Last Updated on by Tree of Wealth

Subscribe to our Telegram & Email Newsletter for immediate updates!

When you are purchasing your dream home, one would think of using your Ordinary Account (OA) from your CPF savings to support your housing payments. After all, OA savings can be used to buy both HDB and private properties. This includes using it for the down payment and housing loan taken for the property purchase, stamp and legal fees, loan taken for the construction of your house and the purchase of vacant land (for private properties only), as well as the Home Protection Scheme premiums (for HDB flats only).

Discharging your CPF charge when you bought your private property

Using your OA for your private property would likely bring about a CPF charge. To discharge it, you need to refund the amount used for the property and the accrued interest to your CPF account, and this can be done in two ways.

The first is voluntarily refunding the amount used to your CPF account. After the refund is made, you will need to engage a lawyer to lift the CPF charge on your property. If you are above 55 and wish to withdraw your Retirement Account savings above the Basic Retirement Sum by pledging the property in the future, a fresh CPF charge will be lodged to secure the refund of the withdrawal amount when the property is sold/transferred in future.

The second is refunding the amount used to your CPF account when you sell your property. Your lawyers handling the sale will complete the discharge as part of the sale transaction.

There are steps taken before you sell or transfer your property. This depends on the type of property. In the case of HDB flat, you will need to check with HDB on your eligibility to sell or transfer your flat. Once HDB has consented, HDB or your lawyer will check with the Board on the amount (if any) to be refunded to your CPF account. For private property, you will need to instruct your lawyer to obtain consent from the Board before you sell or transfer your property.

How much do I need to refund?

Even with OA’s attractive utility, we must still remember that your CPF savings are for your future retirement needs. Using your CPF savings for your property eventually reduces your retirement savings. Thus, when you sell your property, you will need to refund the principal CPF withdrawn towards the property (including the CPF Housing Grant) plus the interest accrued on this amount. This is to restore your retirement savings.

The housing grant will be refunded to your OA. If you received more than $30,000 in housing grants, part of it may be credited to your Special Account/ Retirement Account and MediSave Account.

Scenarios where you do not need to refund

There are scenarios when a refund is not needed:

- When you did not use your CPF savings for your property

- Paying for your late parent(s) – There is no need to refund the CPF savings used by your late parent(s) and the accrued interest on their CPF accounts

Dealing with HDB accrued interest

How to check CPF accrued interest?

This interest accrued accounts for the amount that you would have earned if your CPF savings had not been withdrawn for housing. This is calculated using the CPF principal amount withdrawn for housing every month (at the current CPF Ordinary Account interest rate) and compounded yearly. To check CPF accrued interest, you can view the hdb accrued interest calculator to find out how much is to be refunded to your CPF account upon the sale of your property.

Accrued interest CPF after 55 years old

Even if you are 55 and above, if you have pledged the property to make up your retirement sum, you will also need to refund the pledged amount. A small exception happens when the selling price after paying the outstanding housing loan is not enough to fully refund the CPF principal amount withdrawn together with the accrued interest. If this happens, you do not need to top up the loss in cash, provided the property is sold at market value.

Once the amount is refunded from the sale of your property, it will be used to meet your Full Retirement Savings in your Retirement Account. If there is a balance, it will be paid to you in cash. You may also choose to retain the balance in your CPF account by writing to the CPF board two weeks before the completion of the sale of your property.

In the case of Reduced Life Expectancy

In the case of reduced life expectancy due to a medical condition, being permanently unfit for work, or lack of mental capacity permanently, you may have withdrawn some of your CPF savings.

If the CPF savings that you had previously withdrawn for your property did not form part of the amount approved for withdrawal, you may still have to refund the CPF principal amount withdrawn from the property and the accrued interest. You can apply to withdraw the refunded amount under Reduced Life Expectancy if you are eligible to.

This amount refunded from the sale of your property will be used to top up the applicable reduced Retirement Sum shortfall (if any) in your Retirement Account. Any balance will remain in your CPF account. You may apply to withdraw this excess amount and HDB will access your request.

In both circumstances of transferring or selling your share of the property, you will need to refund the CPF principal amount withdrawn plus the accrued interest (“P+I”).

