Last Updated on by Tree of Wealth

The Manulife RetireReady Plus (III) is a recurring premium participatory endowment scheme, aiming to provide benefits in the form of retirement income. While it may be categorized under savings plans, its primary design focuses on fostering your retirement preparedness, a function analogous to an annuity plan.

Regarding eligibility and features, the entry threshold for the premium stands at an affordable S$694.24 per annum and the plan does away with the need for medical underwriting, facilitating a smoother enrolment process.

Manulife ReadyRetire Plus III Product Features and Benefits at a Glance

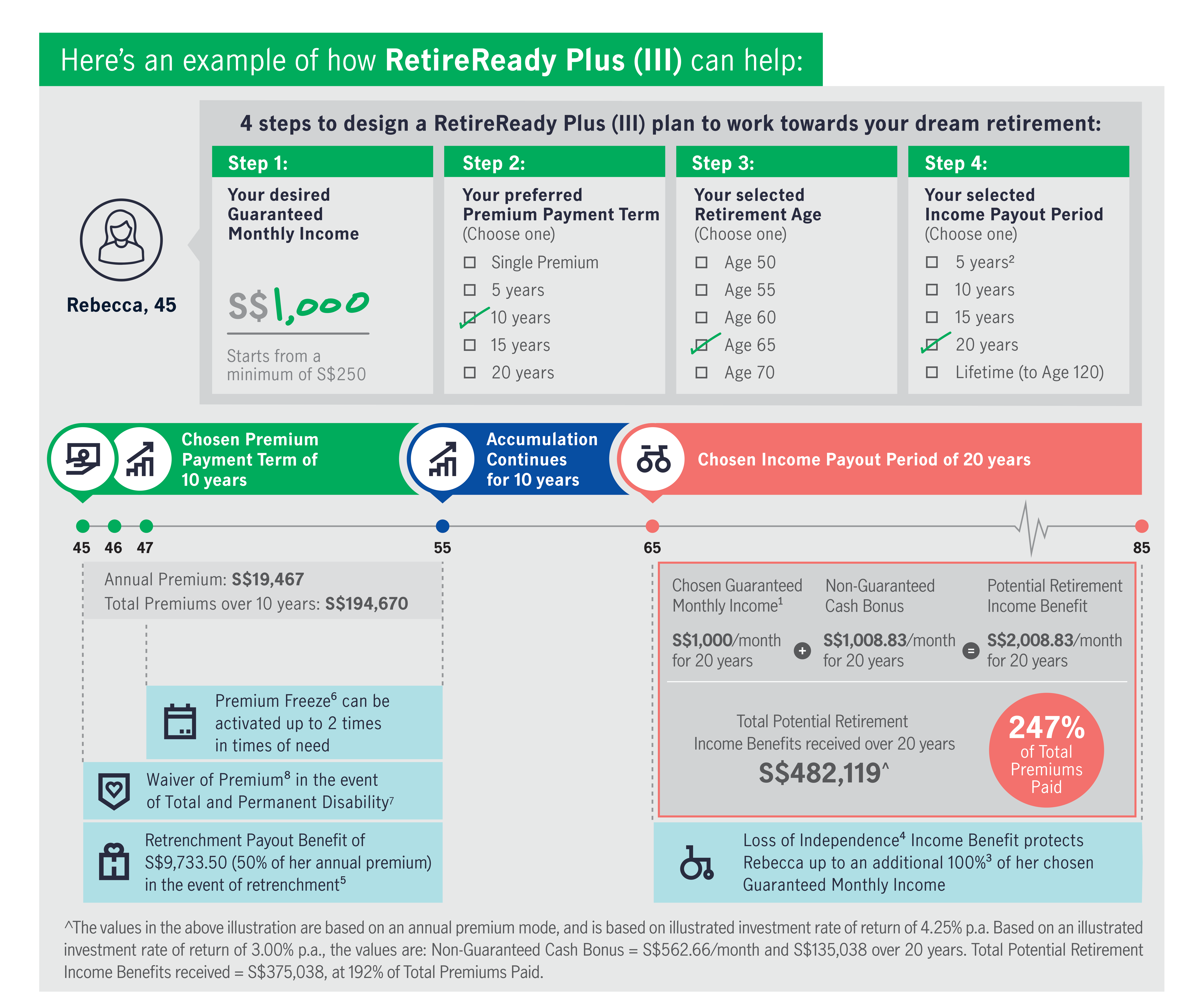

Manulife’s offering is a flexible retirement plan that promises you a guaranteed monthly income for life among other key benefits. The Manulife RetireReady Plus will ensure that you can get a steady income even in your retirement years while giving you an allowance to tailor your retirement plan according to your needs. Tailored to aid in retirement planning, you’re allowed to specify your retirement age, the amount of guaranteed monthly income (GMI), and the preferred period for income payout. The available choices for retirement age are from 50 to 70 years, while the period for income payout varies from 5 years up to a lifetime.

