Last Updated on by Tree of Wealth

Subscribe to our Telegram & Email Newsletter for immediate updates!

You might already be familiar with the Child Development Account (CDA) scheme for Singapore parents. It’s a special savings account that’s opened within 3 to 5 working days of the birth registration or after completing the online form, whichever is later. In Singapore, there are three CDA accounts in the market: POSB Smiley CDA, OCBC CDA and UOB CDA. In this article, we look at where you can use the CDA funds and what happens to the money when the child grows up.

How long can we use CDA?

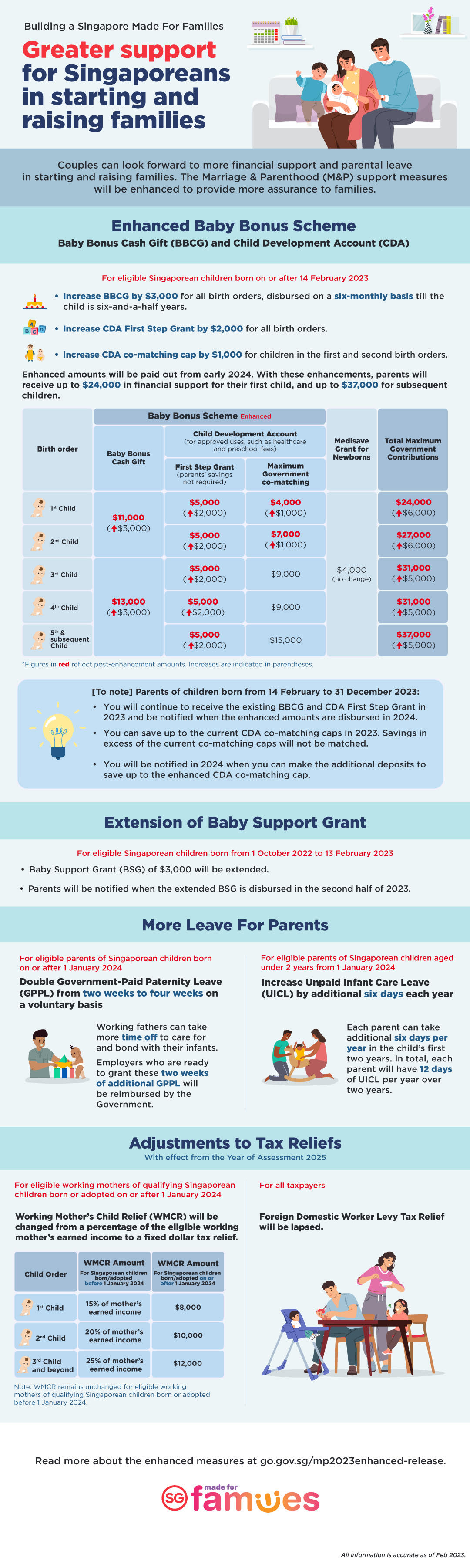

You have 12 years to save in this special savings account. The Government will match the amount you save in the CDA after the first 2 weeks, up to a maximum amount depending on the birth order. Additionally, the new enhanced Baby Bonus scheme has stipulated that babies born from 14 Feb 2023 will receive up to $5,000 of First Step Grant and CDA co-matching contributions, up to the eligible child’s prevailing cap. Check about government matching and First Step Grant on the Made for Families website.

How can we use the CDA account?

The CDA comes in handy to ease the financial burden of new parents since you can use the money to pay for educational and healthcare expenses of all your children at Baby Bonus Approved Institutions (AIs) such as:

- Child care centres

- Kindergartens and special education schools registered with the MOE or CPE

- Early intervention programmes registered with the NCSS or Centre for Enabled Living

- Healthcare institutions

- Assistive technology device providers (eg. for hearing aids)

- Optical shops

- Pharmacies

Do check if the institute accepts payment from the CDA account before you enrol your child or purchase any related items.

What happens to the CDA after the child turns 12 years old?

While the CDA is known as a savings account, note, though, that you cannot withdraw funds directly from the account when you want to use it for your child. So what happens if you have not exhausted the funds at Baby Bonus Approved Institutions once your child turns 12?

Any funds left in the account will be automatically transferred to the Post-Secondary Education Account (PSEA). The Post-Secondary Education Account (PSEA) is part of the Post-Secondary Education Scheme to help fund the post-secondary education of Singaporeans. The funds in PSEA pay for the account holder, or parents can also apply to pay for their siblings’ approved programmes at approved institutions. The account holder can also use the remaining funds to repay government education loans and financial schemes. You can check which institutes accept PSEA funds on the Ministry of Education’s website.

Can I close the CDA account?

The last question is whether you can withdraw the amount within and close the CDA account. The answer is no, you cannot close the CDA and withdraw the funds within. As mentioned above, the funds in the CDA are for you to use at Baby Bonus-approved institutes for your child. So, before registering your child for childcare, check if the institute accepts payment from the CDA account.

Wait…it’s a savings account? Does it have an interest rate?

The last question new parents may have is whether the amount saved in the bank will gain interest. Yes, the three local banks (POSB, OCBC and UOB) offer CDA accounts that typically offer 2% interest. The next question parents may have whether they should choose POSB, OCBC or UOB.

Well, if you check the various banks’ promotions, you might notice subtle differences in the CDA savings scheme in each bank. For instance, the POSB Smiley CDA provides a POSB Smiley Nets Card, which lets parents enjoy exclusive deals at kid-friendly places such as Mindchamps Preschool and even massage deals for moms who just gave birth. Plus, POSB also offers a reserved savings account bundled with CDA. POSB also currently offers 2% interest p.a for $50,000 and below. UOB has a similar scheme, except there is no cap on the amount for 2% interest p.a. In contrast, OCBC has a step-up interest, where you get 1.2% a year on the first S$10,000 saved in your child’s CDA and 2.4% a year when you save above S$10,000.They also have a benefits card which offers up to 50% discount on selected merchants.

Ultimately, whichever account you choose, you need to be aware that you cannot withdraw the CDA funds or close the account. The money remains in the CDA until the child turns 12. You can refer to our above section on “What happens to the CDA after the child turns 12 years old” to find out what you can do with the CDA. You also have to check if the institute accepts CDA funds before enrolling your child into any program. Read our section above on “How to use CDA account” to find out more.

Subscribe to our Telegram & Email Newsletter for immediate updates!

{kind=link}