If you have attained it at the age of 55, and have pledged the property to make up your retirement sum, you will need to refund the pledged amount on top of the P+I. The amount refunded will be used to top up your Retirement Account, up to your Full Retirement Sum. After this, any balance housing refunds will be paid to you in cash.

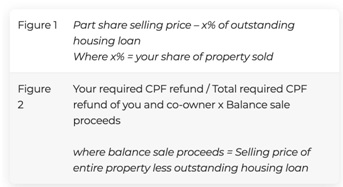

The only exception when selling your share is if the part share selling price less your share of the outstanding housing loan is insufficient to fully refund your required CPF refund, and provided that the part share transaction is conducted at market value, your will need to refund the higher of the below two figures, capped at your P+I, calculated by the formulae below:

Taking over the property from your ex-spouse

Your ex-spouse will have to refund the CPF principal amount he/she has withdrawn for the property including accrued interest when he/she is no longer an owner of the property.

However, the Court can grant the flexibility to make an order for the property to be transferred from a member to his/her ex-spouse without requiring the full CPF refund to be made into the member’s CPF account in respect of the money withdrawn by him/her at the point of transfer.

Should the ex-spouse sell the property in the future, he/she is required to refund into his/her CPF account the money withdrawn from the member’s CPF account (which was not refunded upon transfer) as well as the principal amount withdrawn from his/her CPF account for the purchase of the property with accrued interest.

Court order directing a sale/transfer/disposal of my property

If you have a Court Order, the amount to be refunded depends on your age at the time of sale, transfer, or disposal of your property.

If you are below 55 years old, you will need to refund the CPF principal amount withdrawn plus accrued interest upon sale, transfer, or disposal. Similarly above, if the selling price after paying the outstanding housing loan is not enough to fully refund, you do not need to top up the loss. However, any option monies received from your buyer in cash upon the sale of your property are considered part of the selling price and need to be refunded to your co-owners and your CPF accounts before the transaction can be completed.

If you are above 55 years old, it is best to check with the CPF Board on the amount to be refunded upon sale, transfer, or disposal.

What happens after I sell my property?

The sale proceeds distribution depends on your property type and the loan taken.

Generally, the selling price will be used to pay for the following in this order:

- Outstanding housing loan

- Required CPF refund

- Other sale expenses, e.g., legal fees

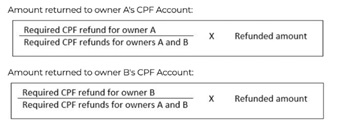

As mentioned above, if the selling price after paying the above is not enough to make the required CPF refund, there is no need to top up the loss. This refunded amount will be returned to your co-owners and your CPF accounts before the transaction can be completed in the following proportions:

How long does it take to process the refunds?

CPF Board will process the refunds within five working days for the sale of the property. This includes the time needed to clear the cheque/ cashier’s order.

Can I use the refunded CPF savings to buy the next property or redeem another housing loan with my CPF savings?

Once you have received your refund, you are generally able to use it for your next property or redeem another housing loan depending on your age at the time of sale of your property.

If you are 55 years old and above, the refunds from the sale of your earlier property will be used to top up your Retirement Account, up to your Full Retirement Sum. After this, any balance housing refunds will be paid to you in cash within one week after the CPF refunds are paid into your CPF account. Alternatively, you can request for the balance housing refunds to remain in your OA to pay for the next property or redeem another housing loan.

While your OA savings can help you with your housing payments, remember that your CPF savings are for your future retirement needs!

A tip is to find a balance between using your cash and OA savings for your housing payments so that you can keep some monies in your OA to earn attractive interest rates. Your OA savings can also act as a safety net for your housing payments.

Let us help you protect your tree of wealth. Whether you are looking to buy or sell new properties, it is crucial to have proper financial planning in protecting this new commitment a well as liability. Miscalculating of it will lead to becoming an expense in times of need. Our dedicated financial advisors are ready to work with you. We bring our wealth of experience and know-how of local policies to guide you through the most complex financial matters.

Simply fill in the form below and contact us for a non-obligatory consultation now!

Subscribe to our Telegram & Email Newsletter for immediate updates!