![Review: Best Careshield Life Supplement Option [In-Depth Analysis]](https://treeofwealth.sg/wp-content/uploads/2020/10/wooozxh-EmnZyCjHhgs-unsplash.jpg)

Last Updated on by Tree of Wealth

According to Ministry of Health, there is a high chance that Singaporeans could be severely disabled after retirement (65 years old). Long-term care is not cheap and there are many costs involved.

CareShield Life is an improvement over the previous ElderShield, administered by the Government and is a:

“long-term care insurance scheme that provides basic financial support should Singaporeans become severely disabled, especially during old age, and need personal and medical care for a prolonged duration (i.e. long-term care).”

Source: https://www.careshieldlife.gov.sg/careshield-life/about-careshield-life.html

What is CareShield Life?

A mandatory, nationwide disability protection scheme that pays a lifelong monthly benefit if you become severely disabled — defined as needing help with three or more everyday activities (ADLs). The benefit starts at S$612/month in 2025 and is designed to step up over time.

Premiums are paid through CPF MediSave and lower-income households receive government subsidies. Important to know: the monthly payout is helpful but may not fully cover actual long-term care costs like home nursing or assisted living.

Why do we need CareShield Life?

Facts – Disability a Major Risk

Think disability only matters in retirement? Think again. 1 in 2 healthy Singaporeans aged 65 could become severely disabled in their lifetime, and may need long-term care.

Severe disability may arise due to a sudden disabling event (e.g. stroke and spinal cord injuries) can affect younger adults too, and many of them are still working. Not to mention the worsening of chronic conditions and diseases (e.g. diabetes), or the progression of illnesses as we age (e.g. dementia).

