Last Updated on by Tree of Wealth

Planning for your retirement is a daunting task, and there are many factors to consider when planning for your golden years. This makes it important to understand CPF LIFE, which is the default retirement plan for Singaporeans.

This is where CPF Lifelong Income For the Elderly (CPF LIFE) comes into play. CPF LIFE is a national insurance scheme that provides retirees with monthly payouts no matter how long they live.

CPF LIFE holds significance since the duration of our lifespan is uncertain. Our retirement savings may fall short if we live longer than expected. With the continuous progression of medical technology, people are living longer, and it’s crucial to enjoy our later years without financial distress.

CPF LIFE addresses this concern by providing lifelong payouts, irrespective of our age, thus guaranteeing financial security during old age.

This article delves into what exactly CPF LIFE is, and how each of the different plans under it works.

What is CPF LIFE?

The Singaporean government has established CPF LIFE (Lifelong Income For the Elderly), an insurance program designed to offer regular payouts every month to individuals aged 65 and above for the entirety of their lives. This initiative aims to provide protection against inadequate retirement savings as studies reveal that Singaporeans are living longer. Unlike a typical Retirement Account, which only disburses monthly payouts until it’s depleted, CPF LIFE guarantees consistent payouts even after your savings have been exhausted.

When you join the CPF LIFE scheme, you need to pay a lump sum premium, deducted from your Retirement Account (RA), and the retirement payouts will continue, no matter how long you live.

You will be automatically included in the CPF LIFE scheme if you fit these criteria:

- Singapore Citizen or Permanent Resident

- Born in 1958 or after

- Have at least S$60,000 in your retirement savings before you reach 65

If you have not been enrolled into CPF LIFE, you are still able to opt in anytime from age 65 to 79.

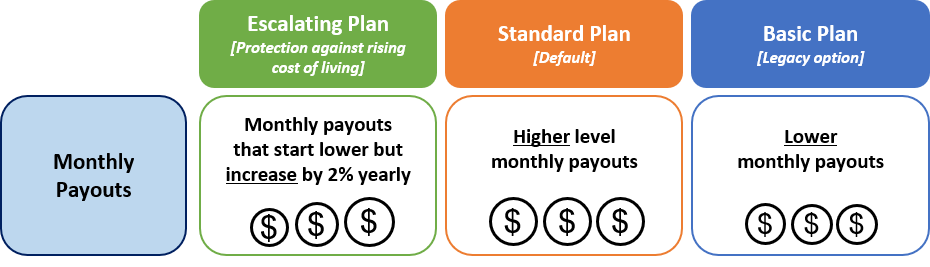

There are three plans under the CPF LIFE scheme – the Escalating Plan, Standard Plan, and Basic Plan.

Each of the three CPF LIFE plans share common features. First, they will provide you with a monthly payout no matter how long you live.

Next, your RA savings will be used to fund the CPF LIFE premium for your CPF LIFE plan. These premiums will earn you CPF interest rates of up to 6%, and includes extra interest of up to 2% from the Government.

Lastly, when you pass away, your beneficiaries will receive your CPF LIFE premium balance, together with any remaining CPF savings.

However, the intricacies of each plan is different, and each plan provides different types of monthly payouts to people with different retirement needs, and will be explained in the following sections.

CPF LIFE: Eligibility and Opt-Out Options

If you’re a Singaporean Citizen (SC) or Permanent Resident (PR) born in 1958 or later and have at least S$60,000 in your CPF Retirement Account (RA) before you turn 65, you will be automatically enrolled in CPF LIFE at age 65.

For those born between January 1, 1958, and April 30, 1961, you will also be enrolled even if you have only S$40,000 in your RA account by age 55. However, those over 80 years old are ineligible to join CPF LIFE if they haven’t already been included.

Individuals who don’t qualify for automatic enrollment (e.g., those with less than S$60,000 in their RA account) may still choose to join CPF LIFE, although their payouts may be lower and may not be enough for their monthly needs. Opt-out options are available for those who do not wish to participate in CPF LIFE.

The CPF LIFE program can be declined through two options. First, an individual can provide evidence of an equivalent program, such as a pension or annuity policy that offers payouts at a similar or greater rate than CPF LIFE. Second, an individual may not qualify for CPF LIFE if their RA account balance is less than S$60,000. In such cases, they may opt-out of the program.

How does it work?

When Singaporean Citizens (SCs) and Permanent Residents (PRs) reach the age of 55, a Retirement Account (RA) is established using their savings from the Ordinary and Special CPF accounts. The RA provides monthly payouts for retirement, but once it’s depleted, there will be no further payouts.

To address this issue, CPF LIFE was introduced as an insurance scheme. The premiums for CPF LIFE are paid from the Retirement Account, and in turn, CPF LIFE provides a monthly payout. The Singaporean government guarantees a 4% base growth rate for any premiums paid into CPF LIFE.

Premiums paid into CPF LIFE are invested in Special Singapore Government Securities (SGSS), which are wealth growth instruments managed by the government. The interest earned from the investment is factored into the monthly payout.

CPF LIFE offers three plan levels: Basic, Standard (the default option with a higher monthly payout than Basic), and Escalating (allowing a 2% annual increase in payouts to combat inflation). The increase in payouts under the Escalating plan is not linked to actual inflation to maintain stability.

