Last Updated on by Tree of Wealth

Singapore is one of the most expensive cities in the world and with the new GST rate of 9% coming in the future, it is bound to get more expensive.

When it comes to savings, a general lamentation towards it is that savings plans tend to be very long term. There are a couple of mid term savings plan in the market and they do give decent returns, as insurers are constantly adjusting and gearing their products to suit market needs. To prevent yourself and your family from suffering from an affordability crisis, here are some savings plan that can allow you to save mid term without incurring unnecessary risks.

Head to Head Analysis 12 Year Savings Plan

Suppose David, a male non-smoker who will turn 31 on his next birthday and is considering either Singlife with Aviva MyEasySaver or AIA SmartGrowth(II). In the table below, we present you the various benefits he gets under each of these plans.

|

|

Singlife with Aviva

Singlife Steadypay Saver |

AIA

SmartGrowth(II) |

|

Sum Assured |

$35,000 | $35,000 |

|

Premium term |

12 |

12 |

| Policy term | 12 |

18 |

|

Annual Premium |

$5,068 | $2,861.95 |

| Maturity Amount | $38,500 (Guaranteed)

$49,501 (Projected at 4.75% return) |

$35,000* (Guaranteed) $50,368* (Projected at 4.75% return) |

|

Cash Benefit Rate of Return Accumulated |

0.84% (for investment returns of 3.25%

2.18% (for investment returns of 4.75%) |

Not applicable |

| Cash Benefit Rate of Return: Paid Out | 0.62% (for investment returns of 3.25%)

1.92% (for investment returns of 4.75%) |

Not applicable |

|

Total cash benefits withdrawn |

$15,750 | Not applicable |

|

Death benefits (Cash Benefit Paid Out Option) |

$43,924 (Guaranteed)

$54,925 (Projected at 4.75% return) |

$35,000 (Guaranteed) $50,368 (projected) |

|

Total Premium |

$60,816 |

$27,636 |

* = Maturity amount for AIASmartGrowth will be paid after 18 years.

Policy Highlights & Comparisons

Singlife Steadypay Saver

What we like

- Highest guaranteed maturity amount –Aviva MyEasySaver plan offers a guaranteed maturity amount of $38, 500 which is higher than the maturity amount offered by AIA. Take note this is because of the lowest overall cash benefit withdrawn.

- Highest guaranteed deathly benefits –Aviva MyEasySaver plan leads the way in offering the highest guaranteed death benefits, totaling to $43, 924. This is 25% higher than the guaranteed death benefits offered by AIA.

- Slightly more flexible – Aviva MyEasySaver plan offers you more flexibility compared to others by offering its users to avail cash benefits by the end of second policy year. This can keep your savings more liquid and help you keep cash for an emergency.

- Highest death benefits – Aviva’s death benefits are also more generous than that of its peers. Given its premium, the death benefits Aviva shells out makes this plan an extra boost in coverage for people whom are looking to save.

