Last Updated on by Tree of Wealth

Medical costs keep rising and serious illnesses are increasingly common. i-CompleteCare is a limited-pay whole-life policy designed as a simple, long-term protection core: it pays out for death and terminal illness, provides disability cover, offers broad Critical Illness (CI) protection across early → advanced stages, and gives a longevity cash benefit at age 99. It’s designed to close protection gaps without forcing you to manage multiple single-purpose policies.

Why this matters (quick)

-

Claims for death, TPD and CI rose from S$1.6B → S$1.94B (2022–2024) (LIA). CI remains underinsured.

-

Roughly 1 in 4 Singaporeans may be diagnosed with cancer in their lifetime — wide CI cover helps reduce the financial shock.

What the plan covers

Full life & disability protection (death & TPD)

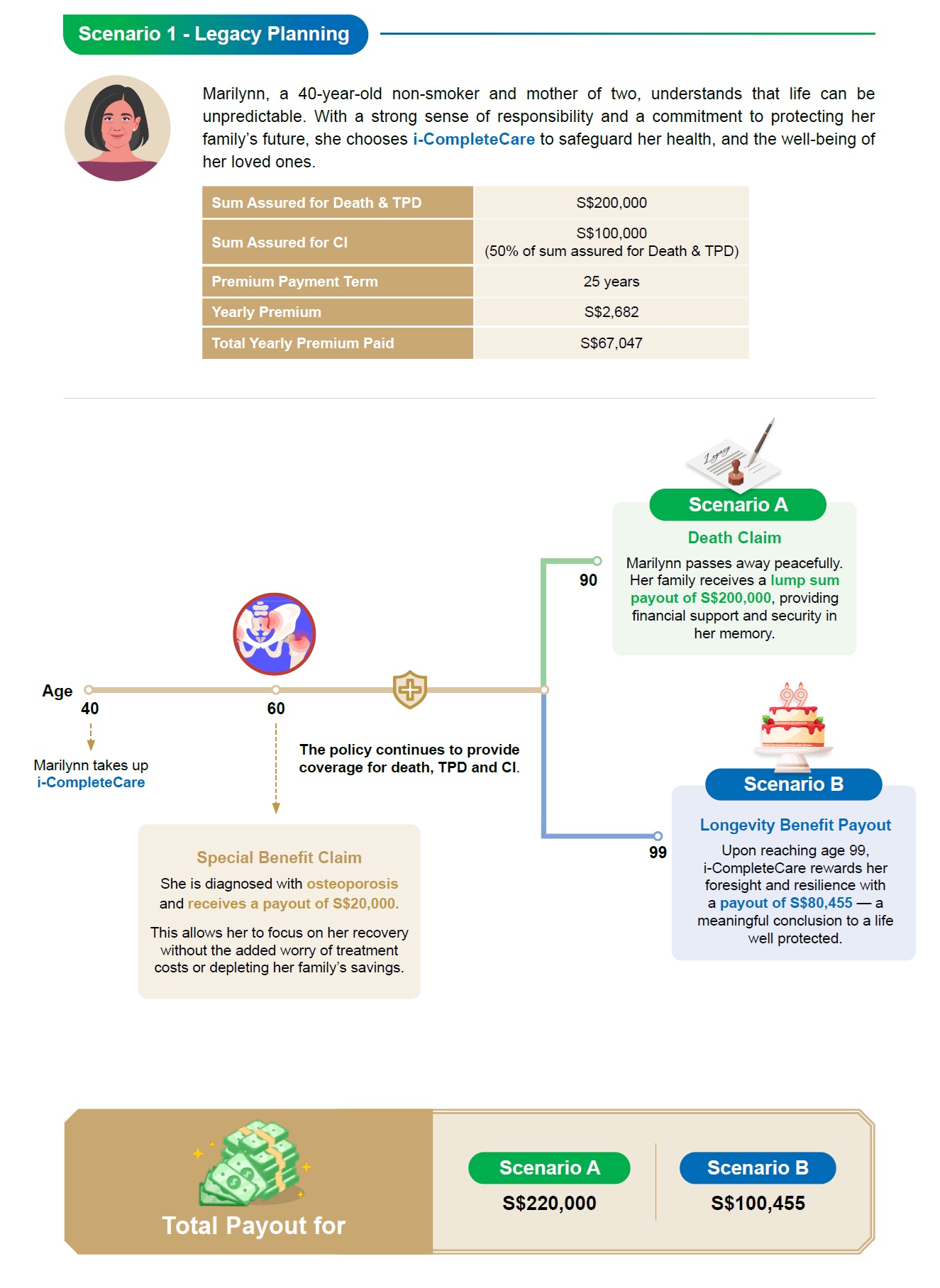

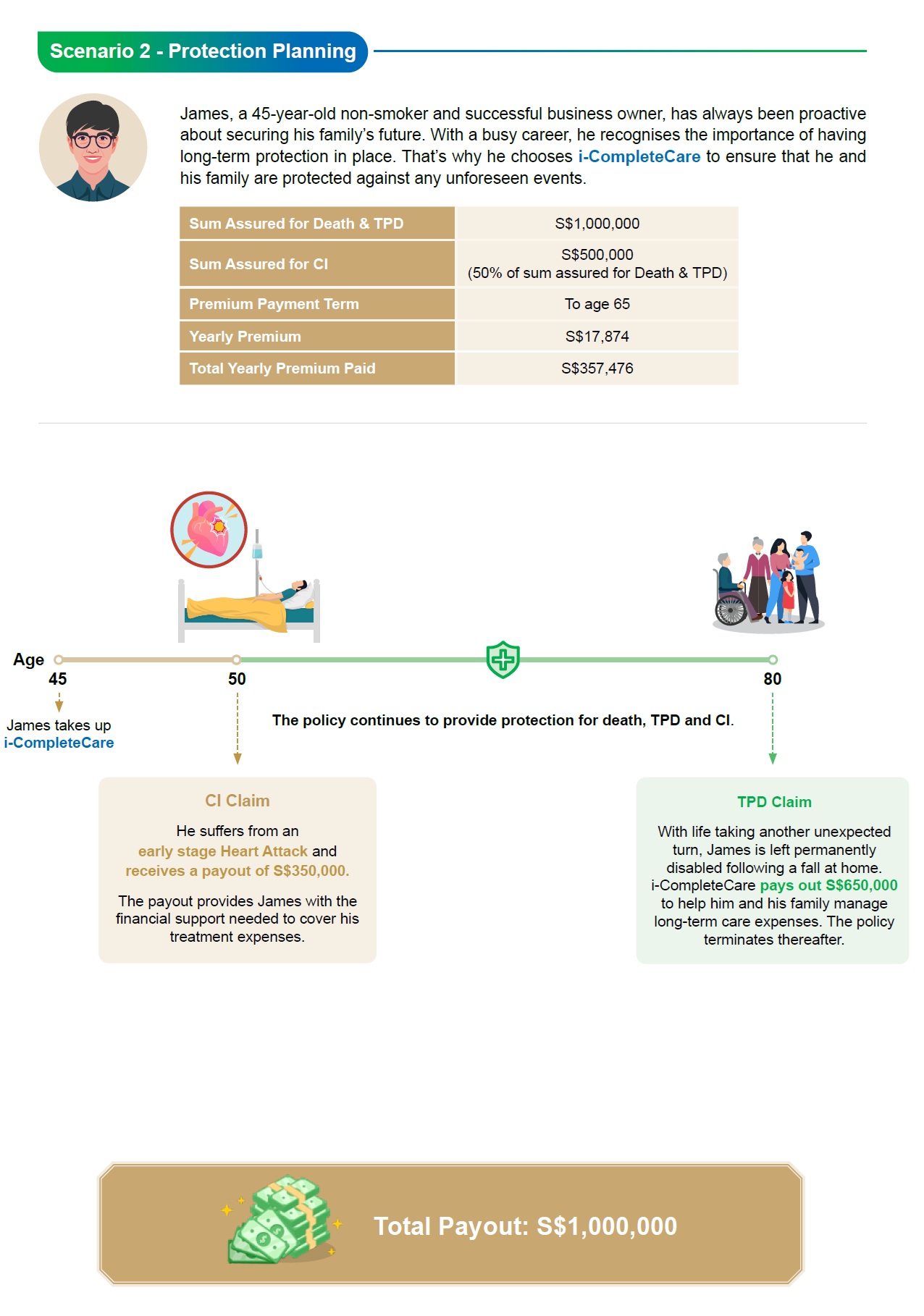

If the insured dies or suffers Total & Permanent Disability (TPD) that meets the policy definition, the plan pays the full sum assured to the policy beneficiaries. People typically use this payout to clear debts (e.g., housing loans), replace lost income for dependants, or top up living and medical expenses. Claims for death and TPD follow the standard underwriting and claims definitions in the policy—your adviser can show exact wording so you know what events qualify.

