Last Updated on by Tree of Wealth

Manulife’s first ReadyBuilder was one of the first few legacy endowment plans in the market, having a maturity period until 120 years old. There are currently a few similar products out there, and Manulife’s Ready Builder II stood the test of time and is still one of the better endowment plan in the market right now.

It offers flexible withdrawals anytime you need it (and when it accumulates wealth), great versatility, option to leave behind to family member to continue to compound your wealth, as well as the option to pause premium payment in the event of involuntary unemployment that has been prolonged.

This plan is all about: Flexibility withdrawals, long lasting compounding, as well as Life Insured – changing to a younger life insured leaving the wealth compounding to the next generation.

One of the key feature of ReadyBuilder II is that it has flexible withdrawals and this makes it very versatile to fit in to many forms of wealth planning for your needs:

- Very suitable for children’s education

- Planning for retirement

- B.T.I.R (Buy Term Invest the Rest)

- Legacy planning

Features At a Glance for Manulife ReadyBuilder (II)

Flexible Cash Value Access

Have the choice to withdraw your money whenever you need it. Cash value starts to accumulate and grow after the 1st year. As you can withdraw anytime, we strongly recommend withdrawing it after the 15th year when your capital has break even (more on this below). You can withdraw to fund key milestones in life, which brings to the next point:

Withdraw Cash At Life’s Milestones

- There is no structured cash benefit payout terms and once there is cash value, you actually can start to withdraw the amount out. It is however much advised to withdraw the amount after it has break even (15th year).

- The plan gives you the flexibility to withdraw the accumulated cash value at the intended life’s interval time, which we will show you how to utilise in 4 main scenarios below

- Flexible Premium Terms: Single Premium, 5, 10, 15, 20 years.

- For Single Premium option, choose to use cash or with Supplementary Retirement Scheme (SRS).

