Last Updated on by Tree of Wealth

AIA has a new Critical Illness (CI) plan it is called Absolute Critical Cover (ASCC). It is a multiple-claim critical illness protection coverage that allows you to safeguard yourself in the events of early, intermediate and advance stage critical illnesses, as well as for chronic and special diseases. Some of the new components that AIA offer, are the child premium discount and cash value (first and only plan in the market to offer this, albeit the premium being one of the highest).

Critical illness coverage has been one of the many hot topics in Singapore. Be it the type of coverage, length and sum assured to be covered for, there are many variations and factors to consider towards constructing a suitable plan for yourself.

Let’s look at the unique features of this latest CI plan from AIA:

AIA Absolute Critical Cover Features At a Glance

1) PRE-EARLY CONDITIONS COVERAGE (BENIGN TUMOUR, CHRONIC DISEASE, SENIOR SILVER)

ASCC covers most of the aspects of diseases across different life stages. There are 3 components when it comes to getting covered for Pre-early conditions, namely: Benign Tumour, Chronic Disease and Senior Silver.

Benign Tumour

For Benign Tumour Benefit of up to 22 specified organs, you can claim up to 1 x 10% of sum assured (capped at $25,000). The criteria to claim for this is that the insured must :

1) Undergo the excision of tumour as recommended by a registered pathologist

2) Tumour must not be cancerous

3) The tumour must undergo histopathological examination after excision

Here are the listed specified organs covered:

1. Heart

2. Liver

3. Lung

4. Pancreas

5. Pericardium

6. Ureter

7. Adrenal Gland

8. Bone

9. Conjunctiva

10. Kidney

11. Nerve in cranium or spine

12. Pituitary gland

13. Small intestine

14. Testis

15. Breast

16. Ovary

17. Penis

18. Uterus (covers endometrial polyps only)

19. Nasopharyngeal

20. Esophagus

21. Oral Cavity

22. Gallbladder

Chronic Disease

For Chronic Disease Benefit of up to 7 different conditions, you can claim up to 1 x 10% of sum assured (capped at $10,000). The criteria to claim for this is that the insured must :

1) Be diagnosed for the condition by a registered doctor or,

2) Undergoes a surgery for a Chronic Disease condition

3) Survives for at least 7 days from date of diagnosis or date of surgery performed

These are the conditions listed under this benefit :

1. Age-related macular degeneration with visual impairment

2. Psoriatic arthritis

3. Severe Hypertension

4. Severe Obstructive or Mixed Sleep Apnoea

5. Severe presbycusis (Age-related hearing loss)

6. Thyroid disorders

7. Varicose veins requiring surgery

Senior Silver Benefit

One of the newest addition coverage in the market covering for 3 specified conditions, you can claim up to 1 x 10% of sum assured (capped at $25,000). The criteria to claim for this is that the insured must be:

1) 51 years old and above before this benefit commences

2) Diagnosed or undergo surgery for the covered conditions

3) Survivor for at least 7 days from date of diagnosis or date of surgery performed

These are the covered conditions :

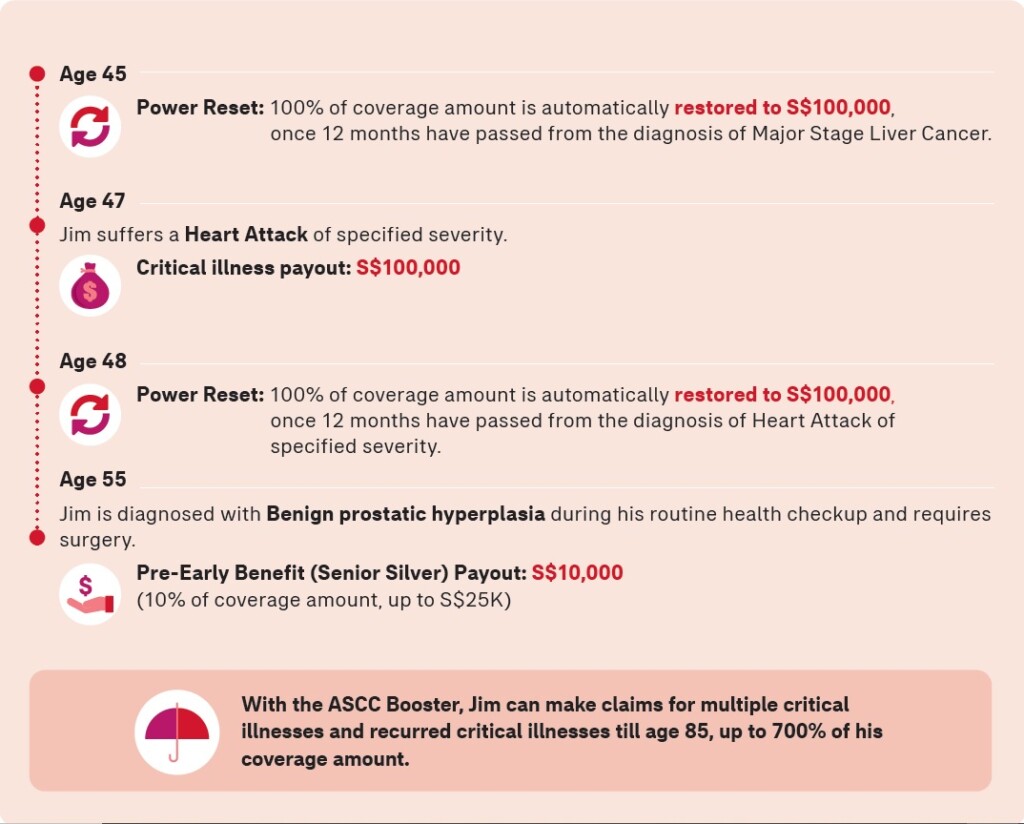

1. Benign prostatic hyperplasia requiring surgery

2. Glaucoma requiring surgery

3. Urinary incontinence requiring surgical repair

2) CHILD PREMIUM DISCOUNT AND SURRENDER VALUE

If you have a child below the age of 21 and is currently covered by this plan, you can purchase the same plan for your child (with you as the policy owner) and enjoy the child premium discount according to the table below.

|

Number of Children Insured |

Premium Discount (till age 21) |

|

1 |

5% |

| 2 or more |

10% |

The ASCC has a surrender value benefit only for the term up to 100 years old (Life Plan). It is not applicable if you are looking at the plan up till age 65 or 75 (Value Plan).