CPF LIFE Basic Plan

CPF LIFE is an insurance scheme designed by the Singaporean government to provide lifelong payouts for individuals who have insufficient retirement savings. However, the amount of payouts received depends on the plan selected and the total amount of CPF savings across all accounts.

The Basic Plan is an option that provides lower monthly payouts than the CPF Escalating and CPF Standard plans. This makes it a suitable option for individuals who have lower spending needs or have additional sources of retirement income.

However, it’s important to note that the monthly payouts under the Basic Plan will reduce further when your combined CPF balances across all accounts eventually fall below S$60,000. This happens as the extra interest earned on the first S$60,000 of your combined CPF balances is credited to the Retirement Account and paid as part of the monthly payouts. Thus, when balances fall below S$60,000, payouts will decline accordingly.

Upon joining CPF LIFE, about 10 to 20% of your Retirement Account savings will be deducted as CPF LIFE premium. The payouts will persist until the individual’s death, and any remaining CPF savings and premium balances from CPF LIFE will be transferred to the nominated beneficiaries.

In summary, the Basic Plan provides lower monthly payouts, making it suitable for individuals who have lower spending needs or have additional sources of retirement income. However, the payouts will decrease further when CPF balances fall below S$60,000.

CPF LIFE Standard Plan

The CPF LIFE Standard Plan is a great option for those who prioritize consistency in their retirement payouts. Unlike the CPF LIFE Escalating Plan, which offers payouts that increase by 2% each year, the Standard Plan offers level payouts that remain the same for the rest of your life. This makes it a suitable option for individuals who are willing to adjust their spending as prices rise due to inflation.

While the Standard Plan’s payouts start higher than those of the Escalating Plan, they eventually become lower. However, the consistency of the payouts throughout the individual’s lifetime is attractive to those who want to plan their finances with certainty.

Under the Standard Plan, all Retirement Account savings will be deducted as CPF LIFE premium. Once the CPF LIFE premium is depleted, individuals will continue to receive monthly payouts from the accumulated interest. In the event of an individual’s passing, any remaining CPF savings and premium balances from CPF LIFE will be transferred to the beneficiaries as well.

CPF LIFE Escalating Plan

The CPF LIFE Escalating Plan offers a premium that starts lower than the Standard Plan, but gradually increases over time. This increase aims to combat annual inflation, ensuring that the spending ability of individuals remains constant despite rising living costs.

With the CPF LIFE Escalating Plan, payouts increase by 2% annually, beginning on the month of the first payout. This strategy ensures that individuals can maintain their standard of living and keep up with inflation. However, instead of matching the payouts specifically to the actual inflation rate each year, the increase is fixed at 2% to ensure that payouts are predictable and stable.

For example, if the payout starts at S$1,000 per month at age 65, it would reach around S$1,500 when the individual reaches 85 years old.

Monthly payouts from CPF LIFE will be taken from the CPF LIFE premium. Once the premium is exhausted, the payouts will be funded from the interest accumulated. Additionally, CPF LIFE premium deductions will be made from Retirement Account savings when individuals join between the ages of 65 to 70.

In summary, the CPF LIFE Escalating Plan offers a lower premium and increasing payouts that combat inflation, making it a suitable choice for those who want to maintain their standard of living throughout retirement.

Calculating Payouts: How Does It Work?

CPF LIFE is a self-sustaining insurance scheme that is designed to be stable, with payouts matched to the premiums that are paid by individuals. Although it does not guarantee payouts, the design of the scheme ensures a high level of stability, increasing the likelihood of receiving payouts.

Payouts are calculated based on four key factors: gender, age, current and future CPF interest rates, and mortality rates. However, the exact method of calculation is not publicly disclosed by CPF.

More Options to Consider

Have you considered deferring your payouts? If you are still working or have other sources of income, you may choose to delay receiving payouts until you reach 70 years old. The longer you defer, the higher your payouts will be. In fact, for each year you defer, your payouts increase by 7%, and after 5 years, your payouts will have gone up by 35%.

If you were previously on a Basic, Balanced, Plus, or Income Plan, switching to the Standard or Escalating plans under CPF LIFE might be a better option for you. By doing so, you can enjoy regular payouts that do not decrease over time, providing you with greater financial stability in your retirement. Contact us to learn more about these options and how they can benefit you.

Which is the right plan?

Choosing the right CPF LIFE plan for your retirement can be a daunting task, as each plan has its own advantages and disadvantages. However, understanding the basics can help you make an informed decision.

If you’re concerned about inflation and the declining purchasing power of your payouts over time, the CPF LIFE Escalating Plan can help mitigate those worries. On the other hand, if you can cope with rising prices, the CPF LIFE Standard Plan’s level payouts should be sufficient.

Regardless of the plan you choose, you’ll be able to enjoy payouts for the rest of your life, with any remaining CPF LIFE premium balance given to your beneficiaries upon death.

However, CPF LIFE is just one of the many retirement and endowment plans available. It’s important to ensure that you have other sources of income to tide you through retirement. That’s where our professional partnered Financial Advisory (FA) Advisor comes in.

Read more here: Best Retirement Plans Singapore 2023 – The Ultimate Guide

Don’t hesitate to drop us a message below and let our FA Advisor get in touch with you to provide non-biased advice on CPF LIFE and other retirement options. Plan your retirement with confidence today!