Stage-based Critical Illness cover (early → advanced)

The plan provides CI protection across the spectrum — from earlier diagnosis stages to severe, late-stage illnesses. When a valid CI claim is made under an eligible early and intermediate stage, the policy pays 50% of the sum assured for that claim (subject to policy definitions and survival/waiting rules). Because early-stage payouts are designed to help you act quickly (second opinions, early treatment, income support), they can be particularly useful for stepping in before major medical bills or prolonged work absence build up.

Special-condition top-up (15 named conditions)

For 15 specific conditions listed in the policy, you get an extra lump sum equal to 20% of the CI sum assured — subject to per-condition caps. These “Special Benefit” payouts are intended for conditions that often need extra or ongoing support (for example, certain cancers or organ-specific events listed in the product summary). Importantly, these special-condition payouts are handled under their own rules (per-condition limits apply) and do not automatically reduce your main CI or death sum assured — check the product summary for the exact list and per-claim limits.²

Longevity cash benefit at age 99

If the policy is still in force at age 99, it pays a one-off benefit equal to 120% of the total yearly premium paid at that time. Think of this as a small financial tail — a predictable cash event late in life that can be used for retirement top-up, long-term care, or simply as a legacy to family. The exact timing and payment mechanics are set out in the policy contract.

You can add riders that waive future premiums if the policy payer becomes totally and permanently disabled (or meets other rider trigger conditions described in the rider wording). When activated, these riders keep the core coverage intact without further premiums from the payer, so claims and benefits remain available to the insured and beneficiaries while premiums are suspended under the rider rules.

How The i-CompleteCare Works

Quick note on limits and overlaps (how claims interact)

-

Some payouts (standard CI and TPD) reduce the remaining death sum assured — this affects the balance left for later death claims.

-

Special-condition payouts are treated differently under the policy and can have their own limits and claim counts (for example, the Special Benefit may not reduce the main CI or death sums).

-

Aggregate caps apply for CI across insurers and across stages (see product footnotes for the S$350,000 per CI early+intermediate cap and the S$3,000,000 maximum across all stages).

Why limited-pay whole life?

Limited-pay means you pay premiums for a defined period (e.g., 20 or 25 years or up to age 60/65) but remain covered for life. That helps lock in protection while you’re earning and reduces long-term premium headache later in life.

Who this is for

-

Families who want a single, long-term protection base covering both life and CI risks.

-

Professionals or business owners concerned about income disruption from serious illness.

-

Anyone wanting to close the CI coverage gap without juggling multiple policies.

How to fit it in your plan

Treat i-CompleteCare as your protection anchor. You might:

-

use it as a base and add shorter-term income replacement or hospitalisation covers if needed; or

-

compare it to combinations such as level-term life + standalone CI to see which mix gives the best cost/benefit for your age and dependants.

Quick FAQ (micro answers)

Q: Will CI claims reduce the death benefit?

A: Yes — standard CI and TPD payouts reduce the remaining death sum assured. (Special Benefit payouts have specific rules — see footnotes.)²

Q: What payout will I get at age 99?

A: A longevity benefit equal to 120% of your total yearly premium paid at that time.

Q: Can I stop premiums after the limited pay term?

A: You stop paying after your chosen limited-pay term but the policy remains in force for life.

Q: Is coverage automatic under any protection scheme?

A: This policy is protected under the Policy Owners’ Protection Scheme administered by SDIC (coverage limits apply).

What’s Next?

Ready to see how i-CompleteCare works for you?

Fill in the contact form below and we’ll prepare a quick, no-obligation illustration showing estimated premiums, benefit scenarios and easy comparisons — one of our advisors will then reach out by WhatsApp or call to walk you through the numbers. We respect your privacy and won’t hard-sell; this is just a clear, personalised view to help you decide.