This benefit will only be available after the 60th policy anniversary, or when the life assured reaches age 75 (whichever is earlier). The cash value would be equivalent to 75% of the sum assured, after deducting any claim amount made. If there is a claim made during the policy, this benefit will not be applicable.

The cash value of the plan would also increase 1% of the sum assured from life assured 76th birthday onwards.

If the life assured reaches 100 years old with no claims made, AIA will be paying 150% of the insured amount (less any amount owing to them) under the policy.

3) ICU COVERAGE

Although this plan is a critical illness plan, it does come with ICU coverage as well. In the event of 1 hospitalisation admission that requires you to stay 4 or more days in the ICU, there will be a 20% pay out based on the sum assured, capped at $25,000.

4) COVERAGE LENGTH

The coverage length available is up to age 65, 75, or 100.

5) CRITICAL ILLNESS COVERAGE

The plan provides coverage for all 3 stages of Critical Illness. A total of 150 multi-stage critical illness are covered, and the max payout for early or intermediate stage is up to $350,000.

The ASCC also covers a wide range of special and juvenile conditions. There are 25 of these conditions and maximum claim of 10x can be made in total, subjected to 20% of sum assured capped at $25,000. This is comprehensive not just to cover adults, but it is also feasible for children as well!

6) POWER RESET & POWER RELAPSE BENEFIT

The AIA Absolute Critical Cover plan is a multipay CI plan and this is the multipay feature. The Power Reset benefit basically helps to keep you covered, even after a diagnosis happened and the claim has been made. If the policy is in force for 12 months after the date from your latest diagnosed critical illness, the sum assured will be restored back to 100% of insured amount, allowing you to make multiple claims to a total of up to 500%.

The Power Relapse benefit can be used when the insured is re-diagnosed or suffered recurrence from the mentioned specified Critical Illness (please see the list below), or undergoes a surgery 2 years after its first diagnosis. 100% of the sum assured will be paid out and can be claimed once for up to 2 re-diagnosed/recurrent conditions (up to 200%).

1) Re-diagnosed Major Cancer

2) Recurred Heart Attack

3) Recurred Stroke

4) Repeated Major Organ Transplant / Bone Marrow Transplantation

5) Repeated Heart Valve Surgery

These 2 benefits come in the form of an optional rider called ASCC Booster, which can be integrated with your AIA Vitality program for premium discounts.

7) DEATH BENEFIT

In the event of death, there will be a payout of 5% of sum assured + surrender value of the plan, at any point of the policy term.

PREMIUM COMPARISON TILL AGE 75

MALE

| Male Non-Smoker $150,000 Sum Assured |

AIA Absolute Critical Cover with ASCC Booster and Early CI Premium Waiver | Aviva MyMultipay CI IV | TM Multicare |

| 30 | $3,291.75 | $2,433.00 | $2,442.00 |

| 35 | $3,899.81 | $3,015.00 | $3,111.00 |

| 40 | $4,237.50 | $3,870.00 | $4,287.00 |

| 50 | $8,128.15 | $7,690.50 | $7,584.00 |

FEMALE

| Female Non-Smoker $150,000 Sum Assured |

AIA Absolute Critical Cover with ASCC Booster and Early CI Premium Waiver | Aviva MyMultipay CI IV | TM Multicare |

| 30 | $3,401.71 | $2,604.00 | $2,553.00 |

| 35 | $4,509.49 | $3,226.50 | $3,255.00 |

| 40 | $4,970.65 | $4,107.00 | $4,204.50 |

| 50 | $7,139.87 | $7,618.50 | $6,849.00 |

HOW IT WORKS

AIA Absolute Critical Cover is Suitable if You:

1) Prefer a wide range of coverage for the Pre-Early Condition benefit

2) Prefer The Power Reset and Power Relapse Benefit, helps to strengthen and multiply the payouts

3) Prefer to look for a coverage for their children with Children Premium Discount. This would be for parents whom are currently on this plan. However with other more competitive premium plans in the market, parents should really look at the options.

4) Prefer the Surrender Value, one of the few CI plans in the market that has cash value.

It would however be less suitable if you would prefer :

- Like a whole life coverage

- Endowment Savings wealth growth purposes

What We Don’t Like About the Plan

- As with AIA’s previous iterations of their CI plans, there are little flexibility on the policy term. This plan only has 3 options of ending at age 65, 75 or 100.

- Waiting period of 1 year in between each claim. Insurers like Aviva and Tokio Marine has no waiting period when the CI transits from early to advance stage.

- Very expensive as compared to other comprehensive multipay CI plans in the market (Aviva, Tokio Marine)

Conclusion for AIA Absolute Critical Cover :

There are potentials and limits of each plan, and no single plan is suitable for every needs and concerns. Working with financial planners with experience in this field that has access to multiple insurers, providing you with an objective point of view and neutral recommendations based on your needs.

Start today by getting in contact with us and have your coverage needs assessed!

Drop us an inquiry below and our professional experienced licensed FA advisor will get in touch with you shortly upon your request.