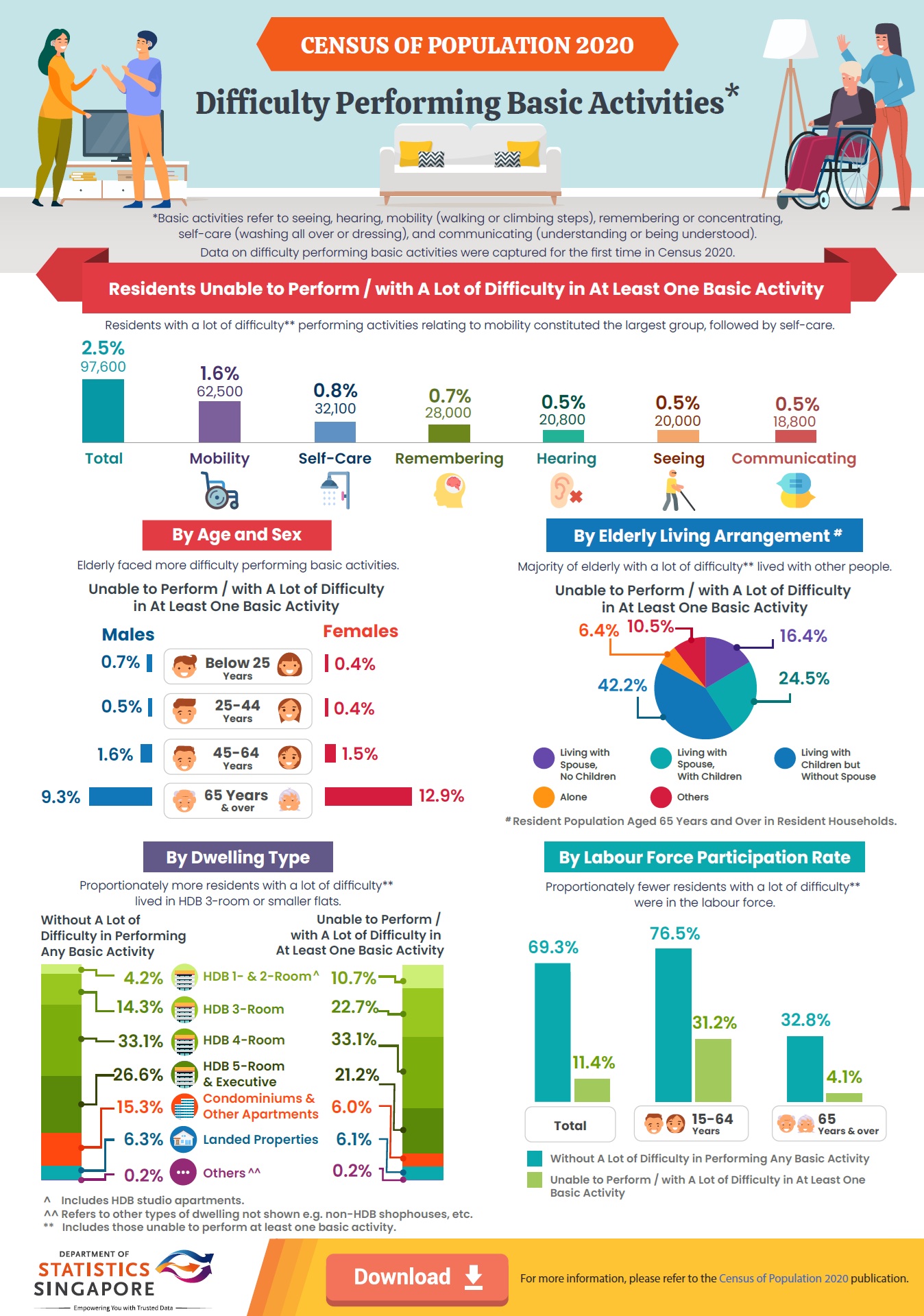

In 2020, 31.2% of residents aged 15–64 who were unable to perform — or had great difficulty performing — at least one basic activity remained part of the labour force. Even more striking: over half of CareShield Life claimants are under 40. So this isn’t a “someday” problem — it’s a present-day planning issue (picture unexpected rain at a picnic — annoying, costly, and best planned for ahead of time).

Road Fatalities

Bad luck on the road isn’t just an inconvenience — it can be life-changing. In 2024 Singapore recorded a five-year high in road fatalities and an increase in injuries (from 8,941 in 2023 to 9,302 in 2024).

Even otherwise healthy, working adults can be left with anything from temporary impairment to long-term disability — so thinking “it won’t happen to me” is a risky bet (and one you definitely don’t want to lose).

Long-term Care – Rehab, Home-based, Nursing Homes

Severe disability often means more than one hospital visit — it can lead to months or years of rehabilitation, day-care at care centres, regular home nursing, or even residential nursing care. Depending on the level of support, expect costs to start around S$1,000 a month and rise from there (specialist therapy, medical supplies and attendant wages add up fast).

For many families, that’s enough to wipe out emergency savings and force tough trade-offs — so a targeted care top-up or additional insurance can turn an impending financial headache into something manageable.

The real cost of disability care in Singapore

Severe disability isn’t just a medical issue — it carries serious financial consequences that can strain families and retirement plans. Government estimates show that half of otherwise healthy Singaporeans who reach age 65 are likely to experience severe disability in their lifetime. That’s not a distant “one day” problem — it’s a statistical probability many people should plan for now.

Here’s what typical long-term care can cost:

-

Live-in caregiver: roughly S$1,200–S$1,500 per month, depending on experience and duties.

-

Day-care centres: about S$900–S$1,600 per month for centre-based programmes and therapies.

-

Nursing homes: after subsidies, expect S$2,000–S$3,600 per month for residential care.

-

A healthy single elderly person (65+) needs S$1,379/month for basic needs (CNA study).

-

Elderly couple: S$2,351/month.

-

Ages 55–64: S$1,721/month. – Source: CNA

-

These figures exclude disability or long-term care costs.

-

Nursing home care for severe disability costs S$1,200–S$4,500/month – Source: Income.

-

Realistic estimate for someone severely disabled and needing full-time care: S$3,000–S$5,000/month.

Factor in annual increases in healthcare and care costs of about 6–8%, and you quickly see how a basic monthly support like CareShield Life’s S$612 (2025 baseline) may fall short of covering everyday care needs.

CareShield Supplements — what they do (and why they matter)

If CareShield Life is the foundation, supplements are the extra layer of protection you choose to add. These insurer-offered top-ups are optional but designed to reduce the shortfall between the base payout and actual care expenses. Common features include:

-

Higher monthly payouts that sit on top of the CareShield benefit.

-

Lower ADL threshold options — some supplements pay out if you lose ability in just one ADL, rather than three.