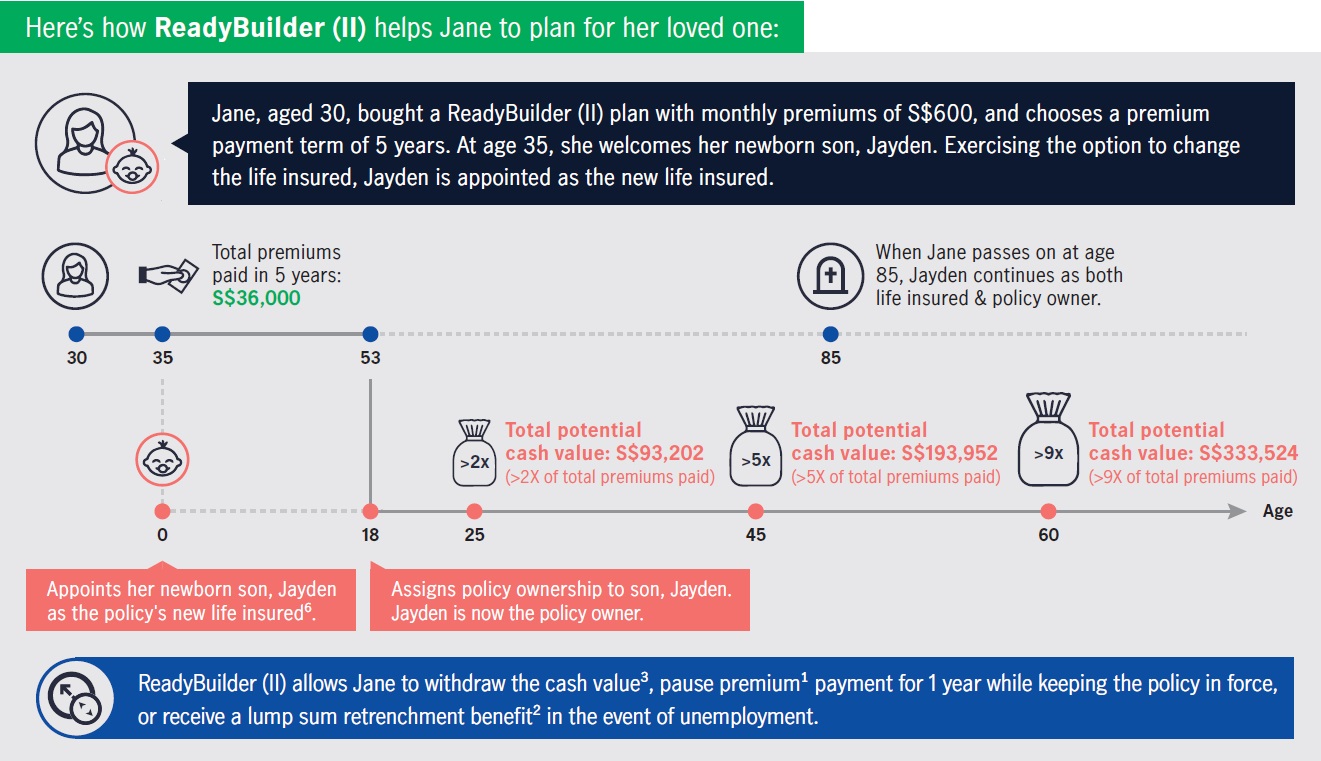

Wealth Accumulation: How to Take Advantage of the Maturity at 120 Years Old Feature & Change of Life Insured Option.

- The long horizon of the savings term helps accumulate and compound the wealth as the plan only matures at age 120.

- Wealth accumulation continuity – You can change the Life Insured after 2 years into the plan to continue accumulating your wealth and growing with them through their lifetime.

- Policy will only expire on the 120th birthday of the primary policyholder (which is you). Even if the primary policy holder is no longer around (death occurs), the plan will act as an ongoing wealth compounding interest garnering instrument for the SLI.

- This is especially useful for long term and even to leave it to the next generation. This is because traditional savings plan will be terminated upon death.

- However as the supposed accumulation compounding period is until age 120 of the primary policy holder, it will literally compound for decades for the next generation.

- You can appoint your spouse or child with insurable interest

- If this is bought upon the child’s birth, the plan will break-even on the child/s 15th birthday, making the plan very long lasting even if the primary policy holder is not around, as it will only mature on the primary policy holder’s 120th birthday.

Guaranteed Issuance

- No medical check-up, no health underwriting procedure. Issuance of the plan is guaranteed.

Early Break-Even – Capital Guaranteed

- Total Premiums paid will breakeven on the 15th year of the policy regardless of the premium payment term, be it 5, 10, 15 or 20 years.

- Guaranteed amount will be slightly higher than total premiums paid on the 15th year.

- Single premium (For cash and SRS), the breakeven year is early, on the 10th year.

- One thing good to note is, the non-guaranteed investment yield (projected at 3% and 4.25%) hasn’t been added on to this consideration.

Premium Term

Range of premium term from 5, 10, 15, 20 years or Single Premium (once)

Protection Coverage

Covers for Death and Terminal Illness. Waiver of Premium on TPD (Total and Permanent Disability) available only for regular premium term plans (5, 10, 15, 20 years).

Retrenchment Benefit

In the event of your retrenchment, receive a lump sum payout.

Supplementary Benefit (Riders)

Customise your protection by adding optional riders to cover for Critical Illness, Death, TPD (Total and Permanent Disability). Only for regular premium plans.

Manulife’s ReadyBuilder II Versatility

Next, we are going to be comparing against a few different combination permutations of BTIR, Children Education and Retirement plans to show the versatility of Manulife’s ReadyBuilder II. The plans that we are comparing with are some of the most competitive plans in the market.

1. Retirement Planning for Late 20s to mid 30s & early 40s

Retirement plans usually requires you to save regularly over a period of time, accumulate, then starts to pay out to you at a chosen retirement age, usually at 55, 60, 65 or even 70 years old. Payout period is also typically for 10, 20 or 30 years.

A feature for retirement plan is that it will pay out a guaranteed sum monthly during the payout period whereas Manulife’s ReadyBuilder II is flexible withdrawal.

|

Aviva MyRetirementChoice III |

Manulife

ReadyBuilder II |

|

| Premium Term | 15 years | 15 years |

| Premium Amount | $8,008.80 | $8,016.66 |

| Payout Structure | Payout Age: 50 Years old

Guaranteed Monthly Benefit: $1,110 ($13, 320 yearly)

Payout Period: 10 Years

|

Flexible Withdrawal with minimum amount.

