Last Updated on by Tree of Wealth

This plan has been withdrawn since Feb/March 2021

When AIA introduced the Triple Critical Cover previously, they took a dramatic turnaround in its advancement of critical illness insurance plan. That insurance plan happens to be the first in the market to ever provide a multi payout option for critical illness insurance plan.

Just when everyone thought this was the height of innovative ideas in the insurance company, AIA decided to spring up another jaw-breaking surprise into the market by introducing the AIA Power Critical Cover (PCC).

This insurance plan is designed to stand out as insurers are presently coming out with designing insurance plans available to all and sundry. With some pretty awesome and unique next-gen ideas, the AIA Power Critical Cover makes insurance more inviting as it expands on new options and modifies some of the options in AIA Triple Critical Cover.

Let us have a look at the features that make it stand out:

AIA Power Critical Cover Product Features and Benefits at a Glance

Sum Assured Maximum Payouts

Maximum Sum Assured – $2, 000, 000

Early Stage CI Maximum Payout – $250, 000

Intermediate Stage CI Maximum Payout – $350, 000

Advance Stage CI Maximum Payout

- 100% of Sum Assured

- Able to claim up to 5 times of CI for different stages and different conditions.

- 12 months (1 year) of waiting period in between each claim.

- 149 Total Stages of Critical Illnesses from Early to Intermediate to Advance stage.

Special & Juvenile Conditions

Additional 20% of sum assure for juvenile benefits.

- Capped at $25, 000 for each condition

- Claim up to 10 times for different Juvenile & Special Conditions

List of Conditions

- Diabetic Complications

- Osteoporosis

- Severe Rheumatoid Arthritis

- Dengue Haemorrhagic Fever

- Mastectomy due to carcinoma-in-situ or malignant

- Breast condition

- Hysterectomy due to cancer

- Vulvectomy due to cancer

- Severe Gout

- Necrotising Fasciitis requiring surgery

- Tourette Syndrome (TS)

- Attention-deficit Hyperactivity Disorder (ADHD)

- Autism Spectrum Disorder (ASD)

- Dyslexia

- Kawasaki Disease with Heart Complications

- Rheumatic Fever with Heart Involvement

Pre Early Benefit

Chronic Disease Benefit

Pay up to 10% Sum Assured Capped at $10,000 x 2

Cardiovascular Disease Benefit

Pay up to 10% Sum Assured Capped at $25,000

Benign and Borderline Malignant Tumour benefit

Pay up to 10% Sum Assured Capped at $25,000

Early/Intermediate/Advance Stage Critical Illness Claims

There is a 100% of sum assured able to claim up to 5 Claims of it for different Early to Intermediate to Late Stage CI with a 12 months/1 year waiting period in between each claim.

Power Relapse Benefit

In the event of recurrence/re-diagnosis of Power Relapse Critical Illness, 100% of the sum assured will be paid or required to undergo a surgery for these Power Relapse CI 2 years after the first diagnosis. Explained in details below under “New Features”

Power Relapse Critical Illness

• Re-diagnosed Major Cancer

• Recurred Heart Attack

• Recurred Stroke

• Repeated Major Organ Transplant / Bone Marrow Transplantation

• Repeated Heart Valve Surgery

ENJOY 5X POWER RESET OPTION

Previously, the AIA Triple Critical Cover presented us with the option of “reset” just three times. AIA Power Critical Cover has added two more options to the window, making it five. This means you can enjoy 100% of sum insured in the form of sum assured, provided your insurance policy remains in form after one year of your last critical illness diagnosis.

This also means the waiting period per claim is 12 months (1 year).

Better Surrender Value Options With 1% Increase Option From 76 Years Old

The previous Triple Critical Cover has a surrender value feature that you can exercise once you clock 75 years old. For the new Power Critical Cover however, an additional option has now been included. You can now start exercising your surrender value feature either after celebrating 60th policy anniversary or when you turn 75 years of age, whichever comes first. So, you get to choose from these two options. This surrender value feature works for Coverage to 100 years of age.

You should, however, note that this feature will no longer be valid or apply to you once you have made any critical illness claim during the running period of the life policy.

Another unique feature that stands Power Critical Care out is that from the age of 76 years, you get to enjoy 1% annual increase of the sum assured from the life assured.

One More Thing: Death Benefit

Another interesting point to note about AIA Power Critical Care is that it still provides the option of enjoying 100% sum assured for death, provided no CI claim was made during the lifetime of the insured.

For most stand-alone critical illness plans, there are no death payouts, but only a small death benefit if death occurs, with no returns on premiums.

NEW FEATURES!

PRE EARLY STAGE CI PAYOUT BENEFIT

AIA is a standout of the pack with this interesting additive. This means the insured can enjoy a payout option for critical illnesses that are at their pre early stages. They further classified this into three main categories, each with specific considerations and limitations.

