Last Updated on by Tree of Wealth

The Aviva MyLongTermCare and MyLongTermCare Plus underwent a name change on 16th August 2022. They are now respectively known as Singlife CareShield Standard and Singlife CareShield Plus.

Designed to enhance the protection offered by CareShield Life, Singlife’s CareShield Standard and CareShield Plus cater specifically to those facing severe disabilities. If you find yourself grappling with severe disability, these plans ensure a consistent monthly payout to ease your journey.

If the term “CareShield Life” seems unfamiliar, worry not. We’ve got a brief rundown for you in the following section. However, if you’re already informed about it, you might want to jump directly to the section detailing the features of Singlife CareShield Standard and Plus to discern if they align with your needs.

Understanding CareShield Life: CareShield Life is a visionary long-term care initiative by the government, conceptualized with the challenges of an aging population in mind. Its central aim is to mitigate the financial challenges associated with severe disabilities by assuring a dependable monthly payout for as long as the disability persists.

Here are some essentials about CareShield Life:

- It’s mandatory. Upon turning 30, enrollment is automatic, irrespective of pre-existing conditions or disabilities.

- Premiums are entirely covered by MediSave, guaranteeing lifetime coverage.

- The scheme began with a $600 monthly payout in 2020.

- Payout amounts undergo an annual increase until the age of 67 or upon a successful claim, whichever is earlier.

While the existence of such a security blanket is commendable, a deeper reflection reveals that a standalone $600 might fall short in catering to both medical necessities and basic living expenses.

In the journey to self-reliance, Singlife’s CareShield plans can serve as vital tools. They can enhance your coverage, ensuring you’re better equipped to manage potential disabilities with improved monthly financial support.

Offered in two distinct packages, the basic Singlife CareShield Standard and the more comprehensive Singlife CareShield Plus, let’s delve into what these plans entail.

Understanding the Core Aspects of Singlife’s CareShield Supplement

- Monthly Benefit: This pertains to the regular financial assistance you receive.

- Payout Criteria: The specifications that determine your eligibility for benefits.

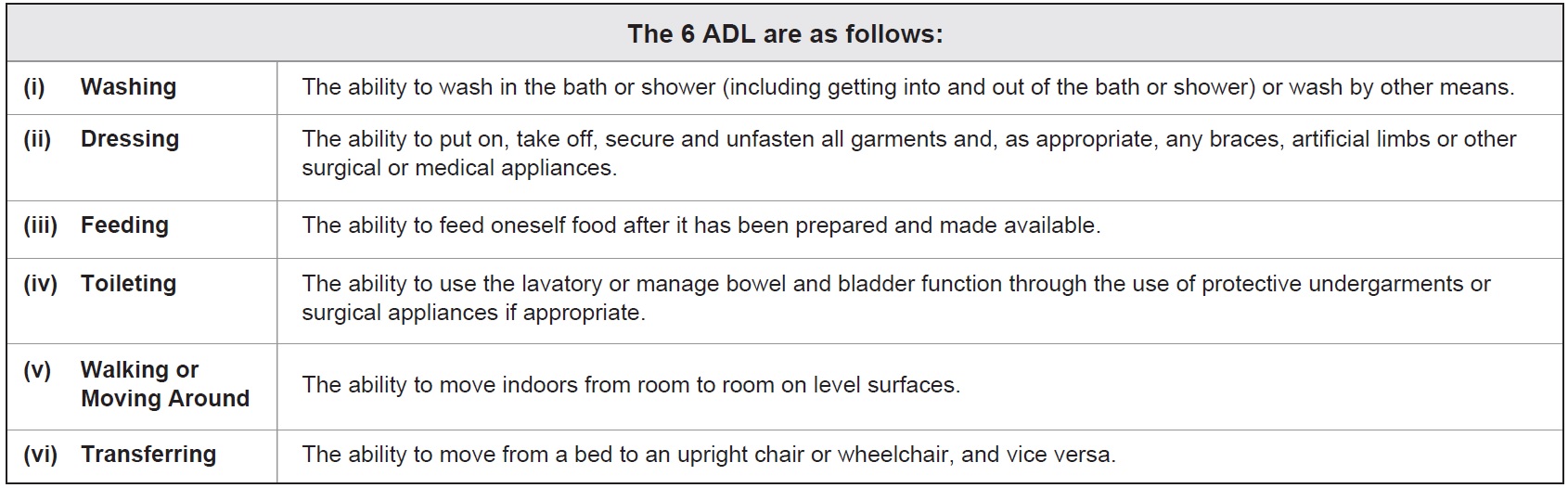

To successfully navigate and understand the complete array of product features, there’s an essential concept to grasp: Activities of Daily Living (ADL). This concept is foundational to determining the severity of a disability. In essence, your ability or inability to perform certain ADLs will dictate if you’re deemed “severely disabled” and, consequently, if you’re eligible for specific benefits.