It is strongly advised to withdraw the cash value after it breaks even (15th year) |

Guaranteed Cash Payout:

| Aviva

MyRetirementChoice III |

Manulife

ReadyBuilder II |

|

| 50 years old | $13,320 | $123, 906 |

| 55 years old | $13,320 | $126, 457 |

| 60 years old | $13,320

(Plan terminates after 10th year) |

$ 131, 378 |

| 65 years old | NA | $ 155, 556 |

| 70 years old | NA | $ 164, 608 |

It is important to note that for Manulife’s ReadyBuilder II, the amount shown is the total amount available.

For example, at 55 years old at $125, 850 (Guaranteed Portion for Manulife ReadyBuilder II), if $40, 000 were to be withdrawn, the remaining guaranteed amount will be reduced accordingly and the plan will still continue to yield interest.

Guaranteed Cash Value:

| Manulife

ReadyBuilder II |

|

| 50 years old | $123, 906 |

| 55 years old | $126, 457 |

| 60 years old | $ 131, 378 |

| 65 years old | $ 155, 556 |

| 70 years old | $ 164, 608 |

2. Buying Term & Invest the Rest (B.T.I.R.)

Buying Term and Investing the Rest (B.T.I.R.) is a way of separating your premium budget into a term insurance and growing the wealth in a separate instrument, be it a savings plan or investment. Typically this works for those that do not like the idea of whole life insurance with cash value element, making the premium higher and cash value lower during old age. They would prefer to grow wealth themselves, in a separate instrument. B.T.I.R. may be cheaper than getting a whole life plan on its own.

We compare with one of the most competitive whole life insurance and term plan in the market respectively: comparing with this combination: Singlife with Aviva’s MyWholeLife IV VS Singlife with Aviva MyProtector Term Plan II with Manulife’s ReadyBuilder II. This is because Singlife with Aviva has a good and competitive critical illness feature with its ICU benefits, Malignant tumour benefits which pays out on top of the sum assured, making it one of the more competitive in the market, not to mention it is extremely versatile.

For the term plan, Singlife with Aviva’s Term MyProtector Term has the option to include the multi-pay CI rider, allowing critical illnesses of different groups or different stages of the same group of critical illness to be covered for more than once.

With this combination of term insurance and Manulife’s Ready Builder II, after the age of 70 where supposedly the multiplier has already ended in the whole life plan, the cash value accumulated in ReadyBuilder II far exceeds the cash value in the whole life plan.

The best thing about this?

You don’t even have to be diagnosed with any conditions nor illness to enjoy this wealth. Because they are your savings. NOT a Critical Illness Payout.

| Plans | Singlife Aviva

Whole Life Plan |

Singlife Aviva

Elite Term Plan |

Manulife

ReadyBuilder II |

| Basic Sum Assured | $100,000 | $1,000,000 | NA |

| Multiplier | x2

(Until age 70) |

NA | NA |

| Early, Intermediate to Advance Stage Critical Illness

(Before age 70) |

$200,000 |

$200,000 |

NA |

| Death/TPD/Terminal Illness

(Before age 70) |

$200,000 + Interest & Yield (non-guaranteed) | $1,000,000 | 105% of total Premiums Paid + Interest & Yield (non-guaranteed) |

|

Death/TPD/Terminal Illness (After age 70) |

$100,000 + Interest & Yield (non-guaranteed) | Plan Terminates after age 70 | 105% of total Premiums Paid + Interest & Yield (non-guaranteed) |

| Annual Premium | $3,968.00 | $2,799.90 | $2,015.61 |

Death Coverage After Multiplier Ends After Age 70

| Plans | Singlife Aviva

Whole Life Plan |

Manulife

ReadyBuilder II |

| Death/TPD/Terminal Illness (After age 75) @ 4.25% Non-Guaranteed Yield | $177,940 | $111,965 |

| Death/TPD/Terminal Illness (After age 80) @ 4.25% Non-Guaranteed Yield | $195,112 | $133,011 |

| Death/TPD/Terminal Illness (After age 85) @ 4.25% Non-Guaranteed Yield | $213,856 | $159,619 |

Cash Value After Multiplier Ends

| Plans | Singlife Aviva

Whole Life Plan |

Manulife

ReadyBuilder II |

| Cash Value at age 75 with 4.25% Non-Guaranteed Yield | $126,179 | $110,857 |

| Cash Value at age 80 with 4.25% Non-Guaranteed Yield | $150,981 | $131,694 |

| Cash Value at age 85 with 4.25% Non-Guaranteed Yield | $177,935 | $158,039 |

3. Child’s Education for Young Parents

Children’s Education plans are a type of endowment savings plan that is structured to payout a number of range of years (usually 2 to 4 years) at a payout age, usually when the child is due to go for tertiary education at around 18 to 20 years old. This is however, rigid and difficult to gauge because, well, life and situation they change by the time our child reach that age.