-

Additional protections such as lump-sum cash benefits, premium-waiver riders, or indexed payouts.

Two widely known supplements in Singapore are NTUC Care Secure and Singlife CareShield Plus — both aim to boost your monthly income in the event of severe disability, but their features, limits and pricing differ. If you’re serious about closing the protection gap, compare benefit levels, ADL triggers, claim rules and long-term affordability before you buy.

What is Activities of Daily Living (ADLs)

These are the everyday tasks that tell us if someone needs daily help — think of them as the basic survival checklist, but without the drama.

-

Washing — Being able to bathe or shower safely, which includes getting into and out of the tub or shower. If that’s not possible, being able to be washed by another method (e.g., sponge bath) still counts.

-

Dressing — Putting on, removing and fastening clothes — plus managing any medical aids like braces or prosthetics that need to be secured.

-

Feeding — Actually feeding yourself after the meal is prepared and on the table — not cooking, just eating.

-

Toileting — Using the toilet and handling bladder or bowel needs, whether independently or with the help of protective garments or medical appliances.

-

Walking or Moving Around — Moving from one room to another on level floors — the basic indoor mobility that keeps daily life ticking.

-

Transferring — Getting in and out of bed and moving to an upright chair or wheelchair (and back) without unsafe difficulty.

The definition for CareShield Life’s payout is Severely Disabled, and by that it means 3 out of these 6 Activities of Daily Living (ADLs).

However if a major disability were to occur and cannot perform 1 or 2 out of the 6 ADLs, there will be no payouts from CareShield Life at all.

Enter Careshield Life Supplement

| CareShield Life | CareShield Life Supplement Upgrade |

| $600 Monthly Payout | Up to $5,000 Monthly Payout |

| Lifetime Payout | Lifetime Payout |

| 3 out of 6 ADL’s | 2 out of 6 ADL’s |

| MediSave Payable | MediSave Payable (Up to $600) and Cash |

As Long-term care is getting income and cost of care replacement in the event of severe disability (emphasized more as the person ages), CareShield Life is ultimately a basic coverage and may not be enough to pay for any of those and survive with a $600 monthly payout. With or without using cash, supplement plans give you the choice to go for a higher monthly income at up to $5,000 at a less severe claim criterion, which leads us to the second point:

CareShield Life’s payout criterion is set at the inability to perform 3 out of 6 ADL’s. CareShield Supplement plans have lower criteria at 2 out of 6 ADL’s. Additionally, you can utilize your MediSave account with an Additional Withdrawal Limit (AWL) of $600 to get this supplement plan. If the premium exceeds $600, the remaining amount can be paid by cash (read more for premium table).

Below we look at the comparison of insurer’s features as well as pros and cons of their supplementary CareShield Life plan.

Features Comparison: Singlife VS Income

| Feature | CareShield Life (Govt) | Income — Care Secure Pro | Singlife — CareShield Plus |

|---|---|---|---|

| Monthly payout (2025) | S$612 | S$200–S$5,000 (in S$10 increments) | S$200–S$5,000 (in S$100 increments) |

| Partial disability (1 ADL) | Not covered | Covered | Covered |

| Lump-sum benefit | None | Yes | Yes |

| Caregiver benefit | None | 60% of disability benefit, payable up to 12 months (for 2+ ADLs) | 60% of disability benefit, payable up to 12 months (for 2+ ADLs) |

| Dependent benefit | None | 25% of disability benefit, payable up to 36 months (for 2+ ADLs) | 20% of disability benefit, payable up to 36 months (for 2+ ADLs) |

| Death benefit | None | 300% of disability benefit | 300% of disability benefit |

| Premium waiver on disability | Yes | Yes | Yes |

| Payable via MediSave | Yes | Yes (up to S$600/year) | Yes (up to S$600/year) |

Premiums — example (35-year-old male, S$1,300 disability benefit):

-

NTUC Income — Care Secure Pro: S$589/year (fully payable via MediSave).

-

Singlife — CareShield Plus: S$679/year (S$600 via MediSave, S$79 cash).

Policy term note: both supplement examples above are shown as payable until age 99.