Premium Term Available

The plan offers four different terms for premium payment – 5, 10, 15, or 20 years. For those who can afford it, there’s an option to make a single lump-sum payment as the premium.

Allocation of Premium

The minimum premiums that you’re required to pay are already net of any associated fees or charges. This implies that the full 100% of your premiums is allocated towards purchasing units of the participating fund. Manulife utilizes a specific asset allocation strategy to ensure your policy remains solvent, guarantees the promised benefit, and capitalizes on emerging opportunities. Bonds, falling under the category of fixed-income assets, contribute to the majority of your guaranteed benefits. This class of assets also includes cash and money market instruments. On the other hand, your non-guaranteed bonuses stem from investments in public equity, private equity, and real estate assets, given their potential for yielding higher returns.

Methods of Payment

Aside from the traditional option of making your premium payments in cash, you have the alternative of paying with your Supplementary Retirement Scheme, especially if you’re opting for a single premium and the plan is for self-insurance.

Make Use of Your SRS Account – Save on Tax and Retirement

To further enhance your retirement planning, you are able to make use of your SRS funds, growing them even more for your retirement.

The Supplementary Retirement Scheme (SRS) is a savings account that can complement your CPF savings while also allowing you to enjoy tax deferment once you transfer it to your retirement plan. Manulife RetireReady Plus allows you to use funds from your as a single premium. If you are already contributing to your SRS account regularly, consider saving it into this retirement plan to further enhance your retirement earnings!

Options for Payout

Payouts under the RetireReady Plus III are made as Retirement Income Benefit (RIB). Upon reaching your chosen retirement age, you have two options: receive your RIB, or accumulate and reinvest your RIB with Manulife at a non-guaranteed interest rate. By default, you’ll receive your RIB on a monthly basis, unless otherwise specified. If you opt to receive your RIB, you’ll receive a guaranteed amount monthly, which you selected at the time of policy purchase, plus any cash bonus for the chosen payout period. It’s worth noting that cash bonus amounts aren’t guaranteed, and Manulife will first offset any amounts due to them. In case your plan is terminated, the payouts will cease. If you choose to keep accumulating your RIB, remember that your interest rate is decided by Manulife and may change with a 30-day notice. You’ll be pleased to know that you can withdraw part or all of your retirement income plus any income at any time, subject to a minimum withdrawal value of S$500 or withdrawal of the remaining balance, but only after you’ve reached your chosen retirement age.

Maturity Benefits

Upon the maturity of your plan, which effectively ends your policy, you’ll receive the final guaranteed monthly income amount (GMI), the last cash bonus, and any reinvested RIB with interests. Any amounts due to Manulife will first be deducted from the payout.

Flexibility of Plan to Change Income Pay-Out Period

With Manulife’s RetireReady Plus III policy, you’re granted the flexibility to adapt your income payout period in response to evolving retirement plans. From the commencement of your policy up to two years before your selected retirement age, you can submit requests to modify this period. After approval from Manulife, your Guaranteed Monthly Income (GMI) is suitably adjusted, leaving the subsequent premiums for the basic plan and additional benefits unaffected. Any cash bonus or Loss of Independence (LOI) income benefit entitlement will be computed based on the updated GMI, with the LOI benefit’s payable period revised to align with the new payout term. This flexibility proves advantageous if your financial needs shift over time, offering the ability to tailor your monthly cash payout duration prior to your first payout. Whether you initially anticipate needing payouts for 10, 20, or 30 years post-retirement, life’s unpredictability necessitates this capacity for adjustment to ensure your retirement plan remains responsive to your needs.

Option to Pause Premium Payments

The option to freeze premium payments for a year, while still keeping your policy active, is available under certain conditions. To qualify for this, your policy must be in force for a minimum of 2 policy years, during which all premiums have been fully paid. After approval of your freeze request, the due premiums, along with premiums for any riders, will be waived for 1 year, beginning from the next premium due date. If you’ve opted for the 5-year premium payment term, you’re allowed to apply for a premium freeze once. For longer payment terms (10, 15, and 20 years), you can apply for a freeze twice. During the premium freeze, you’re exempted from premium payments; however, the retrenchment payout benefit and retirement income benefit won’t apply. The maturity date and premium payment term will be extended by a year for each instance of exercising the freeze option. Likewise, the benefit end date for death, terminal illness, and loss of independence (LOI) income benefits, as well as the waiver of premium on Total Permanent Disability (TPD), will be extended by a year.

