Last Updated on by Tree of Wealth

Tokio Marine’s #goUltra a whole life Investment-linked Policy that comes with Initial Bonus to further add value to the investment that you are taking up. #goUltra is flexible and versatile to adjust to meet your needs should it change throughout the whole life. Withdraw your investment returns should you need it anytime, and contribute more should you want to take advantage of the market situation.

The plan lasts whole life while the premium does not. There is a Minimum Contribution Period (MIP) of which premiums are required to be in coupled with premium waiver all the way to early Critical Illness features, as well as death protection.

Features At a Glance for Tokio Marine #goUltra

High Flexibility

- Unlimited premium holidays should you need to pause premiums

- Able to top up premiums should you want to take advantage of the market

- Unlimited Fund switch with no charges

- Flexible cash withdrawals available (charges may apply)

- 5 major currency choices should you prefer to invest in various currencies: SGD / AUD / GBP / USD / EUR

Wealth Bonuses

- Start your investment with an Initial Bonus of up to 192%, as well as high Loyalty and Additional Bonuses of up to 1.8% annually.

- Choose from a huge range of funds, including equities and dividend paying funds, which allows you to create yet another stream of income.

- 100% of your premiums go into investing

Initial Bonus Rate

| Initial Bonus rate Per Annum (% of annualised premium) | |||

| Monthly Premium (S$) | Minimum Contribution Period | ||

| 5 years | 10 years | 20 years | |

| 999 & below | 2% | 13% | 25% |

| 1,000 – 1,999 | 3% | 19% | 36% |

| 2,000 – 2,999 | 4% | 22% | 41% |

| 3,000 – 3,999 | 6% | 27% | 43% |

| 4,000 and above | 7% | 30% | 48% |

Fees and Charges

| Initial Charge | 5.4% p.a. of Initial Units Account value |

| Policy Charge | 1.35% p.a. of policy value |

| Premium Charge for Top-Up Premium | 5% of each top-up premium |

| Monthly Protection Charge | Applicable for Advanced Death Benefit option only.

Calculated based on sum at risk. |

| Premium Shortfall Charge | Applicable for any reduction in committed annualized regular premium and/or premium holiday prior to the end of the Minimum Contribution Period. |

| Partial Withdrawal Charge | Applicable for any withdrawals prior to the end of the Minimum Contribution Period. |

| Change in Policy Currency Charge | Nil |

| Credit Card Charge | Waived for first premium payment. For subsequent premium payments via credit card, a 1.60% charge will be imposed on each premium paid. |

| Fund Management Charge | Depends on the chosen investment fund |

| Fund Switching Charge | Nil |

| Surrender Charge | Applicable at any time prior to the end of the Minimum Contribution Period. |

Source: Tokio Marine

Protection While Investing

- In the event of death, have the assurance that your investments are protected even when the market is not performing, during the minimum premium contribution period.

- Choose between Advanced Death Benefit or Basic Death Benefit

- Choice of complementing your coverage by adding supplementary benefits riders

Supplementary Protection Riders to Enhance Your Protection

Protect against Early, Intermediates to Advance Stage Critical Illness (CI), including Cancer.

Early Critical Illness Premium Waiver Rider

In the event of the covered Early or Intermediate stage of CI (Critical Illness), future premiums will be waived for 5 years, up to a maximum of 2 times.

Cancer Waiver Rider

In the event of Advanced Stage Cancer being diagnosed, future premiums will be waived.

Waiver of Premium Rider

In the event of Advanced Stage Critical Illness being diagnosed, future premiums will be waived.

Payer Benefit Rider, Spouse Rider

In the event of Death or TPD (Total and Permanent Disability) for self or spouse, future premiums will be waived.

Enhanced Payer Benefit, Enhanced Spouse Rider

In the event of Death, TPD (Total and Permanent Disability) or diagnosis of the covered Critical Illness of the Advance Stage, future premiums will be waived. This is applicable to both the policy holder (self) and spouse.

Legacy Planning

- Choose to transfer the policy to family members for legacy planning

- Choose to change the life assured to family members upon reaching life milestones

Guaranteed Issuance

Plan is guaranteed to be issued with no medical check-up/ underwriting

Minimum Contribution Period

As the Investment Linked policy is a whole life plan, there is a choice of 3 different contribution period, this will affect the bonus as illustrated above.

Choose from 5, 10 and 20 years of minimum contribution period. Thereafter, you can actually continue to put in should you want to grow more for your wealth.

Access to Best-In-Class ILP Funds

Choose from a good range of pure investment funds for retail investors to accredited investor funds.

