Last Updated on by Tree of Wealth

In Singapore, Health Insurance, or Hospitalisation Plans, are usually associated with MediShield Life and Integrated Shield Plans (ISPs). This is the most common and basic healthcare plan utilizing the CPF MediSave to supplement part of the payment for the ISPs, making it more affordable with this Government-backed healthcare plan for Singaporeans.

A comprehensive healthcare plan, ISPs offered by insurers in Singapore covers for mainly hospitalization treatments (Inpatient and Outpatient) as well as the hospital ward stay. The different classes in the ward charges differently.

However, there are some areas that ISPs are not covering; for example, normal gynaecology visits during pregnancy as well as dental services are not covered for. Aside from MediShield Life, are you aware that if you have pre-existing conditions, Integrated Shield Plans from private insurers do not cover them?

About HSBC Life GlobalCare

Enter the HSBC Life GlobalCare: Originally intended for expats and residents in surrounding countries of Singapore to seek good medical treatment in Singapore, it also has other features that even local Singaporeans will find it useful, particularly the coverage for pre-existing condition features, as ISPs will not cover. And the premium? It doesn’t differ much from ISPs.

It is basically a health insurance plan that covers internationally within the countries included in the packages and in a more comprehensive manner that ISPs did not:

- Optical expenses

- Dental expenses

- Vaccinations

- Maternity expenses

- Outpatient treatments

- Inpatient treatments and many more.

What makes HSBC Life Global Care more alluring is that it covers even the pre-existing conditions providing the beneficiary meets certain conditions, read below to find out.

Product Features and Benefits at a Glance

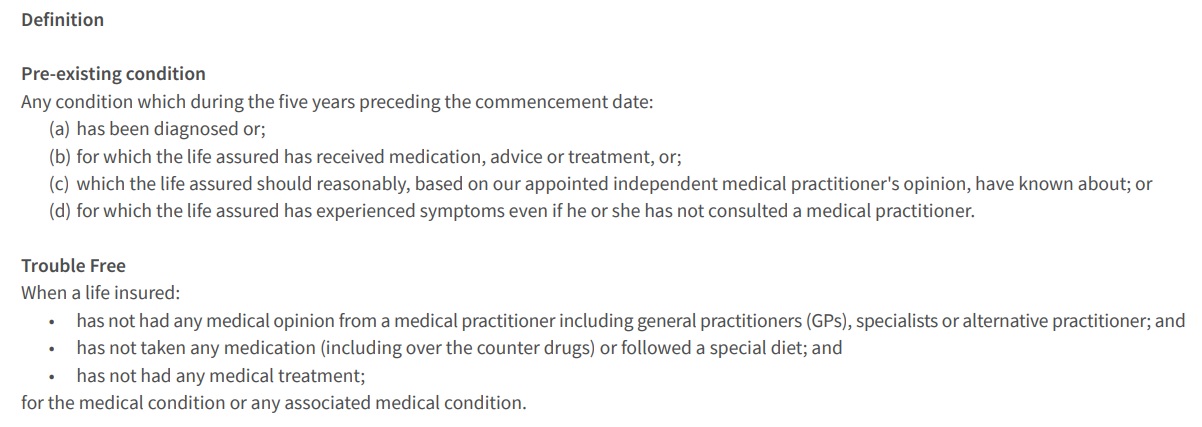

Pre-existing Conditions Coverage

With certain conditions fulfilled as well as staying trouble free for 2 years, Pre-existing conditions are covered for.

Maternity and Newborn Benefits & Coverage

Maternity expenses like delivery charges are covered for. Pre and post natal complications are also covered for.

Wellness and Preventive Health Coverage

Cover yourself for vaccinations, dental care, optical care, health screening and alternative treatments like Traditional Chinese Medicine, homeopathy and more in selected plans.

100% Coverage

Unlike the ISP, there is no Co-payment involved. 100% coverage for hospitalization and treatment, without the hassle.

This includes expenses for inpatient and outpatient treatments incurred pre and post hospitalization as well as hospice & palliative care.

Guaranteed Renewability

Regardless of claims, your policy will be renewed yearly with the original terms and conditions.

Guaranteed Acceptance

No medical underwriting, health checks, medical examinations nor health questions.