The 6 ADL Are As Follows:

| (i) Washing – The ability to wash in the bath or shower (including getting into and out of the bath or shower) or wash by other means. |

| (ii) Dressing – The ability to put on, take off, secure and unfasten all garments and, as appropriate, any braces, artificial limbs or other surgical or medical appliances. |

| (iii) Feeding The ability to feed oneself food after it has been prepared and made available. |

| (iv) Toileting The ability to use the lavatory or manage bowel and bladder function through the use of protective undergarments or surgical appliances if appropriate. |

| (v) Walking or Moving Around The ability to move indoors from room to room on level surfaces. |

| (vi) Transferring The ability to move from a bed to an upright chair or wheelchair, and vice versa. |

What is ADLs and Its Impact on Your Coverage

Understanding Activities of Daily Living (ADLs) is pivotal when looking into the Singlife CareShield plans. To be classified as “severely disabled” under the Singlife CareShield Standard plan, an individual needs to be incapable of performing a minimum of 3 ADLs, mirroring the criteria of CareShield Life.

On the other hand, the Singlife CareShield Plus is a bit more lenient, providing payouts when you are unable to perform just 1 ADLs.

As long as you meet the criteria of being “severely disabled” under your chosen plan, you are entitled to monthly payouts indefinitely. Should your condition see improvement and you no longer fit the “severely disabled” label, the payouts will cease.

Add-on Payout Benefit – ADL Coverage Enhancements

For Singlife CareShield Standard, the benefit is triggered when the insured can’t manage 2 ADLs, while for Singlife CareShield Plus, it activates with an inability to perform 1 ADL:

Plan |

Criteria |

Payout |

|

Singlife CareShield Standard |

2 ADL | 100% of Severe Disability Benefit payable monthly

(up to 12 months) |

| Singlife CareShield Plus | 1 ADL |

100% of Severe Disability Benefit payable monthly (up to 12 months) |

Related

What Is Dementia & Why It Will Affect Long Term Disability Care

Understanding the Deferment Period

It’s crucial to note a 90-day waiting period, also known as the deferment period, that starts from the day you’re officially diagnosed as “severely disabled” by a certified assessor. Only after this period will the monthly payouts begin.

However, if a relapse into severe disability occurs within 180 days of recovery due to the same cause, this deferment period is bypassed.

Payout Amount

The beauty of these plans lies in their flexibility. You can choose a monthly payout between $200 and $5,000, which is provided in addition to the benefits of CareShield Life.

For instance, if you select a monthly benefit of $3,000 under the Singlife CareShield Standard, and later find yourself unable to perform 3 ADLs, your monthly payout will total $3,600 ($600 from CareShield Life and $3,000 from your Singlife CareShield plan).

Conversely, under the Singlife CareShield Plus with the same monthly benefit, being unable to execute 2 ADLs will fetch you a $3,000 monthly payout. If you can’t perform 3 ADLs, the amount increases to $3,600.

Choosing Between the Basic and Plus Plans

If you’re on the fence about which plan to opt for, consider at which stage of disability you’d prefer to start receiving benefits. While the Plus plan offers earlier payouts, it comes with a heftier price tag. Weigh the cost against your financial comfort and the value you see in early benefit access.

Deciding Your Monthly Payout

When settling on a monthly benefit, consider potential care requirements. Will you rely on family support, or might you need professional assistance, like a caregiver or domestic helper? Additionally, evaluate your monthly basic expenses, like meals and other essential costs, to ensure a comfortable and secure lifestyle.