For a comprehensive list of funds, have a look here: Tokio Marine Fund List

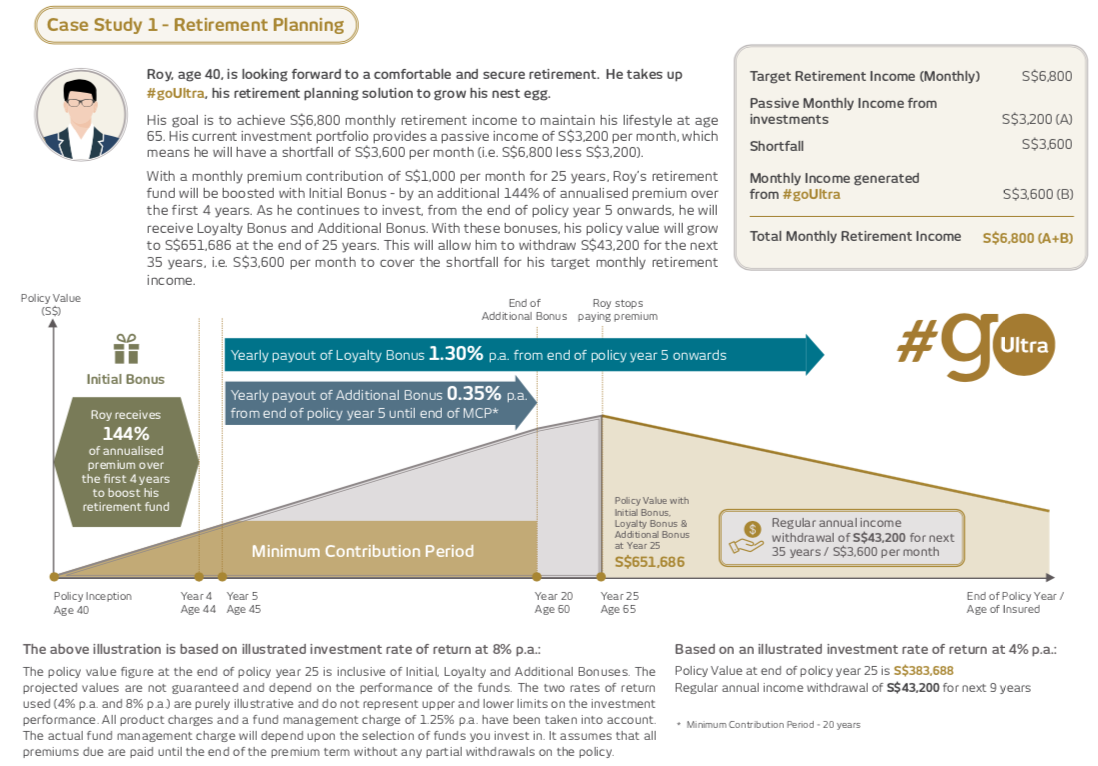

How TM #goUltra Works

Why We Like The Tokio Marine #goUltra

Very Budget Friendly For the Type of Funds Available

- Low start up of $200 monthly for 20 years premium term

100% Unit Allocation

- Starting from the moment you input the regular premium, 100% of it will be allocation to purchase of units. Unlike traditional ILPs where the first 5 years are usually less than 100% for units allocation (first 3 years less than 30% to 50% allocation) as they go into admin expenses and agent’s commissions.

- Your investment is complemented and enhanced with the start-up bonus as well as ongoing loyalty bonuses

Access to a Range of Good Funds

- Not sub funds managed by insurer but pure investment funds that are invested by retail investors as well as accredited investors.

Highest Bonus Up to 192%

Flexible and Low Commitment after Minimum Contribution Period 4 years

Wide Range of Entry Age

- Entry Age (age next birthday) Life Assured: 1 month old – up to age 70

- Policy Owner (Assured): Age 19 – 70

Multiple Lives Application

- Up to 2 Policy Owners (Assured) and 4 Lives Assured

Tokio Marine #goUltra Is Suitable If You Want:

- Access to a range of strong retail funds as well as accredited investors funds

- High flexibility to your investments

- Wide range of choices for currency to invest

- High Start-up bonus to complement your investment journey

- Good investment tool to leave behind your legacy

It would however be less suitable if you would like:

- Returns that are guaranteed

- High protection coverage for death, TPD and Critical Illness

- Single Premium Investment

Conclusion for The Tokio Marine #goUltra Review

We hope the analysis helps you in understanding the pros and cons of the Tokio Marine #goUltra ILP.

As with all plans, Endowment, Whole life protection and Term plans, all Investment-Linked Policies have their own advantages and disadvantages. We recommend that all individuals choose their savings plans keeping in mind their objectives and liquidity needs to ensure they get the best possible value.

Are you considering investing in an ILP? Let us do the homework and help you compare across the different retirement plans in the market to save you time. Drop us an inquiry below and our professional experienced licensed FA advisor will get in touch with you shortly upon your request.

Our financial consultants will use your input and preferences to draft proposals for you. Your information provided will only be used for communication.

All the comparisons will be done according to your needs to get you the best retirement plan.

Fill in the form below and our friendly licensed FA advisor will get in touch with you. Based on your needs, a custom made solution will be adjusted only addressing your concerns.

No obligations, no hidden fees. All advice are of no charges.