Bonus Features

Bonuses are not guaranteed and are contingent on the performance of the plan’s participating fund. The level of bonus you’ll receive is determined annually, after evaluating the fund’s performance. Cash bonuses, if declared by Manulife, are paid as part of your monthly RIB starting from your chosen retirement age. It’s important to note that these cash bonuses are not guaranteed until they’re declared for payout in a specific year. The formula to calculate the monthly cash bonus is as follows: Monthly cash bonus = (Cash bonus rate[%] x GMI) / 12 months. The percentage of the cash bonus varies based on factors like the insured person’s age at policy issuance, gender, chosen retirement age, premium payment term, and chosen period of income payout.

In certain cases, you might be entitled to a surrender bonus if you surrender your policy starting from the final policy year when you’re required to make premium payments. This bonus, calculated as a percentage of your GMI, will be paid to you only if declared by Manulife.

In the event of a terminal illness or death claim, you may be eligible for a claim bonus, which will be paid only if declared by Manulife. The claim bonus, similar to the surrender bonus, is calculated as a percentage of your GMI.

Income Benefit for Loss of Independence (LOI)

The LOI income benefit comes into effect if you experience a severe disability during your chosen income payout period. After a deferment period of 90 days from the date of your claim, the LOI benefit will be disbursed with your next Retirement Income Benefit (RIB) payment. Eligibility for this benefit depends on meeting Manulife’s definition of LOI, as detailed below:

- If, even with the use of special equipment, you are unable to carry out any two out of six daily living activities and need constant assistance, you will receive 50% of the Guaranteed Monthly Income (GMI), up to a maximum of S$2,000 per month.

- If, even with the help of special equipment, you are unable to perform at least three out of six daily living activities and need constant assistance, you will receive 100% of the GMI, up to a maximum of S$4,000 per month.

- In case you suffer from any of the specified disability illnesses, you will receive 100% of the GMI, up to a maximum of S$4,000 per month. The specified disability illnesses include irreversible loss of speech, deafness, and major head trauma, each with its own specific criteria.

Please note, if your condition improves or worsens, the benefit amount will adjust accordingly. The LOI benefit will cease in case of the insured’s death, policy maturity, or if the insured no longer meets the criteria for LOI.

Retrenchment Payout Benefit

If you are retrenched and remain unemployed for at least 30 continuous days from the date of retrenchment, the RetireReady Plus III policy provides a retrenchment payout benefit. To claim this benefit, you must submit a request to Manulife within six months from your retrenchment date, using their prescribed form. You can avail of this benefit provided you are below 65 years of age at the time of retrenchment.

The retrenchment payout comprises a lump sum amounting to 50% of your total annual premium. The total annual premium refers to the yearly premium amount for your basic plan and supplementary benefits. If you turn 65 before the end of your premium payment term, subsequent premiums won’t include the amount for this benefit as coverage ceases from the policy anniversary immediately after you turn 65 years old.

The retrenchment payout benefit can be claimed only once during your plan’s term, and it will be discontinued after the payout. This benefit does not apply to corporate-owned policies or to new policyholders who join at age 65.

Waiver of Premium on Total and Permanent Disability (TPD) Benefit

If you become totally and permanently disabled (TPD) before the end of your premium payment term or before your TPD expiry date (the anniversary of your policy after you turn 70 years old), you will be eligible for a waiver of future basic premiums. The disability must last for at least 6 continuous months before a claim can be made. The definition of TPD varies with the insured person’s age as outlined below:

- Before the insured person’s 18th birthday: The insured requires constant care due to an accident or sickness and needs to stay in a hospital or at home perpetually.

- After the insured person’s 18th birthday and before their 65th birthday: The insured cannot earn any income from work or their business which is expected to be permanent, or they cannot perform at least three out of six Activities of Daily Living even with special equipment and constant assistance.

- After the insured person’s 65th birthday and before the TPD expiry date: The insured cannot perform at least three out of the six Activities of Daily Living even with special equipment and constant assistance.

- At any age before the TPD expiry date: The insured has suffered total and permanent loss of vision in both eyes, loss of use of two limbs, or loss of vision in one eye and loss of use of one limb.