Premiums At a Glance

Male, Level Payout, Premium Term until age 99

|

ANB |

31 | 36 | 40 |

|

Payout Amount |

$1000 | ||

|

Premium |

$489.24 | $465.70 |

$567.04 |

| Payout Amount |

$2000 |

||

|

Premium |

$765.51 | $914.12 | $1116.81 |

| Payout Amount |

$3000 |

||

|

Premium |

$1122.33 | $1345.24 | $1649.29 |

|

Payout Amount |

$4000 |

||

| Premium | $1496.45 | $1793.66 |

$2199.06 |

| Payout Amount |

$5000 |

||

| Premium | $1870.56 | $2242.08 |

$2748.82 |

Female, Level Payout, Premium Term until age 99

|

ANB |

31 | 36 |

40 |

|

Payout Amount |

$1000 | ||

|

Premium |

$487.82 | $585.88 | $717.55 |

|

Payout Amount |

$2000 |

||

| Premium | $958.35 | $1154.47 |

$1417.82 |

| Payout Amount |

$3000 |

||

|

Premium |

$1411.60 | $1705.80 | $2100.82 |

| Payout Amount |

$4000 |

||

|

Premium |

$1882.14 | $2274.39 |

$2801.09 |

|

Payout Amount |

$5000 |

||

| Premium | $2352.67 | $2842.99 |

$3501.36 |

How Singlife CareShield Plus Works

How Singlife CareShield Standard Works

Keeping Pace with Inflation: The Escalating Payout Option

It’s crucial to ensure that your financial protection remains robust even as the cost of living rises. Singlife CareShield’s escalating payout option allows you to do just that. With this feature, you can choose to have your payouts increase by either 2% or 3% annually, ensuring that your benefits keep up with inflation.

While this option will cause your premiums to incrementally rise each year, this will continue only until the end of your policy term or until you make a claim. Once a claim is lodged, there’s good news: your premiums will then freeze at the rate of your initial claim month and won’t increase further in subsequent years.

To provide a clearer picture, let’s consider an example: If you choose a monthly benefit of $1,000, the subsequent section will break down the payouts you can expect should you face severe disability within the initial three years of your policy.

| Year of Disability | Level Payout ($) | Escalating at 2% ($) | Escalating at 3% ($) |

|---|---|---|---|

| 1 | 1,000 | 1,000 | 1,000 |

| 2 | 1,000 | 1,020 | 1,030 |

| 3 | 1,000 | 1,040 | 1,060 |

The escalation of both the monthly benefit and premium will cease either when the first successful claim (this includes the Waiver of Premium benefit) is lodged, or when the premium term concludes, whichever comes first.

From that point onward, your monthly benefit will remain consistent, and you’ll keep receiving this fixed amount for the duration of your policy.

What this means is that from the provided information, if you select a payout that escalates by 2% annually and encounter severe disability in the second year, your monthly payout will stabilize at $1,020, which you’ll receive for the entirety of your policy term.

Understanding Your Premium Options

When deciding on your premium payment duration, you have a couple of options:

- Continue payments until the policy anniversary post your 97th birthday, or

- Opt for a limited period which concludes either:

- On the policy anniversary following your 67th birthday, or

- 20 years post policy acquisition, provided your age on your next birthday is 49 during the policy purchase.

To ease the out-of-pocket expenses and perhaps as an incentive to upgrade your CareShield Life coverage, you can tap into your MediSave account. Specifically, up to $600 annually can be utilized to cover your premiums.

If you’re inclined to select the escalating payout feature, remember that your premiums will also climb, either by 2% or 3% annually, mirroring the rate you’ve chosen for the payout increase.

Lifetime 20% Premium Discount

For those considering the Singlife CareShield Standard or Plus plan as of August 2022, there’s good news: a lifetime premium discount of 20% awaits you. Singlife with Aviva is offering this continuous discount until they announce any changes.

However, to be eligible for this discount, your plan has to satisfy the Minimum Annual Premium (MAP) requirement, which stands at $500 per policy (exclusive of any substandard lives premium loading but inclusive of GST). If, for any reason, your annual premium dips below the MAP during your policy term, the discount application will cease.

Waiving the Premium

To alleviate some of your financial concerns, the policy has a feature where, should you find yourself unable to undertake even one ADL (Activity of Daily Living), your premium payments will be paused. This waiver kicks in only after the deferment period has elapsed.

However, should your health recuperate and you regain the ability to handle all the ADLs, your obligation to pay premiums will be reinstated.