Example below shows the Manulife Ready Builder II and the withdrawn Manulife Educate (Best Education Plan for Cash Payout) when the child is born at age 0:

| Plans | Manulife Educate (Withdrawn) | Manulife ReadyBuilder II |

| Premium Term | 10 years | 10 years |

| Premium Amount | $5,035.52 | $5,003.08 |

| Payout Structure | Before chosen Payout Age (age 18 or 20) – 2 yearly cash benefits

After chosen Payout Age (age 18 or 20) – 4 yearly cash benefits

|

It is strongly advised to withdraw the cash value after it breaks even (15th year) |

Guaranteed Cash Payout when child is:

| Manulife Educate (Withdrawn) | Manulife ReadyBuilder II | |

| 16 years old | $2,800 | $52,072 |

| 17 years old | $2,800 | $52,273 |

| 20 years old | $22,400 | $53,016 |

| 21 years old | $11,200 |

Between $53,623 to $55,897

(Plan continues to grow until you are 120 years old) |

| 22 years old | $11,200 | |

| 23 years old |

$11,200 (Policy Maturity Amount, Plan Terminates) |

|

| 25 years old | NA |

Comparison With Similar Plans

|

Plans

|

Etiqa

Enrich Flex |

Manulife

ReadyBuilder II |

AIA

SmartWealth Builder II |

| Premium | $5,077.80 | $5,003.38 | $5,000 |

| Savings Term | 20 Years | 20 Years | 20 Years |

| Breakeven (Guaranteed) | 15th year | 15th year | 15th year |

| Premium Term | 10, 15 and 20 years only | Choice of Single Premium or regular premium of 5, 10, 15 or 20 years. | Choice of Single Premium or regular premium of 5, 10, 15 or 20 years. |

| Maturity Year | Until Age 100 | Until Age 120 | Until Age 105 |

| Value at the end of 20th year | $106,050

Plan continues to grow until you are 100 years old |

$104,296

Plan continues to grow until you are 120 years old |

$69,650 Plan continues to grow until you are 125 years old |

Find out more on the Etiqa Enrich Flex Plan here

Etiqa Enrich Flex Plan Review: Legacy Endowment With Competitive Returns

Etiqa Enrich Flex Plan Review: Legacy Endowment With Competitive Returns

Find out more on the AIA Smart Wealth Builder here

How Manulife’s ReadyBuilder (II) Works

The Manulife ReadyBuilder (II) is Suitable if You:

- You wish to accumulate wealth or legacy planning to leave your beneficiaries with an inheritance.

- Choose to change life insured after 2 years into the plan to continue your legacy planning efforts.

- You have certain life milestones that may need cash funding. This policy allows you to withdraw cash to facilitate some important life milestones such as starting a business or paying for your child’s college tuition fee, or even your own retirement.

It would however be less suitable if you would like:

- High protection for critical illness from early to advance stage.

- Hospitalisation coverage

- Death, TPD and Terminal Illness coverage

Manulife ReadyBuilder (II) In-Depth Review

Manulife’s ReadyBuilder II offers a comprehensive and flexible solution for long-term financial planning. With its versatile withdrawals, compounding wealth, and coverage until age 120, it is a reliable option for securing your financial future.

Don’t navigate the complexities of financial planning alone.

Get in touch with our experienced financial advisor today to explore how ReadyBuilder II can benefit you and create a tailored financial strategy that aligns with your goals. Take the first step towards a secure future by contacting our financial advisor for personalized guidance and peace of mind.

Based on your needs, a custom made solution will be adjusted only addressing your concern with no obligations nor hidden fees.

Fill in the form below and our friendly licensed FA advisor will get in touch with you based on your needs.

No obligations, no hidden fees. All advice are of no charges.