Things To Note:

Entry Age – 80 years old Maximum

Maximum Coverage Age – 99 years old

Waiting Period – 12 months upon the inception of the policy.

What We Like About The Plan

Full Coverage for Hospitalisation Stay/Treatment

Integrated Shield Plans (ISPs) today no longer have 100% full coverage anymore due to the new directive from MOH (Ministry of Health). The most comprehensive coverage with an ISP entails a 5% co-payment even if you use cash and top it up with the insurer’s most complete rider/ Policyholders now have to bear a 5% co-payment of hospital bill, with it being capped at $3000 annually.

If the Hospitalisation has many treatments going on and long stays for an extended period of time, it could still build up to become a hefty expense. Hence, HSBC Life’s GlobalCare provides a comprehensive 100% hospitalization coverage when compared to ISP, as there are no co-payment involved with GlobalCare and it is still 100% covered for.

Health Benefit Discount – Co-Insurance Option

The HSBC Life GlobalCare gives you the option for Co-paying your hospitalization bills should you decide you are healthy. For the co-insurance option, you will enjoy an 18% discount on your premium.

Worldwide Healthcare Coverage

HSBC Life GlobalCare’s flexibility covers for you even if you are not residing in Singapore. As long as premiums are paid, it will continue to cover you no matter where you are, and the country you are seeking medical treatment in.

It is suitable for local Singaporeans as well as foreigners and expats, which the latter may find it more worthwhile as compared to an ISP where full cash payment is needed as they lack CPF.

For local Singaporeans, unlike the ISP where it provides only emergency accidental and emergency treatments overseas, HSBC Life’s GlobalCare covers for planned healthcare expenses anywhere in the world.

No Medical Underwriting Process/Questions Asked

Upon application there are no medical underwriting, examinations, process nor questions needed, making it a fuss-free sign-up for policy holders.

HSBC Life GlobalCare also covers for pre-existing conditions and in HSBC Life’s words “will reward you for improving your health and being Trouble Free for two years”. Thereafter, your pre-existing conditions will be covered for life.

When it comes to insurance plans covering critical illness, whole life and term plans, all insurers will subject policy holders on medical questions and examinations and upon the presence of pre-existing conditions, most will include exclusion of conditions covered or loading/ additional premiums making policy even more expensive, which brings us to the next point:

Competitive Premium VS ISP

Comparison of Integrated Shield Plan Premiums (Private Hospitals)

Payable by CPF MediSave, do note this portion is on top of the default MediShield Life that is being charged.

| Age | Additional Withdrawal Limit (CPF MediSave) | AIA HealthShield Gold Max | Aviva MyShield Plan 1 | HSBC Life Shield Plan A | NTUC IncomeShield Preferred |

| 1 – 20 | 300 | $191 | $192 | $167 – $170 | $205 – $252 |

| 21 – 25 | 300 | $191 | $232 | $174 | $255 |

| 26 – 30 | 300 | $247 | $232 | $221 | $255 |

| 31 – 35 | 300 | $300 | $409 | $286 | $375 |

| 36 – 40 | 300 | $334 | $409 | $299 | $392 |

| 41 – 45 | 600 | $754 | $714 | $600 | $648 |

| 46 – 50 | 600 | $818 | $924 | $600 | $766 |

| 51 – 55 | 600 | $1165 | $1166 | $887 | $888 |

| 56 – 60 | 600 | $1480 | $1483 | $1,159 | $1162 |

| 61 – 65 | 600 | $1999 | $1957 | $1,567 | $1592 |

| 66 – 70 | 600 | $2939 | $2774 | $2,200 | $2250 |

Comparison of Cash Rider 95% Co-Insurance Rider

Payable by Cash

| Age Next Birthday

|

HSBC Life Enhanced Care Rider (Plan A) | NTUC Income

Deluxe Care Rider (EIS Preferred Plan) |

Raffles Health Insurance Key Rider (Private) | AIA Max VitaHealth A Rider | Singlife Health Plus Private Prime Rider |