Diving Deeper into Singlife’s CareShield Supplement Features

1. Care Benefits Facing severe disability can heavily strain one’s finances. Often, individuals may take years to recover, if recovery is even a possibility. The Singlife CareShield Plus plan incorporates several added benefits to aid you financially in such circumstances.

2. Lump-Sum Benefit Upon your first diagnosis of severe disability, both plans grant a one-time payment that’s equivalent to thrice your monthly benefit. Remember, the deferment period is still applicable here.

3. Rehabilitation Benefit Exclusive to the Singlife CareShield Standard plan, this perk becomes accessible if there’s an improvement in your condition but you’re still unable to handle 2 ADLs independently. This implies that initially, you must have been diagnosed with a severe disability per the Singlife CareShield Standard criteria (an inability to manage 3 ADLs) to qualify for this benefit. If eligible, you’ll get a monthly amount equivalent to half of your previous monthly benefit, as long as 2 ADLs remain challenging for you. Note that this benefit isn’t part of the Singlife CareShield Plus offering, as this plan already regards you as severely disabled and grants full benefits if 2 ADLs are out of reach.

4. Dependent Care Benefit Should you be able to claim monthly or rehabilitation benefits and have a child who’s 21 (or turning 22 the next year), an extra 20% of your monthly benefit will be yours for up to three years. With severe disabilities potentially impacting your earning capacity, this added support can be invaluable, especially if you’re responsible for a dependent child.

5. Caregiver Relief Benefit For those worried about the expenses tied to caregiving, this plan has you covered. You’ll get an additional 60% atop your monthly benefit for a year from the moment you’re eligible for monthly or rehabilitation benefits. This helps defray some of the caregiver-related costs.

6. Death Benefit In the unfortunate event of your passing while you’re still availing monthly or rehabilitation benefits, a lump sum equivalent to three times your latest monthly/rehabilitation benefit will be bestowed upon your next of kin. This provision offers some financial relief during a challenging time.

Opt for the Guaranteed Issuance Option (GIO) for Adaptive Coverage

Life is dynamic. As we march through the ages, we encounter various significant moments that might escalate our responsibilities and, consequently, our need for insurance protection. The ability to upscale protection without repeatedly going through health evaluations can be invaluable.

Recognizing these ever-changing life dynamics, Singlife in partnership with Aviva offers the Guaranteed Issuance Option (GIO). With GIO, you’re empowered to elevate your monthly benefits in line with these critical life moments, without the need to continually validate your health status:

- Property Ownership: Whether you’re a first-time homeowner or expanding your property portfolio.

- Marital Changes: This applies to tying the knot, undergoing a divorce, or becoming a widow or widower.

- Parenthood: Welcoming a child into the world, either through birth or the legal adoption of a child aged 18 or below.

- Salary Increase: Experiencing a salary hike of 50% or more compared to your initial salary at the time of policy application.

- Skill Enhancement: Successfully completing a skill development course that spans at least 6 months.

- New Insurance Acquisition: Procuring a fresh Single Life insurance policy or rider from Singlife with Aviva, which has been fully underwritten at standard terms.

- Spousal Events: Instances where your spouse either becomes severely disabled, being unable to perform at least 3 ADLs, or unfortunately passes away.

However, there’s a caveat. The GIO is only accessible if your policy was initiated under standard terms. If you decide to make use of this option to bolster your monthly benefit, it’s natural that the associated premiums will also see an uptick.

The ceiling on how much you can boost your monthly disbursement is determined by the smaller amount between:

- 50% of the monthly payout at the beginning of the policy, or

- The monthly benefit amount when you decide to utilize the option.

Sidenote On Dementia

As Singaporeans enjoy extended lifespans, the potential for disability during our twilight years becomes more pronounced. Events like strokes can strike suddenly, while chronic ailments such as diabetes, heart disease, and cancer often grow more debilitating over time. Given these realities, it’s paramount for today’s professionals, spanning from young adults to those in their mid-50s, to thoughtfully strategize for their long-term care, ensuring they don’t inadvertently place undue stress on their loved ones and caregivers.

Many think that Long Term Disability arising mostly from stroke and critical illnesses.

However, there is a condition that is often overlooked when we talk about Long Term Disability, and that is Dementia.

What Is Dementia?