CATEGORY 1: CHRONIC DISEASE BENEFIT

This category allows the insured to enjoy a payout as much as 10% sum assured cap at $10,000. The insured can make up to two claims on two separate chronic disease of the percentage sum assured. The following chronic diseases are reckoned with in this category:

- Type 2 Diabetes Mellitus

- Spinal Disease

- Thyroid dysfunction: Hyperthyroidism and Hypothyroidism

- Gastrointestinal disease involving surgery

CATEGORY 2: CARDIOVASCULAR DISEASE BENEFIT

This category allows you to enjoy a claim of up to 10% sum assured or capped at $25,000. Only one disease can be claimed in this category subjected to the above condition. The following are the recognized cardiovascular disease:

- Wolff Parkinson White and Supraventricular Tachycardia with surgical intervention

- Congenital Septal defect requiring surgery

- Chronic Rheumatic Heart Disease

- Severe Deep Vein Thrombosis with Pulmonary Embolism

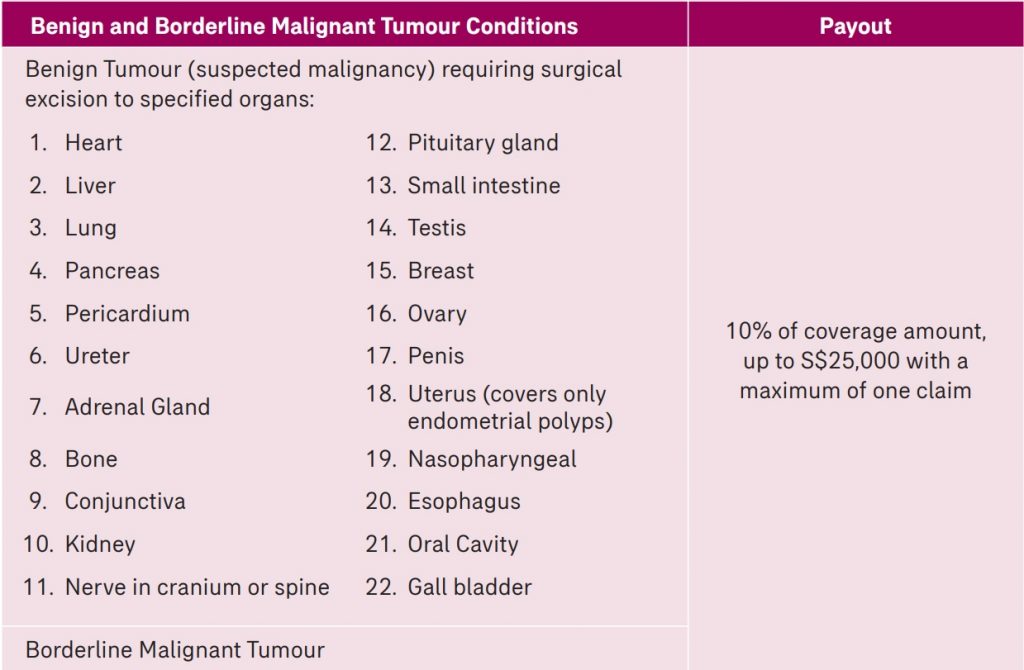

CATEGORY 3: BENIGN AND BORDERLINE MALIGNANT TUMOR BENEFIT

This is the last of the three categories, and the insured can also enjoy up to 10% sum assured cap at $25,000, and just like the second category, only one of this illnesses can be claimed.

Benign and borderline malignant tumor require definitions. In AIA’s case simply means:

A complete surgical excision of a non-cancerous benign lesion (tumour) confirmed in written form by a certified pathologist upon histopathological examination. The lesion must be excised from any of the 22 specified organs present in the table below:

POWER RELAPSE BENEFIT

This benefit is opened to “power relapse critical illnesses” provided there is a recurrence/re-diagnosed of the illness at least two years after the first diagnosis. Also if there is any surgical procedure associated with any of the power relapse illnesses two years after it was first diagnosed. The insured enjoys 100% of the sum assured for any of these illnesses, and this does not in any way affect the power reset option.

The “power relapse critical illnesses” are:

- Rediagnosed Major cancer

- Recurred Heart Attack

- Recurred Stroke

- Repeated Major Organ Transplant or Bone Marrow Transplantation

- Repeated Heart Valve Surgery

It is crucial, however, to note that this claim can only be enjoyed once and up to two recurred or repeating Critical Illness.

The AIA Power Critical Cover is so much more significant because it makes provision for more conditions:

Pre-early benefits- 10 conditions

Early to Intermediate to Advance Stage – 150 critical illnesses

15 special conditions

With a total of 175 conditions, this is the only known plan that covers this number of conditions.

How AIA Power Critical Cover Works

What We Like About The Plan

- Pre-early Condition Benefits – Conditions before Early Stage CI

- The number of conditions covered increased from 104 to 175

- More payout guaranteed; up to 940% sum assured

- Better surrender cash value feature (2 choices), permitting up to 100 years

- Death benefit having a higher sum assured than every other plan

- Same CI at different stages can permit separate claims (subjected to waiting period)

What We Don’t Like About The Plan

- One year waiting period in between the first early stage critical illness claim and second different early/intermediate/advance stage CI as opposed to other plans in the market which have no waiting period

- The premium package is quite expensive until 75 years old

- Lack of flexibility: Only covers till ages 75 and 100, no other options

AIA Power Critical Cover Conclusion

Make the right informed choices about critical illness coverage. Our professional licensed FA advisor will see to it that your coverage is well managed. Kindly indicate your interest in getting the quotations and assessment by filling the form below.

Based on your needs, a custom made solution will be adjusted only addressing your concerns.

No obligations, no hidden fees. All advice are of no charges.