| 1 – 20

|

$444.10 – $459.30 | $445.12 – $482.47 | $236.19 – $280.60 | $642.95 | $589.45 |

| 21 – 30

|

$474.40 – $489.50 | $198.84 | $288.67 | $642.95 | $675.25 |

| 31 – 40

|

$570.30 – $575.30 | $213.98 – $219.03 | $299.78 – $304.82 | $712.59 | $772.15 |

| 41 – 50

|

$605.60 – $767.10 | $330.06 – $349.23 | $309.87 – $402.73 | $881.15 – $994.20 | $927.59 – $989.16 |

| 51 – 60

|

$928.60 – $1635.10 | $470.36 – $536.97 | $486.51 – $863 | $1415.10 – $1821.86 | $1,244.53 – $1,812.78 |

| 61 – 65

|

$2,119.60

|

$760.04 | $1087.06 | $2453.71 | $2,467.85 |

| 66 – 70

|

$3,028.00

|

$1006.32 | $1410.06 | $3346.99 | $3,033.08 |

| 71 – 73

|

$3,755.80

|

$1256.64 | $1706.80 | $3989.94 | $3,375.25 |

| 74 – 75

|

$4,340.20

|

$1,482.73 | $1896.56 | $4490.57 | $3,472.15 |

| 76 – 78

|

$4,827.70

|

$1563.48 | $1916.75 | $4803.47 | $3,513.53 |

| 79 – 80

|

$5,097.20

|

$1793.61 | $2013.65 | $5188.03 | $3,567.02 |

| 81 – 83

|

$6,318.50

|

$2012.64 | $2382.06 | $5499.92 | $3,759.81 |

| 84 – 85

|

$6,358.90

|

$2222.58 | $2382.06 | $5835.02 | $3,888 |

| 86 – 90

|

$6,550.70 – $

6,914 |

$2401.23 – $2716.15 | $2390.13 – $2525.39 | $6187.28 – $6561.75 | $4,017.20 – $4,234.20 |

| >90 years old

|

$7,475.20 –

$9,487.90 |

$2934.17 – $3790.09 | $2753.49 – $3479.22 | $6780.78 – $7482.28 | $4,517.83 – $5,862.28 |

The premiums are actually very competitive even if you compare it with an ISP. However, for the HSBC Life GlobalCare, CPF MediSave is not useable here and that is the only difference with the usual ISP as MediSave pays part of the premiums for that, with cash rider portion.

GlobalCare has 5 plan packages, consisting from Plan A to E. Plan E is an affordable package that covers for healthcare services like inpatient treatment, full 100% of the hospitalization cost and you have a choice of choosing your doctor.

Coverage of Pre-Existing conditions and even congenital illnesses are eligible (as long as 2 years trouble free). The premiums are slightly higher than ISP and is payable by cash with no MediSave involvement.

How HSBC Life GlobalCare Works

Who Is More Suited To The HSBC Life GlobalCare?

This Is Suitable For You If:

- You have pre-existing condition and trouble-free for 2 years (Moratorium Underwriting Period of 2 years), thereafter the plan covers pre-existing condition for life thereafter

- You would like a global healthcare plan with no medical underwriting & questions with guaranteed acceptance

- You are looking for an International Global Healthcare plan priced reasonably

- 100% coverage hospitalization & healthcare treatment with no co-payment is what you are looking for

- You want to have the choice of comprehensive inpatient and outpatient treatment coverage

This Is Not Suitable If:

- You don’t have pre-existing condition

- You are fine with local Singapore’s healthcare with no need for global coverage

- You prefer to use MediSave to supplement part of your healthcare premium.

Do you really need HSBC Life GlobalCare?

Although marketed as a global healthcare plan, depending on the individual it most importantly all boils down to 4 main factors to consider for HSBC Life’s GlobalCare: pre-exisiting conditions coverage, 100% full healthcare coverage, international global hospitalisation coverage as well as full suite of treatment protection including maternity and dental coverage.

These are not covered by MediShield Life nor Integrated Shield Plans (ISPs) and premiums are not that much of a big difference. Getting the HSBC Life GlobalCare also means you can stay at better private hospitals without paying huge hospital bills.

Get the Best Health Insurance Singapore 2020

From this in-depth GlobalCare review we hope you find value and a better understanding in finding the best Health Insurance Protection in Singapore/Globally that best suits your needs today.

For Professional Advice, simply fill in the form below and our friendly experienced licensed FA advisor will get in touch with you based on your needs.

No obligations, no hidden fees. All advice are of no charges.