Dementia is a progressive brain disorder that affects memory, thinking skills, and the ability to perform everyday activities, also known as Activities of Daily Living (ADLs). As dementia progresses, it impacts various aspects of an individual’s functionality.

Here’s how dementia can lead to an inability to perform ADLs:

- Mobility and Transferring: Dementia may lead to challenges with motor coordination and balance. Over time, individuals might struggle to move from one position to another, such as from a bed to a standing position or from a chair to a standing position.

- Dressing: Cognitive decline can make it challenging to remember the sequence of dressing or how to manage fastenings, like buttons or zippers.

- Feeding: Dementia can cause difficulty in recognizing when one is hungry, forgetting how to chew or swallow, or even how to use utensils. This can make feeding oneself challenging.

- Personal Hygiene: Tasks like brushing teeth, bathing, and grooming can become overwhelming. There might be a fear of water, forgetfulness about the need to maintain hygiene, or difficulty in using toiletry items.

- Toileting: An individual may forget where the bathroom is or how to use the toilet. There might also be incontinence issues due to a lack of recognition of bodily signals.

- Continence Management: As dementia advances, an individual may lose control over bladder and bowel functions and may not remember or recognize the need to go to the bathroom.

Besides these basic ADLs, dementia can also impact Instrumental Activities of Daily Living (IADLs), which are more complex skills needed for independent living:

- Managing Medications: Forgetting to take medications, taking incorrect doses, or not recognizing medicines are common challenges.

- Cooking and Meal Preparation: Dementia patients may forget how to cook, leave stoves on, or not eat balanced meals.

- Managing Finances: Forgetfulness can lead to unpaid bills, overspending, or being susceptible to financial scams.

- Using the Telephone or Other Communication Devices: An individual might forget how to use a phone or not recognize familiar numbers.

- Housekeeping and Home Maintenance: There may be neglect in cleaning, laundry, or keeping up with repairs.

- Shopping: Forgetting what to buy, purchasing unnecessary items repetitively, or getting lost in stores can occur.

- Transportation: Individuals might forget how to drive, get lost easily, or not remember the way back home.

As dementia progresses, the decline in cognitive and physical abilities becomes more pronounced, leading to increased dependency. Early recognition and intervention, as well as a supportive environment, can help manage some of these challenges. However, as the disease progresses, professional care and assistance often become essential for the well-being of the individual.

While dementia presents a series of challenges that can affect everyday tasks, it’s crucial to remember that early intervention and a supportive environment can make a significant difference. The journey with dementia can be navigated more smoothly with the right resources, understanding, and planning.

There’s a world of assistance out there, and with the correct guidance, individuals and families can find hope and strength even amidst the challenges.

Related

Review: Best Careshield Life Supplement Option [In-Depth Analysis]

Singlife CareShield Plans: A Comprehensive Review

Among the three insurers offering CareShield Life supplement plans, it appears that Singlife’s offering delivers significant value, providing a multitude of benefits and features that aren’t available with other insurers.

The Singlife CareShield Standard and Singlife CareShield Plus are the only plans that offer both rehabilitation and caregiver relief benefits.

Even when a disability shows improvement, going from an inability to perform 3 ADLs down to 2 ADLs, the individual will likely still need assistance. This is where the rehabilitation benefit demonstrates its importance.

It is recognized that needs and circumstances change over time, leading to evolving liabilities and coverage requirements. The Guaranteed Issuance Option (GIO) and escalating payout options ensure that the Singlife CareShield supplement plan remains adaptable and offers adequate protection.

Long Term Disability Solutions

For those uncertain about the suitability of Singlife’s plans, there are comprehensive guides available on selecting the most appropriate CareShield Life supplements based on various circumstances.

Ultimately, as is the case with all insurance plans, the best plan will differ for each individual. Therefore, the optimal choice should be based on a thorough assessment of individual needs and preferences. It is recommended to seek advice from financial advisors to ensure an informed decision.

Sudden event like Stroke, or chronic conditions like Diabetes and Dementia not only affects one’s health but has implications on financial stability and planning too. It’s never too early or too late to consider the financial dimensions of long-term care.

Our financial advisors specialize in comprehensive financial planning that takes into account potential health concerns like dementia. Equip yourself with the knowledge and strategies needed to face the future confidently.

Get in touch today, and let’s pave a financially secure path together: