than S$60,000 in your RA when payouts begin.

- Non-Singapore citizens or non-permanent residents.

Key Features of RSS:

- Payout duration: Until age 90 or RA depletion.

- Remaining RA savings (including interest) are passed on to beneficiaries when you pass away.

2. CPF Lifelong Income for the Elderly (CPF LIFE)

CPF LIFE, launched in 2009, is Singapore’s national annuity scheme designed to provide lifelong monthly payouts, ensuring you never outlive your savings.

Eligibility for CPF LIFE:

- Born in 1958 or later with at least S$60,000 in your RA by six months before your PEA.

- Singapore citizens or permanent residents.

Key Features of CPF LIFE:

- Payout duration: For life, regardless of RA depletion.

- Remaining CPF LIFE premiums and CPF savings are passed to beneficiaries. However, accrued interest is pooled to sustain the annuity.

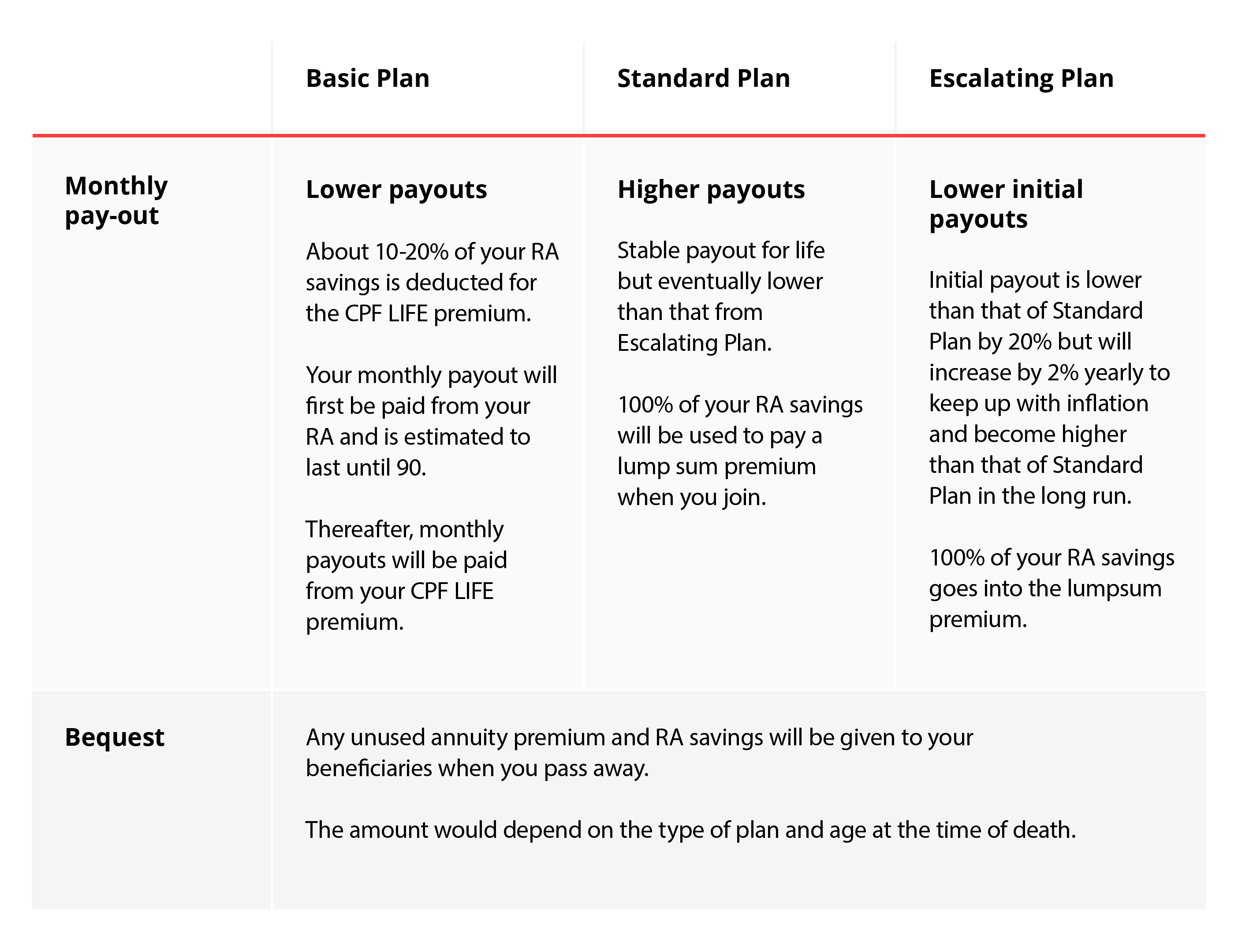

- CPF LIFE offers three plans: Standard, Escalating, and Basic, tailored to different payout preferences.

| Plan | Payout Amount | Payout Growth | Bequest Amount |

|---|---|---|---|

| Standard Plan | Moderate | None | Moderate |

| Escalating Plan | Lower initially | 2% annual increase | Lower |

| Basic Plan | Lowest initially | None | Highest |

Source: CPF

Differences Between CPF LIFE and RSS

| Feature | CPF LIFE | RSS |

|---|---|---|

| Payout Duration | Lifelong payouts | Until RA depletion or age 90 |

| Bequest | Remaining premiums + CPF savings | RA balance (including interest) |

| Interest Usage | Pooled for sustaining annuity | Distributed to beneficiaries |

Retirement Sum Topping Up Scheme (RSTU)

For those looking to boost their CPF savings, the Retirement Sum Topping Up Scheme (RSTU) is a great option.

Key Features:

- Top up your Special Account (SA) before 55 or RA after 55 with cash or CPF transfers.

- Cash top-ups earn up to S$8,000 in annual tax relief, with an additional S$8,000 for top-ups to loved ones’ accounts.

Limits:

- Top-ups are allowed up to the Full Retirement Sum (FRS) before 55 or Enhanced Retirement Sum (ERS) after 55.

Example:

Topping up S$50,000 to your SA at 55 can grow to over S$70,000 by age 65, thanks to CPF’s risk-free interest rates of up to 6%.

Questions to Consider

When planning your retirement with CPF, ask yourself these key questions:

- What retirement lifestyle do I envision?

- A modest lifestyle might only require BRS payouts, while FRS or ERS may be better for a more comfortable lifestyle.

- How will my home play into my retirement?

- Consider renting, downsizing, or unlocking equity through schemes like the Lease Buyback Scheme.

- Do I plan to live with family?

- Shared expenses can reduce the need for higher monthly payouts.

Wrapping Up

Understanding the differences between CPF LIFE and RSS is essential for tailoring your retirement strategy. CPF LIFE ensures lifelong financial security, while RSS offers flexibility for those who may not meet CPF LIFE’s criteria.

For additional flexibility, consider leveraging the Retirement Sum Topping Up Scheme to boost your savings and enjoy tax relief. Regardless of your choice, planning early and aligning your strategy with your desired retirement lifestyle is key.

Ready to start?

Fill out the form below to connect with a financial advisor and create a personalised CPF retirement strategy today!