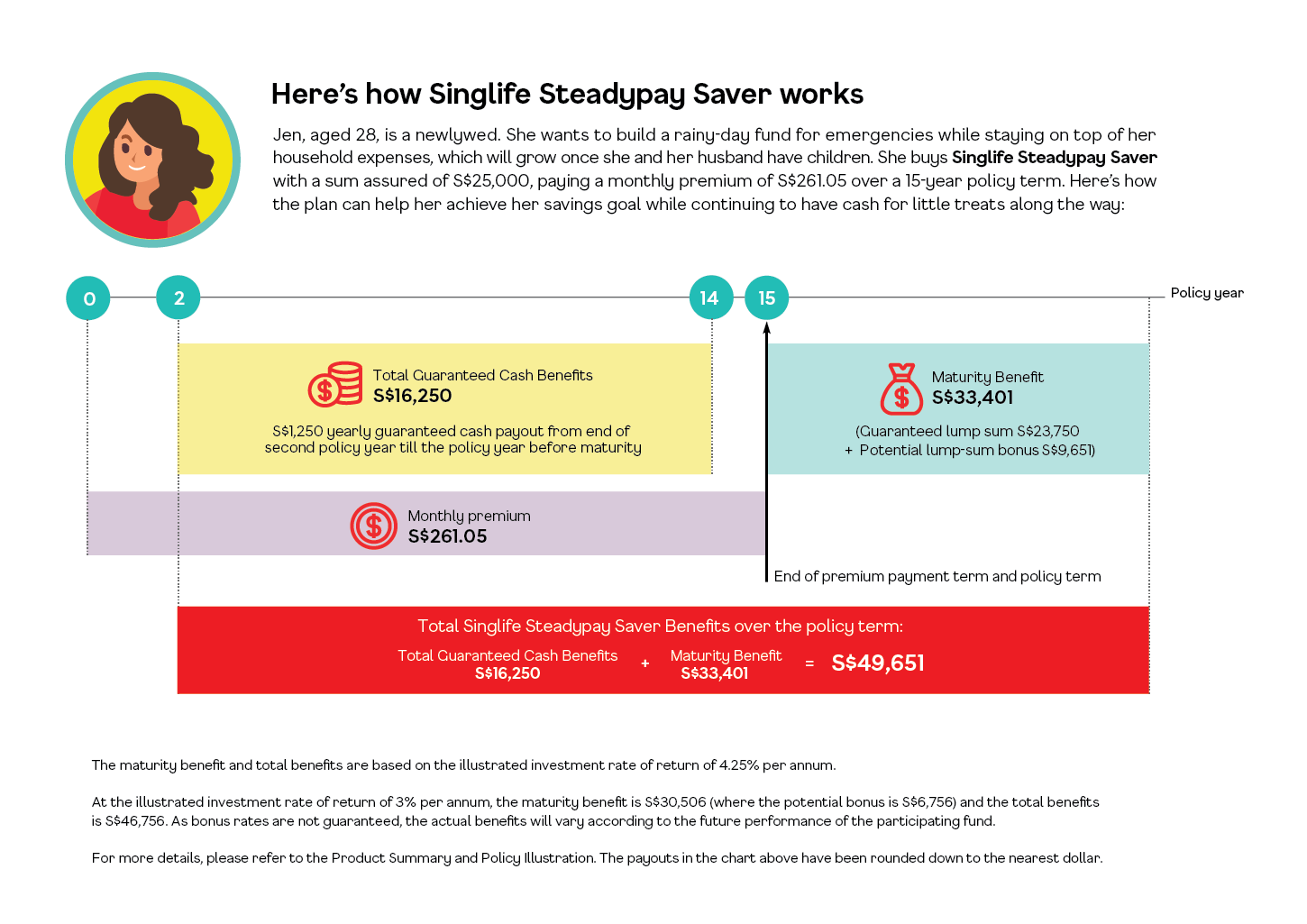

How Singlife Steadypay Saver Works

What we don’t like

- Expensive premium – While Aviva MyEasySaver plan offers attractive benefits, it charges an extremely hefty premium. For a 12 year window, the total premium $60,816 paid is almost double the premium paid for AIA SmartGrowth(II). If costs are an important factor for your consideration, this plan might not be right for you because of the sheer size of premium coupled with the duration through which you have to pay it.

- Minimal cash benefits – For a plan that charges such expensive premium, the cash benefits offered by Aviva MyEasySaver plan are quite dismal. With a mere $15,750 given in cash benefits, this plan fails in giving attractive schemes that makes life easier for users.

AIA SmartGrowth (II)

What we like

- Cheapest premium – Compared to its peers, AIA SmartGrowth offers the cheapest premiums by a long shot. Its annual premium at $2,861.95 is approximately less than half the annual premium for Aviva. This makes this plan quite cost friendly. If you’re someone who doesn’t prefer to spend a lot of money on savings plan at one go, this could be the right plan for you for a 12 pay 18 plan (limited pay).

What we don’t like

- Longest policy term –While AIA’s plan might be cheaper, you’d have to be very patient to enjoy some of its benefits given that the policy term is a surprising 18 years. There are two other options of 21 and 24 years policy term. This could really make this plan inconvenient for a lot of users who believe they can get better returns over such long period in the financial markets. If you’re someone who doesn’t prefer or doesn’t have the patient to wait for your returns on such long-time horizon, this plan might not be right for you.

- No option for cash benefit withdrawal – Another huge drawback of this plan is that it doesn’t offer its users the flexibility of availing cash benefits after certain periods of time. What this means is that the money you’ll be putting in this plan will be locked away throughout the duration of this plan. If you’re someone who wants to allow or some money on the side in cases of emergency, this clause might be worth looking into further.

- Lowest Returns – Although AIA’s maturity figure amounts at $50, 368 (assuming 4.75% return), while they seem higher than the maturity amount offered by Singlife with Aviva, keep in mind that AIA’s plan is 18 years in this scenario, as well as no cash benefit has been withdrawn at all, with Singlife with Aviva’s cash benefit have been withdrawn every single available year. Not to mention AIA’s investment returns in the past has been a rocky one, so take this with a pinch of salt because it is projected at a high return

Conclusion For Singlife Steadypay Saver VS AIA SmartGrowth(II)

All 3 plans here have one thing in common: they are of mid term of around 12 years. We hope the analysis helps you in understanding the pros and cons of these 3 mid term savings plans in the market so that you can decide if any of these options meet your savings objectives. All savings plans have their own advantages and disadvantages. We recommend that all individuals choose their savings plans keeping in mind their objectives and liquidity needs to ensure they get the best possible value.

Fill in the form below and our friendly licensed FA advisor will get in touch with you. Based on your needs, a custom made solution will be adjusted only addressing your concerns.

No obligations, no hidden fees. All advice are of no charges.