NTUC Income — Care Secure Pro

What it does (quick): pays out earlier than CareShield Life — you can receive monthly benefits from 1 ADL (not just 3). You pick your monthly payout (in S$10 steps), get a one-off lump sum on disablement, and premiums can be paid via CPF MediSave (up to S$600/year per insured). A premium-waiver feature keeps the policy running if disability stops premium payments.

Why you might like it

-

Covers earlier-stage disability (trigger from 1 ADL) so you get help sooner.

-

Lump-sum on claim helps cover immediate costs (renovations, equipment, deposits).

-

Very strong payout for single-ADL events — 60% of the benefit, payable up to 60 months (highest among competitors).

-

Flexible benefit sizing — choose monthly cover in S$10 increments.

Watch-outs

-

Premiums can be pricier than rivals for the same headline payout.

-

No built-in option to automatically increase the benefit over time.

Singlife — CareShield Plus

What it does (quick): similar to NTUC’s option, it pays for partial disability from 1 ADL, offers choice of monthly payout, a lump-sum on disablement and a premium waiver on claim. Premiums are payable via CPF MediSave.

Why you might like it

-

Generally competitive pricing — good value for money.

-

You can boost benefits at certain life-stage events without new underwriting (handy when you want more cover later).

-

Optional escalation: choose 2% or 3% annual increases to protect against inflation.

Watch-outs

-

Benefit jumps are in S$100 blocks (less granular than NTUC’s S$10 steps).

-

Partial-disability payout timing is shorter: 100% of benefit for up to 12 months for 1 ADL.

Which CareShield supplement suits you?

-

I just want the basics: CareShield Life is mandatory and gives you the foundation — the safety net everyone has.

-

I need cash up-front when something happens: NTUC Care Secure Pro is built for that — stronger lump-sum support to help with immediate bills and care setup.

-

I want lower premiums and steady income: Singlife CareShield Plus tends to be kinder to the wallet and suits long-term income planning (plus options to grow cover over time).

Bottom line

CareShield Life provides a universal floor, but with long-term care costs often topping S$2,000/month, the base payout alone usually isn’t enough. Both NTUC Care Secure Pro and Singlife CareShield Plus can help close the gap — the right pick depends on your budget, family needs and whether you prefer upfront cash or ongoing income.

👉 Want a side-by-side illustration for your situation? Speak with a licensed adviser and get a clear, no-pressure comparison.

Queries and want to find out more? Simply fill in the form below and our licensed professional financial advisor will get in touch with you. We work with professional financial advisors comparing and analyzing to provide non-biased solutions for you, based on your concerns and individual needs. Also adhering to your privacy, your given information will only be used to communicate with you.

FAQ — CareShield Supplements (Singapore, 2025)

Q1 — What is CareShield Life and do I need a supplement?

CareShield Life is Singapore’s mandatory long-term care scheme that pays a monthly benefit if you become severely disabled. The headline support starts at S$612/month (2025), which is helpful — but it’s often not enough to cover real-world care costs. Many people buy a supplement to top up payouts or get extra features (earlier triggers, lump sums, premium waivers).

Q2 — How do NTUC Care Secure Pro and Singlife CareShield Plus differ?

Both increase your payout above the CareShield base, but they lean into different strengths: NTUC Care Secure Pro focuses on bigger upfront support and strong partial-disability payouts; Singlife CareShield Plus offers competitive premiums and options to automatically grow your benefit over time to combat inflation.

Q3 — Can I pay supplement premiums with MediSave?

Yes — approved CareShield supplements can be paid using MediSave, up to S$600 per insured person per year. Check product rules for exact MediSave limits and eligibility.

Q4 — Which supplement is “best” in 2025?

There’s no single winner — the right plan depends on what you value: immediate lump-sum help and stronger partial-disability cover, or lower premiums and indexed/ escalating payouts. Run a personalised comparison to see which fits your budget and family needs.

Q5 — How much does long-term disability care actually cost?

Costs vary, but ballpark monthly ranges are:

-

Live-in caregiver: S$1,200–1,500

-

Day care centres: S$900–1,600

-

Nursing homes (after subsidies): S$2,000–3,600+

With care prices rising each year, the CareShield base alone often leaves a shortfall — supplements can help bridge it.

Confused about what fits your situation? No sales pressure — we’ll run a quick, no-obligation side-by-side illustration so you can compare premiums and payouts. Leave your details in the form below or WhatsApp us to get started.