Death Benefit

Upon the insured’s death, the amount paid out will depend on when the death occurs. If the insured dies before the income payout period and the policy is in force, the payout will be the higher of 105% of total premiums paid or the guaranteed surrender value, along with any claim bonus. If death occurs during the income payout period and the policy is in force, the payout will be the higher of 105% of total premiums paid less the total Guaranteed Monthly Income (GMI) declared, the guaranteed surrender value, or 12 times of the GMI, along with any claim bonus and accumulated Retirement Income Benefit (RIB) plus interest.

Terminal Illness (TI) Benefit

If you are diagnosed with a terminal illness (TI), whereby you are expected to pass away within 12 months from the diagnosis date, you will receive the death benefit as a lump sum under the RetireReady Plus III Plan. The diagnosis must be confirmed by a medical examiner and another examiner appointed by the company. The maximum payout for TI and critical illness (CI) is S$2,000,000, with a maximum limit of S$1,000,000 for TI.

Surrender/Ending the Policy

Your policy ends at the earliest of the following: your written request to surrender the plan is received by Manulife; your benefits end date; when the maturity benefit is paid out to you; when the policy lapses; when the death benefit is fully paid out to you due to a TI claim or other supplementary benefits are eligible for full accelerated death benefit; or when the insured passes away.

If you choose to surrender your plan, you will receive the guaranteed surrender value, any accumulated RIB with interest, and any surrender bonus, provided that you have made all your premium payments for 2 years. The value received will be net of any amounts you owe to Manulife. The specific surrender value of your plan will depend on your basic plan and the policy illustration’s projections. Click below to get in quote!

Coverage Add-ons (Riders)

For the RetireReady Plus III policy, Manulife offers a couple of rider options. These include:

- Cancer Care Premium Waiver: This rider allows for the waiver of future premiums on your base policy and riders (if any) in the event you are diagnosed with cancer.

- Critical Care Waiver: This rider provides for the waiver of future premiums on your base policy and riders (if any) if you are diagnosed with one of the covered critical illnesses.

Fees and Charges

The RetireReady Plus III policy does not have any separate fees and charges. The minimum premium amounts stated are net, which means that all fees and charges have already been accounted for in the premium amount.

Hassle-free Application

Applying for the RetireReady Plus III plan is straightforward and does not require any medical underwriting. This means that you do not need to answer any health-related questions in your application, ensuring a guaranteed acceptance from Manulife.

How Manulife ReadyRetire Plus III Works

Why it is a good choice?

Competitive Endowment Returns

If you pay premiums of S$19,467 annually for 10 years, your total premiums paid would amount to S$194,670.

Guaranteed Portion

If the policy guarantees a payout of S$1,000 per month for 20 years, this would total to S$240,000.

Non-Guaranteed Portion

Assuming a projected rate of return (ROR) of 4.75% per annum, the non-guaranteed portion (additional payouts beyond the guaranteed S$1,000 per month) would amount to approximately S$242,119.20 over 20 years.

Total Received

By adding the guaranteed and non-guaranteed portions together, you would receive a total of S$482,119 over the 20-year payout period.

Over the duration of this retirement plan, you get an annual bonus even before you choose to retire and a cash bonus once you select your age of retirement. With Manulife RetireReady Plus III, you get to make two flexible choices. This includes the choice of a limited premium term that includes a single premium, 5, years, 10, 15 and even 20 years. You also get to choose your retirement age from 50 up to 70 years but at five year intervals. There is also flexibility in your payout term as the retirement plan allows you to choose a payout term of 5, 10, 15, 20 or even a lifetime payout.

Other essential benefits include a disability benefit that waives all future premiums in case the insured is unable to carry out a minimum of 2 out of 6 activities necessary for daily living (ADLs). This includes an additional guaranteed 0.5x Monthly Income benefit in case you lose 2/6 ADLs independence in your retirement payout period. In the event of unable to perform 3/6 ADLs, there will be an additional guaranteed 1x Monthly Income benefit.

The plan does not need any medical underwriting and you have the choice to pay via Single Premium through the Supplementary Retirement Scheme.

At the end of the day, retirement is what you need to plan for and starts today. This is because all of us only have finite and fixed limited years towards old age and retirement.

Are you considering retirement planning? Let us do the homework and help you compare across the different retirement plans in the market to save you time. Drop us an inquiry below and our professional experienced licensed FA advisor will get in touch with you shortly upon your request.

No obligations. No hidden fees and costs. Just professional advice.